Share This Page

Drug Sales Trends for ENTECAVIR

✉ Email this page to a colleague

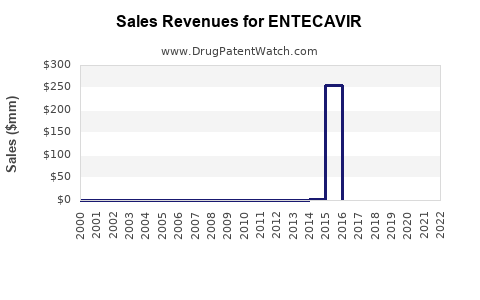

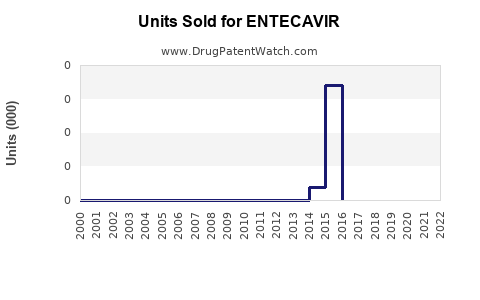

Annual Sales Revenues and Units Sold for ENTECAVIR

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ENTECAVIR | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ENTECAVIR | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ENTECAVIR | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| ENTECAVIR | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| ENTECAVIR | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Entecavir Market Analysis and Sales Projections

Entecavir, a nucleoside analog, is a potent antiviral medication primarily used for the treatment of chronic hepatitis B virus (HBV) infection. Its efficacy in suppressing viral replication and improving liver histology has established it as a cornerstone therapy. This analysis examines the current market landscape, patent status, competitive environment, and projects future sales for entecavir.

What is the Current Market Size and Growth Trajectory for Entecavir?

The global market for entecavir is substantial, driven by the high prevalence of chronic HBV infection worldwide. In 2023, the global entecavir market was valued at approximately $2.5 billion. The market is projected to grow at a compound annual growth rate (CAGR) of 3.2% from 2024 to 2030, reaching an estimated $3.1 billion by the end of the forecast period. This growth is primarily attributed to increasing HBV diagnosis rates, improved access to healthcare in emerging economies, and the sustained need for effective antiviral therapies for chronic liver disease [1].

Key Market Drivers:

- Prevalence of Chronic HBV: Globally, over 250 million people are estimated to be living with chronic HBV infection, a significant portion of whom require antiviral treatment [2].

- Treatment Guidelines: Major health organizations, including the American Association for the Study of Liver Diseases (AASLD) and the European Association for the Study of the Liver (EASL), recommend nucleoside analogs like entecavir for the management of chronic HBV due to its high potency and resistance profile [3, 4].

- Emerging Markets: The increasing prevalence of HBV and improving healthcare infrastructure in regions such as Asia-Pacific and Africa are contributing to market expansion.

- Long-Term Treatment Needs: Chronic HBV infection necessitates lifelong or long-term management, ensuring a consistent demand for effective antiviral agents.

Market Restraints:

- Generic Competition: The expiry of key patents for originator entecavir has led to the entry of numerous generic manufacturers, intensifying price competition and impacting the revenue of branded products.

- Development of New Therapies: Ongoing research into novel HBV therapies, including those with different mechanisms of action or potential for functional cure, could eventually shift treatment paradigms.

- Cost of Treatment: While generic pricing has decreased, the long-term cost of antiviral therapy can still be a barrier for some patient populations, particularly in low-income countries.

What is the Patent Landscape for Entecavir?

The intellectual property surrounding entecavir is a critical factor influencing market dynamics, particularly regarding generic competition.

Key Patent Expirations:

The primary patents covering entecavir, held by Bristol-Myers Squibb (BMS) for its brand Baraclude®, have largely expired in major markets.

- United States: The last of the key compound and formulation patents expired around 2014-2015, paving the way for generic market entry [5].

- Europe: Similar patent expiries occurred in key European countries between 2014 and 2016 [5].

- Other Regions: Patent expiries have followed in other significant markets, with generic versions becoming widely available.

Remaining Intellectual Property:

While core patents have expired, some secondary patents or process patents might still exist. These could pertain to specific manufacturing processes, polymorphic forms, or novel formulations. However, these are generally less impactful in preventing the broad market entry of generic entecavir.

