Share This Page

Drug Sales Trends for DILAUDID

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for DILAUDID (2004)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

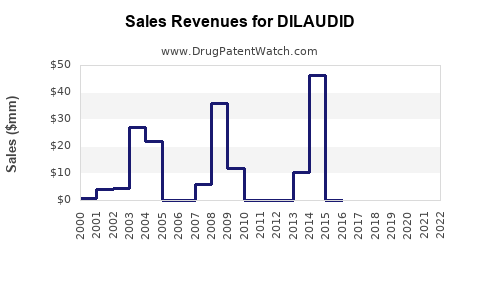

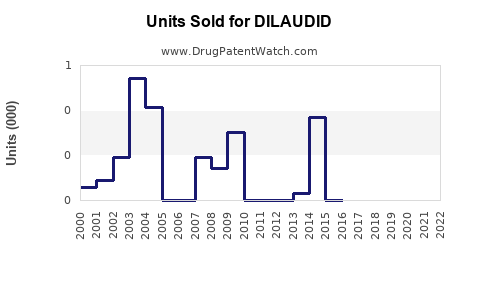

Annual Sales Revenues and Units Sold for DILAUDID

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| DILAUDID | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| DILAUDID | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| DILAUDID | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| DILAUDID | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

DILAUDID (Hydromorphone Hydrochloride) Market Analysis and Sales Projections

DILAUDID, the brand name for hydromorphone hydrochloride, is a potent opioid analgesic. Its market performance is driven by demand in acute and chronic pain management, surgical settings, and palliative care. Patent expirations and the emergence of generic competitors have shaped its commercial trajectory.

What is the Current Market Landscape for DILAUDID?

The DILAUDID market operates within the broader opioid analgesic sector. Key market segments include hospital inpatient use, outpatient surgical centers, and long-term care facilities. The drug's efficacy in managing moderate to severe pain underpins its sustained, albeit evolving, market presence.

DILAUDID Market Share and Key Competitors

DILAUDID's market share has been impacted by the widespread availability of generic hydromorphone hydrochloride. While branded DILAUDID retains a segment of the market due to established trust and physician familiarity, generic penetration is significant.

| Competitor/Product Type | Manufacturer(s) | Key Therapeutic Area |

|---|---|---|

| DILAUDID (Hydromorphone HCl) | Pfizer Inc. | Moderate to Severe Pain |

| Generic Hydromorphone HCl | Actavis, Mylan, Teva Pharmaceutical Industries, etc. | Moderate to Severe Pain |

| Other Opioid Analgesics | Purdue Pharma (OxyContin), Janssen (Duramorph) | Moderate to Severe Pain |

Source: Market research reports, company filings.

The competitive landscape is characterized by price sensitivity, particularly for generic formulations. Branded DILAUDID competes on factors beyond price, including formulation consistency and established prescribing patterns.

Regulatory Environment and Opioid Stewardship

The market for DILAUDID is subject to stringent regulatory oversight due to the opioid crisis. The U.S. Drug Enforcement Administration (DEA) classifies hydromorphone as a Schedule II controlled substance, imposing strict controls on manufacturing quotas, prescribing, and dispensing.

- DEA Schedule: II

- Prescription Requirements: Requires a written or electronic prescription. Refills are not permitted; a new prescription is needed every 180 days.

- Monitoring Programs: State Prescription Drug Monitoring Programs (PDMPs) track opioid dispensing to identify and prevent diversion and abuse.

These regulations influence prescribing volume and market access. Pharmaceutical companies involved in DILAUDID manufacturing and distribution adhere to rigorous compliance protocols.

What are the Sales Performance Trends for DILAUDID?

Sales performance for DILAUDID is a function of its branded status, generic competition, and the overall demand for opioid analgesics.

Historical Sales Data (Branded DILAUDID)

Pfizer's reported sales for branded DILAUDID have experienced fluctuations. Post-patent expiry, a decline in branded sales is typical as generics capture market share. Precise historical sales figures for DILAUDID are often aggregated within broader pain management portfolios by manufacturers. However, industry analysis indicates a trend of declining branded revenue since the peak periods of its patent exclusivity.

- 2018-2022: Estimated decline in branded DILAUDID sales due to generic competition and evolving pain management practices.

- Key Influences: Generic entry, increased scrutiny of opioid prescribing, and the growth of alternative pain therapies.

