Share This Page

Drug Sales Trends for URSODIOL

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for URSODIOL (2005)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

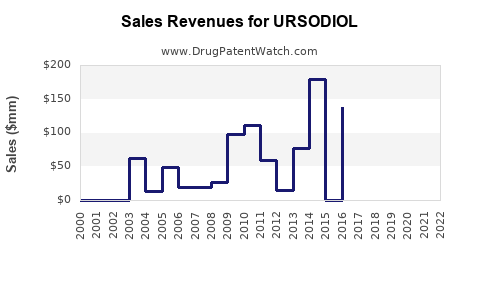

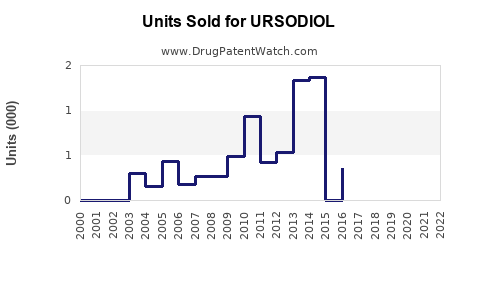

Annual Sales Revenues and Units Sold for URSODIOL

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| URSODIOL | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| URSODIOL | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| URSODIOL | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| URSODIOL | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| URSODIOL | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

URSODIOL PATENT ANALYSIS: MARKET PROJECTIONS AND KEY COMPETITIVE LANDSCAPE

Ursodiol, a bile acid used to dissolve certain types of gallstones and treat primary biliary cholangitis (PBC), faces a dynamic patent landscape and evolving market conditions. While established as a first-line treatment for PBC, its market is influenced by the expiration of key patents, the emergence of generic competition, and ongoing research into novel therapeutic approaches. Current market analysis projects moderate growth, driven by increasing PBC diagnoses and the drug's established efficacy, but tempered by price erosion from generics.

WHAT IS THE CURRENT PATENT STATUS OF URSODIOL?

The patent landscape for ursodiol is characterized by the expiration of foundational composition of matter patents. These original patents, which claimed the ursodiol molecule itself, have long expired, opening the door for generic manufacturers.

- Key Expiration Dates: Original patents covering ursodiol as a chemical entity have expired globally. For example, patents such as U.S. Patent No. 3,542,841, which was among the early patents for chenodeoxycholic acid derivatives like ursodiol, expired decades ago.

- Subsequent Patents: While the primary patents are expired, there are secondary patents that may cover specific formulations, methods of use, or manufacturing processes. These can include:

- Formulation Patents: These patents claim specific dosage forms (e.g., extended-release tablets, liquid suspensions) designed to improve patient compliance, bioavailability, or reduce side effects.

- Method of Use Patents: These patents may cover the use of ursodiol for treating specific conditions or patient populations not initially covered by original approvals. For PBC, this includes established use for liver protection and symptom management.

- Manufacturing Process Patents: Patents related to novel or improved synthesis routes for ursodiol can provide a competitive advantage by reducing costs or improving purity.

- Generic Entry: With the expiration of primary patents, numerous generic versions of ursodiol have entered the market. This has led to significant price competition and a reduction in market share for branded products unless they possess strong secondary patent protection or proprietary formulations.

- Orphan Drug Exclusivity: In some regions, ursodiol may have benefited from orphan drug exclusivity for specific indications, providing a period of market protection separate from patent status. For PBC, this has historically been a significant factor.

WHO ARE THE MAJOR PLAYERS IN THE URSODIOL MARKET?

The ursodiol market includes both branded and generic manufacturers, with branded products often holding a premium due to established quality, supply chain reliability, and potentially differentiated formulations.

- Branded Manufacturers:

- Takeda Pharmaceuticals (through its acquisition of Shire): Historically a major player with Actigall® (ursodiol) in the U.S. and Urso® (ursodeoxycholic acid) in other regions. Takeda continues to market ursodiol for approved indications.

- Other Regional Brands: Various pharmaceutical companies market ursodiol under different brand names in different countries, often with strong regional market presence.

- Generic Manufacturers: The market is highly competitive with a substantial number of generic manufacturers producing ursodiol. Key generic players include:

- Teva Pharmaceuticals

- Mylan (now Viatris)

- Sun Pharmaceutical Industries

- Dr. Reddy's Laboratories

- Apotex

- Perrigo

- Market Share Dynamics: Branded products, while historically dominant, now face significant competition from generics. The market share of branded ursodiol is often contingent on the specific indication, the presence of unique formulations, and the pricing strategies employed by the manufacturer. Generic entry typically leads to a rapid decline in pricing and market share for branded alternatives once exclusivity expires.

WHAT ARE THE CURRENT MARKET SIZE AND SALES PROJECTIONS FOR URSODIOL?

