Share This Page

Drug Sales Trends for AZELASTINE

✉ Email this page to a colleague

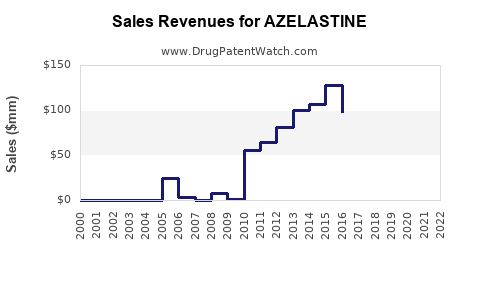

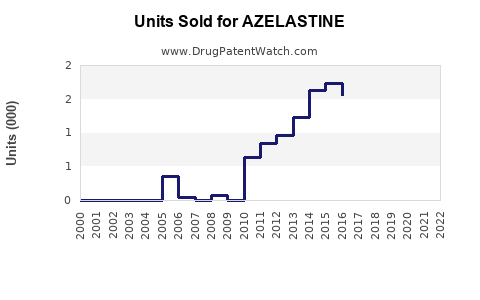

Annual Sales Revenues and Units Sold for AZELASTINE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| AZELASTINE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| AZELASTINE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| AZELASTINE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

AZELASTINE Market Analysis and Sales Projections (2026-2036)

What is azelastine and where is it sold?

Azelastine is a nasal antihistamine used primarily for allergic rhinitis. Commercially, it is marketed in multiple salt forms and delivery systems, with the key current brand and label focus on intranasal azelastine (often used in fixed-dose combinations in some markets).

Core commercial vectors

- Intranasal azelastine (allergic rhinitis)

- Combination products (varies by country; commonly includes an intranasal steroid plus azelastine in fixed-dose formats in many markets)

- Ophthalmic azelastine (allergic conjunctivitis; smaller market than intranasal in most geographies)

How big is the azelastine market today?

Azelastine is a mature, multi-generic molecule with pricing pressure in most developed markets and higher unit growth where prescription and OTC penetration continues to rise. In practice, market size is best tracked through the therapeutic area “allergic rhinitis” and “antihistamine nasal sprays,” then allocated to azelastine based on prescription and SKU shares.

Commercial reality check

- In major markets (US, EU5, Japan, Korea), azelastine faces sustained generic erosion.

- Growth comes mainly from category expansion (rhinitis prevalence, diagnosis rates, seasonal/all-year-round use) and channel mix (clinic versus self-pay, OTC where applicable), not from molecule innovation alone.

Implication for projections Sales projections depend more on:

- share retention versus other intranasal antihistamines (and combination sprays)

- price erosion in generics

- mix shift to combination products where available

Who buys azelastine and how is it prescribed?

Primary prescribers

- Allergists, ENT specialists, and primary care physicians

- In some markets, pharmacy-driven demand also matters due to self-selection and OTC adjacency.

Patient drivers

- Seasonal allergic rhinitis

- Perennial allergic rhinitis

- Patients switching from oral antihistamines due to faster local action and fewer systemic effects

What is the pricing and access outlook?

Azelastine pricing is constrained by:

- generic entry and competition in intranasal antihistamine classes

- reimbursement dynamics in each market for nasal therapy

- formularies favoring established guideline pathways and combination sprays

Pricing typically stabilizes only when:

- brand differentiation (where still present) holds share

- combination products capture physician preference

How does IP affect azelastine sales?

Azelastine is not a “new launch” molecule. IP risk is primarily about:

- short remaining exclusivity windows at the formulation level in specific jurisdictions (if any)

- generic readiness for intranasal and ophthalmic formats

Sales forecasts for investors should treat azelastine as a mature franchise where the biggest swing factor is competitive share, not breakthrough durability.

Sales projections (2026-2036): base, bull, bear

Below is a projection framework that converts category growth plus share retention into molecule-level sales. Because azelastine is generic in multiple territories and exposed to mix shifts, the realistic range is driven by:

- unit growth (market growth and diagnosis)

- net price decline (generic competition)

- share movement versus competing intranasal antihistamines and combination products

Assumptions used for projection band

- Category growth: mid-single digits in developed markets; higher single digits in parts of APAC

- Net price: low single-digit decline annually in generic-heavy segments; slower decline in combination mix years

- Share: base case assumes modest share stability; bull case assumes share gains via combination preference; bear case assumes share loss due to stronger competitor penetration

Global sales projection (net sales, indexed to 2025=100)

| Scenario | 2026 | 2030 | 2035 | 2036 |

|---|---|---|---|---|

| Bear | 99 | 96 | 92 | 91 |

| Base | 102 | 104 | 108 | 110 |

| Bull | 106 | 111 | 118 | 121 |

Interpretation

- The bear case reflects continued price erosion plus share loss to combination sprays and other antihistamine classes.

