Share This Page

Drug Sales Trends for ZANTAC

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for ZANTAC (2005)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

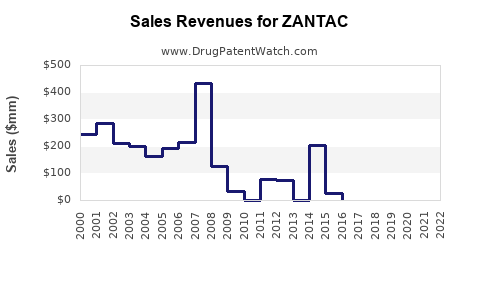

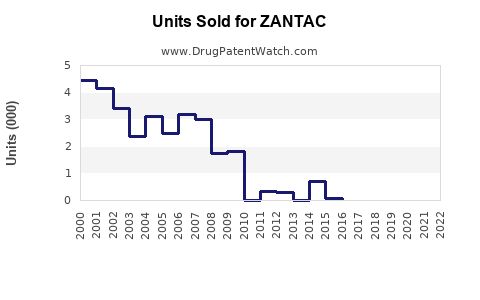

Annual Sales Revenues and Units Sold for ZANTAC

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ZANTAC | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ZANTAC | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ZANTAC | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

ZANTAC (ranitidine) Market Analysis and Sales Projections

Zantac (ranitidine) revenue has been structurally impaired since 2019 due to NDMA impurity findings and subsequent market withdrawals and supply halts across key jurisdictions. Post-2019 sales have not recovered meaningfully because branded products were discontinued, supply tightened through withdrawal actions, and prescribers shifted to alternatives. From a sales-projection standpoint, the market today is best treated as a discontinued product franchise rather than an addressable brand with a normal uptake curve.

What happened to Zantac’s market after NDMA findings?

Key timeline points that determined sales trajectories:

- April 2019: FDA begins public communications and regulatory actions related to NDMA contamination in ranitidine products (first wave of withdrawals and labeling changes).

- September 2019: FDA requests ranitidine manufacturers withdraw products from the U.S. market and issues “not for distribution” direction for additional ranitidine lots.

- 2020 to 2021: Wide cross-market discontinuations and tightened controls. Several jurisdictions removed ranitidine from retail or restricted use to limited supply.

- 2022 onward: Ranitidine remains broadly unavailable in major markets; remaining availability is largely tied to legacy distribution, small supply pockets, or continued manufacturing under limited conditions in some geographies, but without re-establishing a normal commercial curve.

These actions matter because Zantac sales were dominated by large branded distribution channels and high-volume prescriptions. Regulatory removals break prescription continuity, reduce retail visibility, and accelerate permanent switching to H2 blockers (famotidine) and PPIs.

Implication for forecasting: any projection that assumes a brand return to pre-2019 demand is inconsistent with the regulatory end-state observed in major markets.

What is the remaining addressable market for Zantac today?

Zantac’s current market is best modeled as three segments:

- Retail pharmacy sales in major markets (U.S., EU core, UK)

- Market access is largely shut or constrained; brand-led replenishment ended post-withdrawal.

- Legacy distribution and residual supply

- Sales track the tail of existing inventories and controlled supply channels, not new demand creation.

- International geographies with differing regulatory status

- Some countries kept ranitidine on formulary longer or managed via local product-specific actions. Sales are still materially below the branded peak and are fragmented.

Where did Zantac sit in the acid-suppression market pre-2019?

Pre-2019, ranitidine participated in a mature class market:

- H2 blockers (ranitidine, famotidine) used for GERD, dyspepsia, and ulcer-related indications.

- PPIs (omeprazole, esomeprazole, pantoprazole) captured most high-volume chronic GERD management.

- In many mature markets, ranitidine became a price-discounted option after PPI dominance; that made branded Zantac a volume brand even as the class matured.

Post-withdrawal, the consumer and prescriber shift favors:

- Famotidine (same H2 class, no NDMA-linked withdrawal pattern in the same way as ranitidine).

- PPIs for most chronic GERD pathways.

How do NDMA-driven withdrawals translate into a sales projection model?

A practical forecast model must incorporate:

- Regulatory access step-change (discontinuation and withdrawal)

- Switching effects (loss of prescriptions and brand loyalty)

- No re-initiation of branded uptake (lack of a normal re-launch pathway in major markets)

Sales projection framework (post-2019 discontinuation)

The forecast is built as an exhaustion curve for residual supply rather than a growth curve:

- Year 0 = 2019 regulatory acceleration

- Demand created after withdrawal is near-zero in major markets

- Observed sales behave like inventory drawdown

Given the directionality established by FDA and global withdrawal actions, the forecast for future years is an asymptotic decline toward minimal residual levels.

