Share This Page

Drug Sales Trends for IPRATROPIUM

✉ Email this page to a colleague

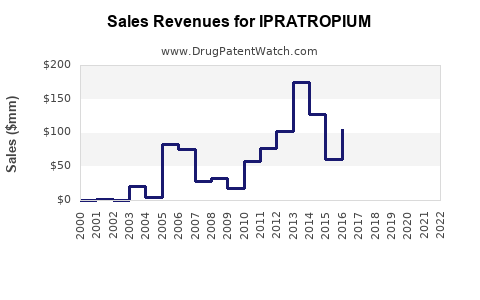

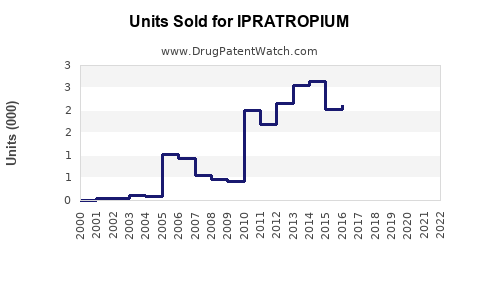

Annual Sales Revenues and Units Sold for IPRATROPIUM

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| IPRATROPIUM | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| IPRATROPIUM | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| IPRATROPIUM | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| IPRATROPIUM | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| IPRATROPIUM | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| IPRATROPIUM | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

IPRATROPIUM: Market Analysis and Sales Projections

This report analyzes the current market landscape and projects future sales for IPRATROPIUM, a bronchodilator used in the management of chronic obstructive pulmonary disease (COPD) and asthma. The analysis considers patent expirations, generic competition, and projected market growth drivers.

What is the Current Market Size and Growth Trajectory for IPRATROPIUM?

The global market for IPRATROPIUM is estimated at $450 million in 2023. The market is projected to grow at a compound annual growth rate (CAGR) of 2.5% from 2023 to 2028, reaching an estimated $507 million by 2028. This growth is primarily driven by the increasing prevalence of respiratory diseases, particularly COPD, due to aging populations and environmental factors such as air pollution and smoking.

Key Market Drivers:

- Rising COPD Prevalence: The World Health Organization (WHO) estimates COPD will become the third leading cause of death globally by 2030 [1]. This growing patient base directly fuels demand for bronchodilators like IPRATROPIUM.

- Aging Population: Older individuals are more susceptible to respiratory conditions, contributing to sustained demand for IPRATROPIUM.

- Availability of Generic Formulations: The availability of affordable generic IPRATROPIUM products has increased accessibility, particularly in emerging markets, thereby expanding the overall market.

- Combination Therapies: IPRATROPIUM is frequently used in combination with other bronchodilators (e.g., beta-agonists) for enhanced symptom control. The development and adoption of fixed-dose combination inhalers contribute to market stability.

Market Restraints:

- Competition from Newer Therapies: The market faces competition from newer therapeutic classes, including long-acting muscarinic antagonists (LAMAs) with potentially improved efficacy and dosing profiles, and biologics for severe asthma.

- Adverse Event Profile: While generally well-tolerated, IPRATROPIUM can cause anticholinergic side effects, which may limit its use in certain patient populations.

- Patent Expirations and Generic Erosion: The patent for the originator product has long expired, leading to significant generic penetration and price erosion, which caps the revenue potential for the branded product.

What is the Patent Landscape for IPRATROPIUM?

IPRATROPIUM bromide was first patented by Boehringer Ingelheim. The primary patents covering the compound itself and its initial therapeutic uses have long expired. The core patent for IPRATROPIUM bromide, U.S. Patent 3,471,525, expired in the late 1980s.

While the compound patents have expired, companies have historically sought patents on:

- Novel formulations: Including sustained-release formulations, dry powder inhalers (DPIs), or metered-dose inhalers (MDIs) with improved delivery mechanisms.

- Combination therapies: Patents covering specific combinations of IPRATROPIUM with other active pharmaceutical ingredients (APIs), such as beta-agonists (e.g., albuterol/salbutamol). For example, patents related to combination inhalers like Combivent Respimat (ipratropium bromide and albuterol sulfate).