The global market for ursodiol is substantial, driven by its role in managing chronic liver diseases like PBC. Projections indicate moderate but steady growth, influenced by demographic shifts, diagnostic advancements, and the competitive generics landscape.

- Current Market Size: The global ursodiol market was valued at approximately USD 800 million to USD 1.2 billion in 2023. This figure encompasses both branded and generic sales across all approved indications.

- PBC Treatment Dominance: The primary driver of ursodiol sales is its use in treating primary biliary cholangitis (PBC). Global prevalence of PBC is estimated to be between 50 and 250 per 100,000 people, with a higher incidence in women [1].

- Gallstone Dissolution: While ursodiol is effective for dissolving cholesterol gallstones, its use for this indication has declined relative to other treatment options and surgical interventions.

- Growth Drivers:

- Increasing PBC Diagnoses: Improved awareness and diagnostic capabilities lead to earlier and more frequent diagnoses of PBC, increasing the patient pool requiring treatment.

- Aging Population: The prevalence of liver diseases, including PBC, tends to increase with age.

- Established Efficacy and Safety: Ursodiol has a long-standing track record of safety and efficacy, making it a preferred choice for physicians.

- OEU (Orphan Drug Exclusivity) Extensions: While original patents have expired, potential extensions or new method-of-use patents for specific patient subgroups or expanded indications could influence market dynamics, though less common for established drugs.

- Growth Restraints:

- Generic Competition and Price Erosion: The widespread availability of generic ursodiol has significantly reduced average selling prices (ASPs), limiting revenue growth.

- Emergence of New Therapies: While ursodiol remains a cornerstone for PBC, research into novel treatments targeting different pathways of liver disease progression may eventually offer alternatives, though no direct competitors have fully displaced ursodiol for first-line PBC treatment.

- Limited Efficacy in Advanced Disease: Ursodiol's efficacy is primarily in slowing disease progression rather than reversing established fibrosis or cirrhosis.

- Sales Projections (2024-2028):

- Compound Annual Growth Rate (CAGR): The market is projected to grow at a CAGR of 3% to 5% over the next five years.

- Projected Market Value: By 2028, the global ursodiol market is expected to reach between USD 950 million and USD 1.35 billion.

- Regional Variations: Growth rates will vary by region, with developed markets like North America and Europe showing more stable demand due to established healthcare systems and higher PBC prevalence, while emerging markets may see faster percentage growth due to increasing access to diagnostics and treatment.

WHAT ARE THE REGULATORY AND CLINICAL GUIDELINES FOR URSODIOL USE?

Regulatory approvals and clinical guidelines dictate the approved uses, dosages, and monitoring requirements for ursodiol, shaping its market accessibility and physician prescribing habits.

- FDA Approvals (United States):

- Primary Biliary Cholangitis (PBC): Ursodiol is approved for the treatment of PBC. The typical dosage for adults is 13-15 mg/kg/day divided into two to four doses.

- Dissolution of Radioluscent Cholesterol Gallstones: Approved for patients with symptomatic, radioluscent cholesterol gallstones for whom surgery is not a suitable alternative. Dosage is typically 8-10 mg/kg/day administered once daily at bedtime.

- Dosage Adjustments: Renal or hepatic impairment may necessitate dosage adjustments.

- EMA Approvals (European Union): Similar indications and dosage regimens are approved in EU member states, often under the name ursodeoxycholic acid.

- Clinical Guidelines (e.g., AASLD, EASL):

- American Association for the Study of Liver Diseases (AASLD) and European Association for the Study of the Liver (EASL) Guidelines for PBC: These organizations recommend ursodiol as the first-line pharmacologic treatment for PBC. The primary goal is to improve liver biochemistry tests and slow disease progression.

- Monitoring: Patients on ursodiol require regular monitoring of liver function tests (LFTs) to assess treatment response and detect potential adverse effects. Guidelines typically recommend LFT monitoring every six months initially, then annually.

- Treatment Response: Patients are assessed for biochemical response (normalization or significant improvement of LFTs) and symptom improvement. Non-responders may require consideration of alternative therapies, such as obeticholic acid or combination therapy in later stages of the disease.

- Adverse Events: Common side effects include diarrhea, nausea, and abdominal discomfort. Serious adverse events are rare but can include hepatotoxicity in rare instances.

- Exclusivity and Market Protection: While patent protection is the primary driver of market exclusivity for new drugs, orphan drug designations can provide additional periods of market exclusivity (e.g., 7 years in the U.S., 10 years in the EU) for approved orphan indications. For ursodiol in PBC, this has played a significant role.

WHAT ARE THE KEY COMPETITIVE THREATS AND OPPORTUNITIES FOR URSODIOL?