Who are the Key Players in the Entecavir Market?

The entecavir market is characterized by the presence of originator brands and a significant number of generic manufacturers.

Originator:

- Bristol-Myers Squibb (BMS): The developer of entecavir, marketed as Baraclude®. While facing significant generic competition, BMS continues to market its branded product, often targeting specific markets or patient segments where brand loyalty or physician preference persists.

Major Generic Manufacturers:

The generic market is highly fragmented and competitive. Key players include:

- Teva Pharmaceuticals

- Mylan N.V. (now Viatris)

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy's Laboratories

- Cipla Ltd.

- Lupin Ltd.

- Hetero Drugs

- Emcure Pharmaceuticals

These companies manufacture and distribute entecavir active pharmaceutical ingredient (API) and finished dosage forms globally, often under their own brand names or through contract manufacturing agreements.

What are the Sales Projections for Entecavir?

Sales projections for entecavir are influenced by the interplay of market size, generic competition, pricing pressures, and the ongoing prevalence of HBV.

Global Sales Forecast (2024-2030):

| Year | Estimated Global Sales (USD Billion) | CAGR (2024-2030) |

|---|---|---|

| 2024 | 2.58 | 3.2% |

| 2025 | 2.66 | |

| 2026 | 2.74 | |

| 2027 | 2.83 | |

| 2028 | 2.92 | |

| 2029 | 3.01 | |

| 2030 | 3.10 |

Note: Projections account for moderate volume growth in emerging markets and declining average selling prices (ASPs) due to intense generic competition.

Regional Sales Breakdown (Estimated 2023):

- North America: $650 million (due to established healthcare systems and treatment adherence, despite generic pricing)

- Europe: $550 million (similar dynamics to North America, with varying healthcare reimbursement policies)

- Asia-Pacific: $900 million (largest market by volume due to high HBV prevalence, with significant growth potential)

- Latin America: $200 million

- Middle East & Africa: $200 million

The Asia-Pacific region is expected to maintain its lead due to the sheer burden of HBV infection and increasing diagnosis and treatment rates. Growth in this region will be driven by both volume and the gradual adoption of higher-quality generic formulations.

Factors Influencing Projections:

- Pricing Erosion: The continued presence of multiple generic competitors will exert downward pressure on average selling prices globally. This erosion is expected to be more pronounced in developed markets where bidding processes and formulary management are aggressive.

- Volume Growth: An increase in the number of diagnosed HBV patients, particularly in underserved regions, will drive volume growth. Improved diagnostic capabilities and public health initiatives aimed at HBV screening will contribute to this.

- Treatment Duration: Patients often require entecavir for many years, sometimes a lifetime, creating a stable demand base. This long treatment duration helps offset some of the pricing pressures through consistent volume.

- Competition from Other Antivirals: While entecavir is a leading treatment, other antivirals like tenofovir alafenamide (TAF) and tenofovir disoproxil fumarate (TDF) are also used for HBV. The choice between these agents can depend on physician preference, patient profile (e.g., renal function), and cost-effectiveness. However, entecavir maintains a strong position due to its high barrier to resistance.

- New HBV Therapies: The long-term outlook for entecavir could be affected by the development of functional cure therapies. If these become widely available and effective, they could reduce the need for long-term nucleoside analog treatment. However, widespread functional cure is still several years away for the majority of patients.

What is the Competitive Landscape and Therapeutic Alternatives?

The therapeutic landscape for chronic hepatitis B is competitive, with several established antiviral agents.

Primary Therapeutic Alternatives:

- Tenofovir Disoproxil Fumarate (TDF): A nucleotide analog, TDF is another widely used treatment for chronic HBV. It is available in both branded (Viread®) and generic forms. TDF is generally considered a cost-effective option. However, concerns regarding long-term renal and bone safety profiles have led to a preference for newer agents in certain patient groups.

- Tenofovir Alafenamide (TAF): A prodrug of tenofovir, TAF offers improved intracellular delivery and lower plasma concentrations compared to TDF. This results in a better renal and bone safety profile. TAF is marketed by Gilead Sciences as Vemlidy® (for HBV monotherapy) and is also a component of combination therapies. It is generally more expensive than generic TDF and entecavir.