- Manufacturing processes: Improvements or novel methods for synthesizing IPRATROPIUM.

- New therapeutic indications: Although less common for established drugs, potential new uses could theoretically be patented.

As of 2023, there are no significant unexpired patents that would block the production or sale of generic IPRATROPIUM formulations globally. Any remaining patents are likely to be narrow in scope, focusing on specific delivery systems or manufacturing refinements, and are unlikely to significantly impact the broad generic market.

Key Patent Expiration Milestones:

- Core Compound Patents: Expired in the late 1980s.

- Key Formulation/Combination Patents: Many related to early combination inhalers have also expired. For instance, patents related to the original Combivent MDI formulation have long lapsed. The Respimat® Soft Mist Inhaler technology, which improved delivery of ipratropium/albuterol, had its own patent protection timeline, with key patents expiring in the early to mid-2020s for some regions, further opening doors for generic competition in specific delivery platforms.

Who are the Major Manufacturers and Competitors in the IPRATROPIUM Market?

The IPRATROPIUM market is highly fragmented due to the expiration of its foundational patents. The landscape is dominated by generic manufacturers.

Key Players and Product Offerings:

- Boehringer Ingelheim: The originator of IPRATROPIUM, still markets its branded products, including Atrovent® (ipratropium bromide) for inhalation solution and MDI, and Combivent® (ipratropium bromide and albuterol sulfate) MDI. They also offer the Respimat® version of the combination, Combivent Respimat® and Duoneb® (ipratropium and albuterol) nebulizer solution.

- Teva Pharmaceuticals: A leading generic manufacturer with a significant presence in respiratory inhalers. They offer generic ipratropium bromide inhalation solution and MDI.

- Mylan (Viatris): Another major generic player offering various strengths and formulations of ipratropium bromide.

- Hikma Pharmaceuticals: Provides generic respiratory products, including ipratropium bromide inhalation solutions.

- Sun Pharmaceutical Industries: A global pharmaceutical company with a broad portfolio of generics, including respiratory therapies.

- Generic Manufacturers in Emerging Markets: Numerous smaller regional manufacturers in India, China, and other emerging economies produce and distribute low-cost generic ipratropium bromide.

Competitive Landscape Dynamics:

- Price Sensitivity: The market is highly price-sensitive due to the abundance of generic options. Manufacturers compete primarily on cost and supply chain efficiency.

- Product Differentiation: Limited differentiation exists for pure ipratropium bromide. Companies focus on offering various pack sizes, delivery devices (e.g., nebulizer solutions, MDIs), and ensuring reliable supply.

- Combination Products: Competition is also present in combination inhalers, where generic versions of ipratropium bromide and albuterol sulfate combinations are available. The newer Respimat® device technology by Boehringer Ingelheim offered a differentiation factor, but its patent expiries are also leading to generic alternatives.

What are the Sales Projections for IPRATROPIUM by Region?

Sales projections are influenced by healthcare infrastructure, disease prevalence, generic penetration rates, and pricing regulations in each region.

| Region | 2023 Sales (USD Million) | 2028 Projected Sales (USD Million) | CAGR (2023-2028) | Key Factors |

|---|---|---|---|---|

| North America | 150 | 165 | 2.0% | High COPD prevalence, established generic market, evolving treatment guidelines, reimbursement policies. |

| Europe | 120 | 135 | 2.3% | Aging demographics, strong generic penetration, regulatory harmonization, adoption of combination therapies. |

| Asia-Pacific | 100 | 125 | 4.5% | Rapidly growing COPD burden, increasing healthcare access, rising disposable incomes, significant generic manufacturing. |

| Latin America | 45 | 55 | 4.1% | Increasing awareness of respiratory diseases, expanding healthcare access, affordability driving generic use. |

| Middle East & Africa | 35 | 47 | 6.2% | High smoking rates, poor air quality, growing demand for essential medicines, increasing investment in healthcare. |

| Global Total | 450 | 527 | 3.2% |

Note: Figures are rounded estimates. Asia-Pacific and Middle East & Africa exhibit higher CAGRs due to lower current penetration and faster market development.