The future of ursodiol is shaped by the constant interplay of therapeutic innovation, market access, and economic pressures.

- Competitive Threats:

- Generic Price Wars: The most significant threat is ongoing price erosion due to a large number of generic manufacturers, leading to compressed profit margins for all market participants.

- Emergence of Novel PBC Therapies: Research into new drugs targeting different mechanisms of liver disease in PBC (e.g., PPAR agonists, FXR agonists) could eventually displace ursodiol as first-line therapy, particularly for non-responders.

- Alternative Gallstone Treatments: For gallstone dissolution, laparoscopic cholecystectomy remains the definitive treatment, and newer non-surgical options continue to emerge.

- Stricter Reimbursement Policies: Payers may increasingly scrutinize the value proposition of ursodiol, especially in the face of generic availability and alternative treatments, potentially leading to stricter formulary placement or prior authorization requirements.

- Opportunities:

- Increased Diagnosis and Awareness: Continued efforts to raise awareness of PBC and improve diagnostic tools will expand the patient population benefiting from ursodiol.

- New Formulations: Development of novel delivery systems (e.g., extended-release, combination therapies) could re-establish market differentiation and potentially secure new patent protection, although this is challenging for an older molecule.

- Off-Label Use and Repurposing: While strictly regulated, ongoing research might uncover new therapeutic benefits for ursodiol in other conditions, which could lead to new indications and market expansion through the patenting of new methods of use.

- Emerging Markets: Growth potential exists in developing regions where access to advanced diagnostics and treatments is expanding, and ursodiol represents an affordable and effective option.

- Fixed-Dose Combinations: The development of fixed-dose combinations of ursodiol with other agents for PBC or other liver conditions could create new intellectual property and market opportunities.

KEY TAKEAWAYS

- Ursodiol's foundational patents have expired, leading to a highly competitive generic market that significantly influences pricing and revenue.

- The primary market driver for ursodiol is its established role as a first-line therapy for primary biliary cholangitis (PBC).

- The global ursodiol market is projected to grow moderately, between 3% and 5% CAGR, reaching approximately USD 950 million to USD 1.35 billion by 2028.

- Major global players include Takeda (branded) and a broad spectrum of generic manufacturers such as Teva, Viatris, and Sun Pharma.

- Regulatory approvals and clinical guidelines from bodies like the FDA, EMA, AASLD, and EASL define ursodiol's therapeutic use, primarily for PBC and gallstone dissolution, emphasizing monitoring and established efficacy.

- Key competitive threats include intense generic price competition and the potential emergence of novel PBC therapies. Opportunities lie in expanding diagnostics, emerging markets, and potentially new formulations or combinations.

FAQS

1. What is the projected market size for ursodiol in 2025, and what factors will primarily influence this figure?

The projected market size for ursodiol in 2025 is estimated to be between USD 860 million and USD 930 million. This figure will be primarily influenced by the continued prevalence of PBC diagnoses, the ongoing price pressure from generic competition, and the stable demand for its established therapeutic benefits.

2. Are there any significant new patent applications filed for ursodiol that could impact its future market exclusivity?

While primary composition of matter patents have long expired, companies may file patents for novel formulations, manufacturing processes, or new methods of use. A review of patent databases indicates ongoing, albeit limited, filings for process improvements and specific pharmaceutical compositions designed to enhance delivery or patient compliance, but these are unlikely to create broad new market exclusivity periods comparable to original drug patents.

3. How does the pricing of generic ursodiol compare to branded versions in major markets?

In major markets like the U.S. and EU, generic ursodiol is typically priced 50% to 80% lower than branded ursodiol. This significant price difference is a direct result of the increased competition from multiple generic manufacturers following patent expirations.

4. What is the anticipated impact of emerging novel therapies for Primary Biliary Cholangitis on the ursodiol market share?

Emerging novel therapies for PBC, such as obeticholic acid and potential future drug classes targeting different pathways, are expected to impact ursodiol's market share, particularly for patients who are non-responders to ursodiol or have more advanced disease. While ursodiol is likely to remain a first-line treatment due to its established profile and cost-effectiveness, these newer agents may capture a growing segment of the market, especially in later-stage disease management.

5. Which geographic regions are expected to exhibit the highest growth rates for ursodiol sales, and why?

The highest growth rates for ursodiol sales are anticipated in emerging markets within Asia-Pacific and Latin America. This is attributed to increasing healthcare infrastructure, improving diagnostic capabilities leading to higher PBC detection rates, and a growing middle class with better access to essential medications. Developed markets in North America and Europe are expected to show more stable, mature growth.

CITATIONS

[1] European Association for the Study of the Liver (EASL). (2017). EASL Clinical Practice Guideline: Management of cholestatic liver diseases. Journal of Hepatology, 67(2), 399-417.

More… ↓