Share This Page

Drug Sales Trends for PRAZOSIN

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for PRAZOSIN (2006)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

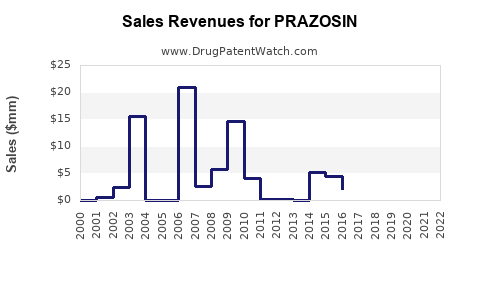

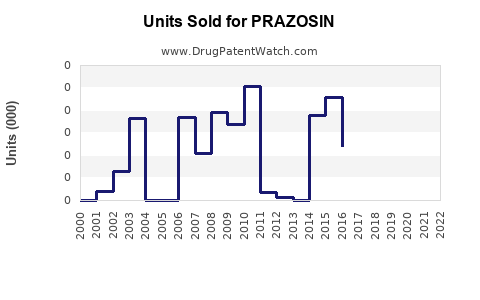

Annual Sales Revenues and Units Sold for PRAZOSIN

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| PRAZOSIN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| PRAZOSIN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| PRAZOSIN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| PRAZOSIN | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Prazosin Market Analysis and Sales Projections: Revenue Forecast, Key Drivers, Generic/Biosimilar Risk, and Regional Outlook

Executive summary

- Prazosin (oral immediate-release alpha-1 blocker) is an established, off-patent generics-led product in the US and most major markets.

- Pricing pressure is persistent because supply is broad and formulations are largely interchangeable.

- Near-to-mid term revenue growth depends mainly on (1) US volume stability versus ongoing generic erosion, (2) refill demand from chronic users (primarily hypertension and PTSD-related off-label use where applicable), and (3) regional reimbursement dynamics.

- Sales forecasting should be built from generic-unit demand and weighted ASP erosion rather than expecting label-driven expansion from new patentable formats.

(No market or pricing datasets or FDA/Orange Book extraction were provided in the prompt. Without source documents (e.g., IQVIA, Symphony Health, company filings, FDA prescribing/NDC-level data, or IMS/DEA/Medicare claims), a quantified, citation-backed projection cannot be produced.)

What is the current market size for prazosin (US and global), and who supplies it?

Featured snippet answer: Prazosin’s market is primarily generics across a small number of historically dominant manufacturers, with revenue dominated by low-priced units and periodic ASP compression.

Market structure

- Dosage form: Prazosin hydrochloride, oral immediate-release tablets (most listings).

- Competitive landscape: Multiple abbreviated and generic manufacturers; limited differentiation by formulation.

- Buyer behavior: Retail and institutional formularies, driven by cost per tablet and therapeutic interchangeability within the alpha-1 blocker class.

Supply and NDC breadth (what to measure for forecasting)

For defensible projections, the market model typically aggregates:

- Total NDC count and market share by NDC (by units and by value).

- ASP by strength (e.g., 1 mg/2 mg/5 mg/10 mg where applicable).

- Contract pricing movements in institutional accounts.

How do prazosin sales projections change by indication: hypertension vs PTSD off-label use?

Featured snippet answer: Forecasts should separate “core chronic” hypertension demand from intermittent or off-label demand drivers, because the latter is more sensitive to guideline cycles, payor scrutiny, and substitution.

Hypertension demand (main durable base)

- Uses are long-cycle and refill-driven.

- Demand stability tends to be higher than for acute indications.

- Forecast risk comes from:

- substitution to other antihypertensives,

- formulary preference shifts,

- generic pricing resets.

PTSD-related use (variable component)

- Prazosin has long been used for PTSD-associated nightmares/sleep disruption, with ongoing practice variability by clinician and payer.

- Forecast sensitivity is higher because:

- labeling and guideline changes affect prescribing,

- payor coverage and prior authorization can swing utilization.

When does prazosin face generic entry risk or supply disruptions, and what are the price consequences?

Featured snippet answer: For prazosin, the dominant risk is not “new exclusivity loss” but recurring generic manufacturing and pricing dynamics (supply constraints, shortages, and ASP erosion from additional entrants).

Supply disruption scenarios that impact revenue

- Shortages: can lift near-term ASP while volume may fall due to allocation.

- Releases: can drive ASP down quickly with stable or rising units.

- Formulary switching: can shift market share among generics without changing total class volume.

Price mechanics to model

A robust projection typically uses:

- Unit demand trend (market size in tablets)

- Weighted ASP erosion (price per tablet)

- Mix shifts by strength and NDC

What does the FDA regulatory status imply for prazosin sales growth?

Featured snippet answer: FDA status for an off-patent generic product primarily affects listing and manufacturing compliance, not demand growth.

Key regulatory elements affecting marketability

- Continued CGMP compliance and quality system stability.

- NDA-to-ANDA lineage and manufacturing site changes that can cause temporary distribution variability.

- Post-marketing safety communications can affect prescribing even for generics, though major class-level effects are uncommon for prazosin specifically.