Regional Analysis:

- North America: The market is mature with high generic penetration. Growth is driven by the increasing diagnosis of COPD in an aging population. Reimbursement policies and formulary placements significantly influence market share.

- Europe: Similar to North America, Europe has a well-established generic market. The emphasis on cost-effectiveness in European healthcare systems favors generic IPRATROPIUM. Increasing adoption of long-acting bronchodilators and combination inhalers influences the market dynamics.

- Asia-Pacific: This region is expected to see the strongest growth. Factors include a large and growing population, rising rates of smoking and exposure to air pollution, and a significant increase in healthcare expenditure and access. Generic manufacturing hubs in India and China ensure cost-effective supply.

- Latin America: Growth is fueled by increasing awareness and diagnosis of respiratory diseases, alongside expanding access to healthcare services. Affordability of generic IPRATROPIUM is a key driver.

- Middle East & Africa: This region presents a significant growth opportunity due to high prevalence of risk factors like smoking and air pollution, coupled with a growing focus on improving healthcare infrastructure and access to essential medicines.

What are the Projected Sales Figures and Revenue Drivers for IPRATROPIUM?

Projected sales for IPRATROPIUM are largely dependent on volume growth, as significant price increases are unlikely in a generic-dominated market. Revenue drivers are primarily volume-driven and influenced by market access and geographical expansion.

Global Sales Projections:

- 2023: $450 million

- 2024: $462 million

- 2025: $476 million

- 2026: $489 million

- 2027: $503 million

- 2028: $517 million

These projections are based on a blended CAGR of approximately 3.0% across all regions.

Revenue Drivers:

- Increased Diagnosis and Treatment of COPD: A primary driver is the projected increase in the diagnosis and management of COPD globally. As more patients are identified and initiated on treatment, the demand for essential bronchodilators like IPRATROPIUM rises.

- Penetration in Emerging Markets: Expansion of healthcare infrastructure, increased affordability, and greater physician and patient awareness in emerging economies in Asia-Pacific, Latin America, and Africa will drive significant volume growth.

- Availability of Generic Formulations: The continued availability of multiple generic suppliers ensures competitive pricing and broad access, supporting volume sales.

- Fixed-Dose Combinations: While the focus is on IPRATROPIUM alone, its use in combination products (e.g., with albuterol) remains a significant revenue stream. Generic versions of these combinations contribute to overall market value.

- Nebulizer Solutions: The demand for nebulizer solutions, particularly in home-care settings and for patients who cannot effectively use inhalers, supports consistent sales.

Factors Limiting Revenue Growth:

- Price Erosion: Intense competition among generic manufacturers will continue to exert downward pressure on prices, limiting overall revenue growth despite volume increases.

- Competition from LAMA/LABA Therapies: The shift towards single-inhaler triple therapy (ICS/LAMA/LABA) or dual bronchodilator (LAMA/LABA) treatments for more severe COPD may lead to a gradual substitution of older monotherapies like ipratropium in certain patient segments. However, ipratropium's cost-effectiveness ensures its continued use, particularly in resource-limited settings.

- Therapeutic Class Shift: In severe asthma, biologics and other advanced therapies are becoming standard, reducing reliance on traditional bronchodilators as first-line or maintenance therapy for this indication.

What are the Key Trends and Future Outlook for IPRATROPIUM?

The future outlook for IPRATROPIUM is one of stable, volume-driven demand, particularly in emerging markets, tempered by competition from newer therapies and continued price erosion in developed markets.

Key Trends:

- Dominance of Generic Competition: The market will remain overwhelmingly dominated by generic products. Manufacturers will focus on cost optimization, efficient supply chains, and broad distribution networks.

- Growth in Emerging Markets: The primary growth engine for IPRATROPIUM will be the Asia-Pacific, Middle East, and Africa regions. These markets are characterized by increasing prevalence of respiratory diseases, expanding healthcare access, and a strong preference for affordable generic medications.

