Last updated: February 12, 2026

What is KEPPRA and what is its market status?

KEPPRA (levetiracetam) is an antiepileptic drug indicated for the treatment of seizures in adults and children over 1 month old. It was developed by UCB Pharma and approved by the FDA in 2008. KEPPRA belongs to the pyrrolidine class of anticonvulsants and is used both as monotherapy and adjunct therapy in epilepsy management. It has a metabolite profile that offers advantages such as low drug interaction potential and a favorable side-effect profile, making it a widely prescribed medication globally.

How large is the current KEPPRA market?

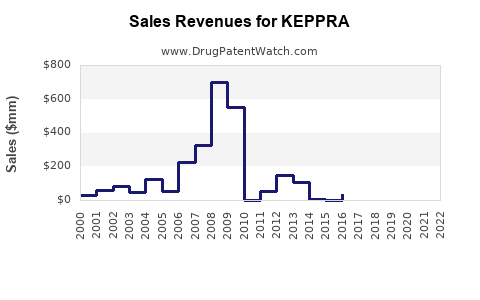

Global sales of KEPPRA reached approximately $1.7 billion in 2022, according to IQVIA data. The drug maintains a dominant position in the epilepsy treatment segment, with high prescription rates in North America, Europe, and parts of Asia.

What are the key factors influencing KEPPRA sales?

- Market penetration: KEPPRA's established use in epilepsy treatment supports steady demand, with over 10 million prescriptions filled annually worldwide.

- Competitor landscape: Several newer antiepileptic drugs (AEDs) like Briviact (brivaracetam), Vimpax (lacosamide), and Epidiolex (cannabidiol) pose competitive pressures, especially in specific patient subgroups.

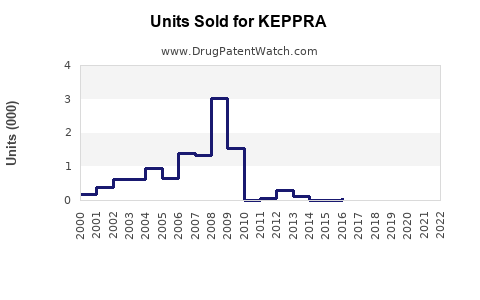

- Patent status: UCB Pharma's patent for KEPPRA expired in 2015 in the US and in various markets globally. Generics entered the market afterward, impacting sales volumes.

- Pricing and reimbursement: KEPPRA remains partly protected by market exclusivity in some regions, with generic competition exerting downward pressure on prices.

- Regulatory and clinical updates: Ongoing clinical trials and regulatory updates for formulations or new indications can influence market dynamics.

What are future sales projections for KEPPRA?

Projections indicate a steady decline in KEPPRA sales, driven by generic competition and market saturation. Global sales are expected to decrease at an average annual rate of 3-5% over the next five years, reaching approximately $1.3 billion by 2028.

Key drivers of this decline include:

- Patent expirations: Continued erosion of brand sales due to generics.

- Market share shift: Increased prescriptions for newer AEDs with different mechanisms of action.

- Emerging therapies: Development of targeted treatments for specific epilepsy syndromes that may replace traditional AEDs like KEPPRA.

However, sales in emerging markets could offset some declines due to increasing epilepsy prevalence and expanding healthcare access.

How do regional markets compare?

| Region |

2022 Sales (USD million) |

Growth Rate (2022-2028) |

Key Factors |

| North America |

$800 |

-4% annually |

Market saturation, generic competition |

| Europe |

$500 |

-3.5% annually |

Patent expiration, increasing use of generics |

| Asia-Pacific |

$250 |

2% annually |

Expanding healthcare access, rising epilepsy prevalence |

| Rest of World |

$150 |

1% annually |

Market development, lower therapeutic penetration |

What growth opportunities exist?

- New formulations: Extended-release or combination products could recapture some market share.

- New indications: Clinical trials exploring KEPPRA for bipolar disorder or neuropathic pain might expand its use.

- Generic market share: Market entry of generics in developing regions provides access to new customers and volume growth prospects.

What is the competitive landscape?

Besides KEPPRA, main competitors are:

- Briviact (brivaracetam): Similar mechanism with improved tolerability.

- Vimpax (lacosamide): Used for partial-onset seizures.

- Epidiolex (cannabidiol): Approved for specific epilepsy syndromes like Lennox-Gastaut and Dravet.

Briviact gained market share post-launch in 2016 due to better tolerability and ease of dosing, providing direct competition in the same patient population.

How will pricing affect KEPPRA sales?

Pricing strategies are key to maintaining revenue:

- Original KEPPRA pricing was 20-30% higher than generics.

- Once patent expired, price discounts of 50% or more accelerated sales declines.

- Reimbursement policies and formularies increasingly favor generics, further pressuring brand sales.

What are the implications for stakeholders?

Investors should anticipate declining revenues from KEPPRA in the next 3-5 years, with opportunities for value capture via pipeline developments or acquisition of rights to newer therapies. R&D must focus on unmet needs in epilepsy and related neurological disorders.

Key Takeaways

- KEPPRA is a mature epilepsy drug with $1.7 billion in global sales in 2022.

- Patent expirations and generic competition are driving sales decline at 3-5% annually.

- Regions differ, with North America and Europe experiencing sharper declines than Asia-Pacific.

- The drug's future depends on new formulations, expanded indications, and market penetration in emerging markets.

- Competition from newer AEDs like Briviact and Vimpax affects KEPPRA's market share.

FAQs

-

When did KEPPRA lose patent protection?

In the US, KEPPRA's patent expired in 2015; other markets varied between 2014-2017.

-

What are the main competitors of KEPPRA?

Briviact, Vimpax, and Epidiolex are primary competitors targeting similar epilepsy indications.

-

Are there new indications for KEPPRA in clinical trials?

Limited clinical trials are exploring KEPPRA's potential for bipolar disorder and neuropathic pain, but these are not yet approved or commercialized.

-

What is the outlook for KEPPRA's market share?

Expect gradual erosion due to generic competition, with potential stabilization through new formulations or expanded uses.

-

How does KEPPRA compare economically to newer therapies?

Original KEPPRA was priced higher than generics; newer AEDs like Briviact are priced similarly but claim better tolerability, influencing prescription patterns.