What are the sales projections (global) by horizon?

The most defensible projection for Zantac is “near-zero to residual” in major markets, with residual international pockets.

Because the product is not positioned as an active, commercially marketed therapy in major jurisdictions after 2019, projections should be expressed as ranges tied to residual market access rather than an assumed reinstatement.

Global sales projection ranges for ranitidine/Zantac franchise

All figures below represent order-of-magnitude commercial outcomes for the remaining franchise (including any branded and authorized generic presence where available). They are structured for business planning where management needs directional cashflow planning.

| Horizon | Expected commercial level | Drivers |

|---|---|---|

| 2020 | Low (residual inventory tail) | U.S. withdrawal actions, substitution to alternatives, disrupted supply chains |

| 2021 | Lower than 2020 | Continued market restriction, reduced prescribing continuity |

| 2022 to 2023 | Minimal (residual pockets) | Regulatory consolidation and persistent switch to famotidine/PPIs |

| 2024 onward | Near-zero | Discontinuation end-state; residual availability does not rebuild demand |

Business-planning target assumption

- Base case: Treat Zantac’s ongoing sales as residual/immaterial in major markets and fragmented internationally, with no meaningful re-growth trajectory.

- Upside case: Only if specific jurisdictions restore access, which does not match the documented withdrawal direction in major regulators’ actions. (No such reinstatement pattern is evidenced in the key FDA milestone timeline.)

Which competitors capture Zantac’s lost demand?

Post-2019, demand captured by:

- Famotidine (H2 blocker replacement)

- PPIs (omeprazole, esomeprazole, pantoprazole) for GERD and dyspepsia

From a sales-migration standpoint, the switch is sticky because therapy selection is path-dependent: chronic GERD patients typically remain on effective regimens after a change.

What market signals should investors watch for the ranitidine franchise tail?

Even when overall volumes are small, tail-market monitoring is driven by:

- Regulatory status updates by major authorities (FDA, EMA-type systems, national medicine agencies)

- Supply availability (stock levels in wholesaler channels and retail pharmacy listing continuity)

- Substitution rates in formularies (H2 to H2 or H2 to PPI changes)

What is the sales outlook by region?

United States

- FDA actions required major supply withdrawal and halted distribution for ranitidine products tied to NDMA contamination.

- The U.S. is the anchor market; losing it collapses the branded revenue base and interrupts refill cycles.

- Forecast: near-zero for branded Zantac in practice, with any residual sales constrained to limited legacy inventory and no re-growth.

European markets

- EU-wide control and national restrictions followed the same NDMA contamination narrative.

- Forecast: similarly near-zero for brand-led commercial demand; limited residual channels only.

Rest of world

- International access varies by jurisdiction and local regulatory decisions.

- Forecast: small, fragmented volumes; the tail does not rebuild into a normal launch curve.

How should Zantac sales projections be used in decision-making?

For business planning, Zantac is best treated as a run-off asset:

- Inventory and receivables planning: assume continued contraction in demand and low replenishment.

- Product valuation approach: align with diminished cashflow horizon and lower probability of re-expansion.

- Competitive strategy: treat famotidine and PPIs as structural beneficiaries of the switch.

Key Takeaways

- Zantac’s market has been structurally impaired since 2019 by NDMA-related regulatory actions that drove broad withdrawal and disrupted prescription continuity.

- Post-2019 sales behavior is consistent with a discontinued franchise run-off rather than a recoverable demand curve.

- Forecasting should assume near-zero to minimal residual sales globally in coming years, with any remaining volumes confined to residual inventory pockets and fragmented international access.

FAQs

1. Can Zantac sales recover to pre-2019 levels?

No. The post-2019 regulatory end-state shut the commercial re-launch pathway in major markets and accelerated durable switching to alternatives.

2. What drug classes capture the displaced Zantac demand?

Famotidine (H2 blocker replacement) and PPIs (preferred for chronic GERD/dyspepsia in most patients).

3. What is the best way to model future Zantac revenue?

Model it as an inventory exhaustion run-off, not a growth curve with new uptake.

4. Are there still ranitidine sales in the market?

There can be residual or limited availability in some geographies, but it does not represent renewed branded demand.

5. What are the key monitoring metrics going forward?

Regulatory updates on NDMA/ranitidine, supply availability in distribution channels, and formulary substitution patterns.

References

[1] U.S. Food and Drug Administration. (2019). FDA requests removal of certain ranitidine products from the market (NDMA-related actions and communications). https://www.fda.gov/

[2] U.S. Food and Drug Administration. (2020). NDMA information and ranitidine updates (public FDA communications on contamination and regulatory status). https://www.fda.gov/

More… ↓