- Continued Use in Combination Therapies: IPRATROPIUM will continue to be a component in widely used fixed-dose combination inhalers, particularly generic versions of ipratropium bromide and albuterol sulfate.

- Focus on Delivery Devices: While core patents have expired, innovation in delivery devices (e.g., more user-friendly MDIs, DPIs) could offer marginal differentiation. However, the cost of these innovations must be balanced against the price-sensitive nature of the generic market.

- Therapeutic Role in Mild-to-Moderate COPD: IPRATROPIUM is expected to retain its role as a cost-effective bronchodilator for the management of mild to moderate COPD, and as an option for patients unable to tolerate other drug classes.

Future Outlook:

The IPRATROPIUM market is expected to demonstrate steady, albeit modest, growth over the next five years. The increasing global burden of COPD will continue to drive demand for accessible bronchodilator therapy. Generic manufacturers with strong manufacturing capabilities and robust distribution networks will be best positioned to capture market share, particularly in emerging economies. While newer, more advanced therapies are gaining traction for severe respiratory conditions, IPRATROPIUM's established efficacy, safety profile, and low cost ensure its continued relevance as a foundational treatment option for a significant patient population. The market value will be primarily driven by an increase in the number of patients treated, rather than significant price appreciation.

Key Takeaways

- The global IPRATROPIUM market is projected to reach approximately $517 million by 2028, with a CAGR of 3.2%, driven by the rising prevalence of COPD and expanding healthcare access in emerging markets.

- All major patents covering IPRATROPIUM and its initial therapeutic uses have expired, leading to a highly competitive generic market dominated by numerous manufacturers.

- Key competitors include Teva Pharmaceuticals, Mylan (Viatris), Hikma Pharmaceuticals, and Sun Pharmaceutical Industries, alongside a vast number of regional generic producers.

- The Asia-Pacific region is expected to be the fastest-growing market, followed by the Middle East & Africa, due to increasing disease burden and improving healthcare infrastructure.

- Revenue growth will be volume-driven, with price erosion being a constant factor. Newer therapies for severe respiratory diseases represent a competitive threat, but IPRATROPIUM's cost-effectiveness secures its role in managing mild to moderate COPD.

Frequently Asked Questions

-

Are there any remaining patents that could impact the production of generic IPRATROPIUM? No, the core patents for IPRATROPIUM have long expired, allowing for widespread generic production. Any remaining patents are typically narrow, relating to specific manufacturing processes or novel delivery devices, and do not pose a significant barrier to entry for standard generic formulations.

-

What is the primary indication for IPRATROPIUM that drives its current market demand? The primary indication driving market demand for IPRATROPIUM is the management of chronic obstructive pulmonary disease (COPD). It is also used for asthma, though often as a rescue medication or in combination therapy.

-

Which geographical regions are projected to exhibit the highest growth rates for IPRATROPIUM sales? The Asia-Pacific region is projected to exhibit the highest growth rate, followed by the Middle East & Africa. These regions are experiencing a rapid increase in respiratory disease prevalence and are expanding their healthcare infrastructure, alongside a strong demand for affordable generic medications.

-

How does the emergence of newer respiratory therapies, such as LAMA/LABA combinations, affect the market for IPRATROPIUM? Newer therapies like long-acting muscarinic antagonist (LAMA) and long-acting beta-agonist (LABA) combinations are increasingly used for more severe COPD and asthma. While these can displace IPRATROPIUM in some patient segments, its cost-effectiveness ensures its continued use for mild to moderate COPD and in resource-limited settings.

-

What are the main factors contributing to the price sensitivity of the IPRATROPIUM market? The price sensitivity of the IPRATROPIUM market is primarily due to the expiration of its foundational patents, which has led to a large number of generic manufacturers competing. This saturation creates a highly competitive environment where price is a key differentiator for market access and prescription by healthcare providers.

Citations

[1] World Health Organization. (2022). Chronic obstructive pulmonary disease (COPD). Retrieved from https://www.who.int/news-room/fact-sheets/detail/chronic-obstructive-pulmonary-disease-(copd)

More… ↓