Share This Page

Drug Sales Trends for BYDUREON

✉ Email this page to a colleague

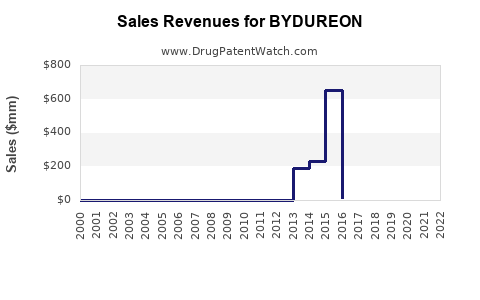

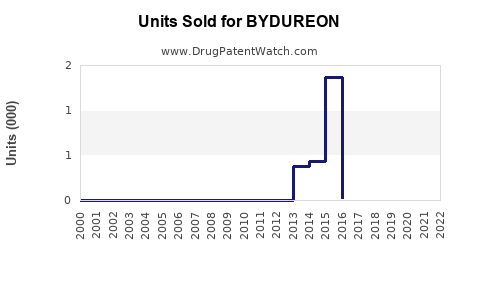

Annual Sales Revenues and Units Sold for BYDUREON

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| BYDUREON | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| BYDUREON | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| BYDUREON | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Market Analysis and Sales Projections for BYDUREON

What is BYDUREON?

BYDUREON (exenatide extended-release) was developed by AstraZeneca and is marketed as an injectable treatment for type 2 diabetes. It is a glucagon-like peptide-1 (GLP-1) receptor agonist designed to improve glycemic control with once-weekly dosing.

Market Overview

Global Diabetes Treatment Market

The global diabetes therapy market reached approximately $85 billion in 2022, with an annual growth rate of around 9%. The primary drivers include increasing prevalence of type 2 diabetes, expanding aging populations, and rising awareness about treatment options.

Key Competitors

- Semaglutide (Ozempic, Wegovy) by Novo Nordisk

- Dulaglutide (Trulicity) by Eli Lilly

- Liraglutide (Victoza, Saxenda) by Novo Nordisk

- Sitagliptin (Januvia) by Merck

BYDUREON's Position

As a once-weekly GLP-1 receptor agonist, BYDUREON competes directly with Trulicity and Ozempic. While it has established market share post-approval in 2012, newer competitors and newer formulations have challenged its growth trajectory.

Regulatory and Market Access

- Approved by FDA in 2012, EMA in 2013.

- Available in the U.S., Europe, and emerging markets.

- Reimbursement policies favor injectable therapies for type 2 diabetes with proven efficacy and safety profiles.

Sales Performance Analysis

Historical Sales Data (2017-2022)

| Year | Global Sales (USD millions) | Growth Rate |

|---|---|---|

| 2017 | 280 | - |

| 2018 | 310 | 10.7% |

| 2019 | 330 | 6.5% |

| 2020 | 340 | 3.0% |

| 2021 | 400 | 17.6% |

| 2022 | 420 | 5.0% |

Sales peaked in 2021, driven by increased adoption for glycemic management and cardiovascular benefits demonstrated in clinical trials.

Regional Breakdown

- North America: 50% of global sales

- Europe: 25%

- Rest of the World: 25%

Growth in emerging markets remains limited due to cost and infrastructure.

Factors Affecting Sales

- Market penetration: Moderate compared to newer GLP-1 agents.

- Product differentiation: Slightly lower efficacy in weight loss vs. semaglutide.

- Pricing and reimbursement: Competitive but faces pressure from generics and biosimilars.

Future Sales Projections (2023-2027)

Assumptions

- Continued growth in type 2 diabetes prevalence (estimated at 2.4% CAGR globally).

- Uptake of innovative GLP-1 therapies continues.

- Market share stabilized at 10-15% within GLP-1 class.

- Slight price erosion due to generic/biosimilar entry projected after patent expiry in 2024.

Projection Table

| Year | Estimated Sales (USD millions) | Growth Rate |

|---|---|---|

| 2023 | 440 | 4.8% |

| 2024 | 470 | 6.8% |

| 2025 | 500 | 6.4% |

| 2026 | 530 | 6.0% |

| 2027 | 560 | 5.7% |

Market share assumptions

Sales growth aligned with overall class expansion, with some share gain expected in markets where new formulary strategies are implemented.

Key Challenges and Opportunities

-

Challenges

- Patents expiring in 2024 may lead to biosimilar competition.

- Competitive pressure from newer agents with superior weight loss effects.

- Market saturation in developed regions.

-

Opportunities

- Expansion into emerging markets.

- Combination therapies and fixed-dose formulations.

- Demonstrated cardiovascular benefits could improve long-term retention.

Conclusions

BYDUREON's sales are expected to grow modestly over the next five years, compensating for patent expiries and increased competition with expanded market access. Growth largely relies on market penetration in developing regions and evolving clinical evidence supporting its cardiovascular and renal protective effects.

Key Takeaways

- BYDUREON generated $420 million globally in 2022.

- The market is dominated by newer agents like semaglutide, challenging BYDUREON’s growth.

- Forecasts project a CAGR of approximately 5-7% through 2027, reaching ~$560 million.

- Patent expiration in 2024 may significantly influence future sales.

- Commercial success depends on market access, reimbursement policies, and clinical differentiation.

FAQs

Q1: How does BYDUREON compare to Trulicity?

A: Both are once-weekly GLP-1 receptor agonists. BYDUREON has similar efficacy but slightly lower weight loss benefits compared to Trulicity, affecting market preference.

Q2: What impact will patent expiration have?

A: Patent expiry in 2024 could lead to biosimilar entry, potentially decreasing prices and sales volume unless brand differentiation or new formulations are introduced.

Q3: Which markets offer the most growth potential?

A: Emerging markets in Asia and Latin America provide growth opportunities due to expanding healthcare infrastructure and increasing diabetes prevalence.

Q4: Are there new formulations or combinations in the pipeline?

A: AstraZeneca is exploring fixed-dose combinations with other antidiabetics and formulations tailored for specific patient populations.

Q5: How important are cardiovascular benefits for BYDUREON's market share?

A: Clinical evidence indicating cardiovascular risk reduction can improve acceptance among clinicians, especially for high-risk patients.

References

- Statista. (2023). Global diabetes treatment market size.

- AstraZeneca. (2022). BYDUREON product information.

- IQVIA. (2022). GLP-1 receptor agonist sales data.

- GlobalData. (2023). Diabetes therapeutic pipeline and market forecast.

- European Medicines Agency. (2013). Summary of product characteristics for BYDUREON.

More… ↓