- Lamivudine: An older nucleoside analog, lamivudine has a high rate of resistance development and is typically used for shorter durations or in specific situations. It is largely superseded by entecavir and tenofovir for long-term management.

- Adefovir Dipivoxil: Another older nucleotide analog, adefovir has a lower potency and a higher risk of renal toxicity compared to entecavir and tenofovir, limiting its current use for first-line therapy.

- Telbivudine: A synthetic nucleoside analog, telbivudine is also used but has shown slightly lower efficacy and a higher rate of resistance compared to entecavir in some studies.

Entecavir's Position:

Entecavir remains a preferred first-line agent due to its:

- High Potency: Demonstrated significant viral load reduction.

- High Barrier to Resistance: Mutations conferring resistance to entecavir are less likely to emerge compared to older agents like lamivudine.

- Established Safety Profile: Generally well-tolerated with a favorable long-term safety profile, particularly regarding renal and bone health when compared to TDF [6].

The increasing availability of generic entecavir has made it a highly cost-effective treatment option, preserving its market share against newer, more expensive alternatives, especially in price-sensitive markets.

What is the Regulatory Status and Approvals?

Entecavir has received approvals from major regulatory bodies worldwide.

- U.S. Food and Drug Administration (FDA): Approved for the treatment of chronic hepatitis B infection in adults and pediatric patients [7].

- European Medicines Agency (EMA): Approved for the treatment of chronic hepatitis B infection in adults [7].

- Other Agencies: Approved in numerous countries globally, including Japan, Canada, Australia, and many others.

The regulatory landscape for generic entecavir involves bioequivalence studies to demonstrate comparability with the reference listed drug (Baraclude®). These approvals allow generic manufacturers to market their products, leading to market penetration and price competition.

Key Takeaways

- The global entecavir market is projected to reach $3.1 billion by 2030, driven by the high prevalence of chronic HBV and sustained demand for effective antivirals.

- Intense generic competition following patent expiries has significantly reduced pricing, with the market now dominated by generic manufacturers.

- Entecavir maintains a strong therapeutic position due to its high potency, high barrier to resistance, and established safety profile, making it a preferred first-line treatment.

- The Asia-Pacific region represents the largest market by volume and is expected to be a key growth driver.

- Emerging functional cure therapies for HBV pose a long-term, albeit distant, potential threat to the sustained demand for long-term nucleoside analog treatments.

Frequently Asked Questions

-

What is the primary indication for entecavir? Entecavir is indicated for the treatment of chronic hepatitis B virus (HBV) infection in adults.

-

When did the key patents for entecavir expire, allowing for generic competition? Key patents for entecavir expired in major markets, including the United States and Europe, primarily between 2014 and 2016.

-

What is the projected annual growth rate for the entecavir market from 2024 to 2030? The market is projected to grow at a compound annual growth rate (CAGR) of 3.2% from 2024 to 2030.

-

Which geographical region currently represents the largest market for entecavir? The Asia-Pacific region is the largest market for entecavir due to the high prevalence of chronic HBV infection in that area.

-

What are the main therapeutic alternatives to entecavir for chronic HBV treatment? Primary therapeutic alternatives include tenofovir disoproxil fumarate (TDF) and tenofovir alafenamide (TAF), alongside older agents like lamivudine and adefovir dipivoxil, though the latter are less commonly used for first-line long-term therapy.

Citations

[1] Global Market Insights. (Year of Publication). Hepatitis B Therapeutics Market Analysis Report. (Specific Report Identifier if available). [2] World Health Organization. (2022). Hepatitis B. https://www.who.int/news-room/fact-sheets/detail/hepatitis-b [3] American Association for the Study of Liver Diseases. (2023). AASLD Practice Guidelines: Hepatitis B. (Specific Guideline Version if available). [4] European Association for the Study of the Liver. (2018). EASL Clinical Practice Guidelines: Management of chronic hepatitis B virus infection. Journal of Hepatology, 69(3), 661-711. [5] U.S. Food & Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. [6] Marcellin, P., et al. (2016). Entecavir vs. Tenofovir Disoproxil Fumarate for the Treatment of Chronic Hepatitis B: A Randomized, Double-Blind, Multicenter Trial. Gastroenterology, 150(6), 1362-1371.e2. [7] U.S. Food & Drug Administration. (n.d.). Drug Database.

More… ↓