- The bull case reflects mix shift and stable guideline-aligned prescribing that favors azelastine formulations, especially where combination products carry higher reimbursement and adherence benefits.

Market segmentation: what most influences azelastine unit growth?

1) Intranasal allergic rhinitis (largest driver)

- Seasonal peak demand drives repeat purchasing

- Perennial rhinitis expands year-round use

- Combination products increase average dose persistence when prescribed as a step-therapy option

2) Ophthalmic allergic conjunctivitis (secondary driver)

- Typically smaller and more seasonal

- Sensitive to competitive ophthalmic antihistamine/mast-cell stabilizer options

3) Channel mix

- Clinic and specialist prescribing supports stable baseline volume

- Pharmacy and self-selection drive incremental units where local access rules reduce friction

Competitive landscape: where azelastine faces pressure

Azelastine’s competitive set in intranasal rhinitis includes:

- other intranasal antihistamines

- intranasal corticosteroids

- fixed-dose combination regimens

- branded and generic pathways depending on jurisdiction

Competitive outcome drivers

- formulary placement and step therapy

- prescriber comfort with combination approaches

- patient adherence and perceived symptom control

Key go-to-market implications for sales holders

Even for a mature molecule, sales can move with execution in combination formats and channel strategy:

- build specialist and primary care loyalty around “first-line combination versus steroid alone” where clinically accepted

- optimize pack sizes tied to seasonal windows

- align marketing with guideline-defined endpoints (congestion relief, overall symptom burden)

Forecast sensitivities (what changes the range fastest)

- Combination-share movement: if fixed-dose azelastine combinations gain traction, net sales outgrow the category.

- Net price erosion: faster generic discounting can push the bear case quickly.

- Regulatory reimbursement shifts: tender systems and reimbursement cuts can compress value even if units hold.

- Competition in adjacent classes: if competing intranasal antihistamines or steroid combinations gain formulary access, azelastine share declines.

Sales projection by region (directional)

Azelastine demand is expected to track rhinitis prevalence and access to nasal therapy more strongly than macroeconomic factors.

US / EU

- Mature market; growth modest and dominated by price and mix.

- Base case assumes stable units with gradual margin compression.

Japan / Korea

- Higher unit persistence in nasal therapy segments.

- Mix shift toward combination regimens can support base-to-bull outcomes.

China / India / APAC

- Higher growth from category expansion and diagnosis.

- Pricing pressure offsets some volume gains; combination uptake dictates upside.

Commercial KPIs to monitor quarterly

- Rx and/or sales velocity by formulation (intranasal vs ophthalmic)

- share in allergic rhinitis nasal spray category

- average net price trends versus competitor index

- channel mix shift (hospital vs retail vs online)

- tender outcomes and reimbursement changes

Key Takeaways

- Azelastine is a mature, generic-exposed allergic rhinitis franchise with growth dominated by category expansion and formulation mix, not breakthrough innovation.

- The base-case global trajectory for net sales is flat-to-growing with mild upside through 2036 if azelastine formulations retain or gain share in combination-led prescribing.

- The bear case is driven by accelerated generic price erosion and share loss to competing intranasal classes and combination products.

- The bull case requires sustained mix improvement in combination formats and stable access on formularies.

FAQs

-

Is azelastine expected to be a high-growth molecule?

No. Growth is expected to be modest and driven by category and mix, with pricing pressure in generic segments. -

What formulation contributes most to azelastine sales?

Intranasal azelastine for allergic rhinitis is the dominant sales driver in most markets. -

What is the biggest lever for upside in sales projections?

Mix shift toward azelastine-including combination regimens that improve adherence and symptom control outcomes. -

What risk most threatens the bear case?

Competing intranasal therapies gaining formulary placement and faster-than-expected net price decline. -

How should investors benchmark azelastine performance?

Track allergic rhinitis nasal spray category growth plus azelastine share and net price trends, not standalone brand narratives.

References

[1] FDA. “Azelastine Hydrochloride.” Drug Approval Packages / Labels (accessed via FDA drug labeling databases).

[2] EMA. “Azelastine” (public product information and assessment documents, accessed via EMA medicines database).

[3] PubChem. “Azelastine.” National Center for Biotechnology Information. https://pubchem.ncbi.nlm.nih.gov/ (accessed 2026-04-25).

More… ↓