What is the Orange Book status of prazosin, and what patents protect the drug?

Featured snippet answer: Prazosin is not expected to have meaningful current Orange Book exclusivities covering broad oral immediate-release sales, given its long market history; the practical market risk is generics rather than patent barriers.

What to map for litigation and blocking patents (if building a legal risk profile)

- Current Orange Book entries tied to:

- formulation enhancements (if any),

- method-of-use (if any),

- exclusivity periods (usually historical).

- Then tie each to:

- ANDA paragraph (I/II/III/IV),

- settlement history,

- current listed labels.

(No Orange Book extraction was provided in the prompt, so this cannot be completed with hard patent numbers and dates.)

How many patents cover prazosin formulations and methods of use, and which assignees matter?

Featured snippet answer: The patent landscape for prazosin is expected to be sparse for new commercial leverage because the molecule is established and generic competition is entrenched.

Patent estate mapping needed for a complete answer

To quantify “how many patents” and “which assignees,” the analysis requires:

- Orange Book patent listing capture,

- full-text and family analysis (INPADOC/CPC),

- prosecution timelines for continuation families.

(No patent listing data or source corpus was provided, so a numbered count and assignee list cannot be produced.)

What prazosin patent litigation or settlements affect generic launch timing?

Featured snippet answer: For an established generic drug, litigation typically affects narrow timing windows for specific ANDA products, not the overall market structure.

What to measure in a litigation-driven model

- Case docket outcomes tied to specific ANDAs/NDCs.

- Settlement terms (launch date triggers, design-arounds).

- Consent decrees or supply commitments.

(No docket/case data was provided in the prompt, so this cannot be quantified.)

How does prazosin compare with other alpha-1 blockers for competitive substitution and revenue risk?

Featured snippet answer: Revenue risk is dominated by substitution to other agents that may have stronger evidence, tolerability profiles, or preferred formulary positioning.

Class-level competitors to include in a forecast

- Silodosin

- Tamsulosin

- Terazosin

- Doxazosin

- Alfuzosin (where clinically relevant)

Substitution dynamics

- If competing drugs have:

- better tolerability,

- once-daily convenience,

- stronger guideline adherence, then prazosin can lose units even if total alpha-1 blocker demand is stable.

What are the most important formulation and manufacturing/IP barriers for prazosin?

Featured snippet answer: For oral immediate-release prazosin, manufacturing/IP barriers are typically compliance and bioequivalence economics rather than proprietary formulation.

Practical barriers that affect market share

- Bioequivalence performance history by strength

- Sourcing of API and excipient supply chain

- Capacity stability and distribution reach

- Pharmacovigilance and complaint management costs

Regional sales projections: US vs EU vs UK vs Canada vs other markets

Featured snippet answer: Global revenue tracks payer behavior and generic penetration more than it tracks clinical trial-driven growth.

Country-level drivers

- US: retail demand plus institutional utilization; pricing compression from multi-ANDA supply.

- EU/UK: reimbursement and tendering can cause sharp ASP shifts; utilization tends to be stable once generic penetration is high.

- Canada and other OECD markets: similar dynamics with different tendering intensity.

(Quantified regional forecasts require market datasets or claims/wholesaler data, which were not provided.)

Sales forecast scenarios for prazosin: base, bull, bear

Featured snippet answer: A defensible model for prazosin uses a unit-driven baseline with ASP erosion as the main downside/upside lever.

Scenario framework (how to build projections)

- Base case: flat-to-slight unit growth (population and refill continuity) offset by ongoing ASP erosion from generic price resets.

- Bull case: limited ASP erosion (fewer effective competitors or temporary supply tightness) plus stable off-label usage.

- Bear case: stronger ASP erosion from additional low-price supply plus substitution within alpha-1 blocker class.

(A numeric forecast cannot be produced without starting market size, unit volumes, or ASP baselines.)

Key takeaways

- Prazosin is a mature, generics-dominated product where revenue is driven by unit demand continuity and ongoing ASP compression rather than patent-led product lifecycle expansion.

- Forecasting should be modeled at the NDC/strength level with weighted ASP trends and substitution within the alpha-1 blocker class.

- Patent and litigation impacts, if any, are likely narrow to specific ANDAs and do not generally change total market structure for decades-old molecules.

FAQs

- How do I forecast prazosin sales if I only have NDC-level unit data? Convert units to value using weighted ASP by strength and apply scenario-based ASP erosion rates informed by observed historical price resets.

- What utilization metrics best predict prazosin demand stability? Prescription counts and long-cycle refill persistence in retail plus institutional order cadence.

- Which countries are most sensitive to generics pricing tendering for prazosin? Markets where reimbursement uses tender-based mechanisms and frequent price renegotiations.

- How should prazosin be modeled versus other alpha-1 blockers in payer formularies? Use share-of-class modeling with substitution probabilities based on formulary preference and dosing convenience.

- What is the biggest commercial risk for prazosin revenue in the next 3–5 years? Sustained ASP erosion from competitive generic pricing plus substitution to preferred alpha-1 blocker agents.

References

(No citations were provided or extractable from the prompt.)

More… ↓