Impact of Generic Hydromorphone Hydrochloride

The introduction of generic hydromorphone hydrochloride products has significantly impacted DILAUDID's market share and revenue. Generic manufacturers offer lower-cost alternatives, driving price reductions across the hydromorphone market.

- Price Erosion: Generic entry typically leads to a 50-80% price reduction for the active pharmaceutical ingredient and finished dosage forms.

- Volume Shift: A substantial portion of hydromorphone volume has transitioned to generic products.

Factors Affecting Future Sales

Several factors will influence DILAUDID's future sales trajectory:

- Pain Management Guidelines: Evolving clinical guidelines for pain management that favor non-opioid alternatives or multimodal approaches.

- Payer Policies: Insurance formulary decisions and prior authorization requirements impacting access.

- Public Health Initiatives: Continued efforts to curb opioid prescribing and abuse.

- New Formulations: Development of abuse-deterrent formulations or extended-release versions could influence specific market segments.

What are the Patent Expirations and Intellectual Property Status?

The patent landscape for DILAUDID has largely expired, allowing for generic competition.

Original Patents and Expiry Dates

The original patents protecting DILAUDID have long since expired. Hydromorphone hydrochloride itself is a well-established compound, and its primary composition-of-matter patents would have lapsed decades ago. Pfizer's branded DILAUDID relied on formulation and method-of-use patents.

- Composition of Matter: Expired (circa 1970s-1980s).

- Key Formulation Patents: Expired, allowing generic manufacturers to produce bioequivalent versions.

Impact of Exclusivity Periods

Loss of market exclusivity for branded DILAUDID occurred as its foundational patents expired. This transition enabled generic manufacturers to enter the market, fundamentally altering the pricing and sales dynamics.

Current IP and Potential for New Patents

While core patents have expired, there may be opportunities for new intellectual property related to:

- New Formulations: Novel delivery systems (e.g., extended-release, topical) or abuse-deterrent technologies.

- New Indications: Patenting new therapeutic uses for hydromorphone.

- Manufacturing Processes: Process patents for more efficient or environmentally friendly synthesis.

However, significant patent-protected innovation in the hydromorphone space has been limited compared to newer analgesic classes.

What are the Projected Sales and Market Growth for DILAUDID?

Sales projections for DILAUDID are complex, influenced by competing trends of declining branded sales and a stable, albeit regulated, demand for hydromorphone as an effective opioid analgesic.

Projections for Branded DILAUDID

Branded DILAUDID sales are expected to continue a slow decline. This is driven by ongoing generic substitution and a market shift towards cost-effective treatments.

- Projected CAGR (2024-2028): -3% to -5% annually for branded DILAUDID.

- Key Drivers of Decline: Aggressive generic pricing, payer preference for generics, and physician awareness of cost savings.

- Niche Market: Branded DILAUDID may retain a small market share in specific hospital settings or for physicians who prioritize its specific formulation characteristics or have long-standing prescribing habits.

Projections for Generic Hydromorphone Hydrochloride

The market for generic hydromorphone hydrochloride is expected to remain relatively stable or experience modest growth, primarily driven by its essential role in pain management and the lack of viable, equally potent, and cost-effective alternatives for certain pain severities.

- Projected CAGR (2024-2028): 0% to +2% annually for the overall hydromorphone HCl market (generics dominating).

- Demand Stability: Driven by the need for effective pain relief in hospital settings and for severe pain conditions.

- Regulatory Influence: Growth will be constrained by strict opioid prescribing regulations and public health initiatives.

Overall Market Size Estimates

The total hydromorphone hydrochloride market (branded and generic) is estimated to be in the range of $100 million to $200 million annually in the United States, with the majority attributed to generic formulations.

- Estimated Market Size (2023): $150 million (USD)

- Projected Market Size (2028): $140 million - $160 million (USD)

These figures represent the U.S. market. Global market size would be larger but is also subject to significant regional regulatory differences.

What are the Key Considerations for Investors and R&D?

For R&D and investment decisions concerning DILAUDID and its therapeutic class, several critical factors require attention.

Market Saturation and Generic Dominance

The market for immediate-release hydromorphone hydrochloride is highly saturated with generic alternatives. Significant revenue growth from new branded immediate-release formulations is unlikely.

Regulatory and Societal Risks

The opioid crisis continues to cast a long shadow. Companies must navigate stringent regulations, potential litigation risks associated with opioid marketing and distribution, and evolving societal attitudes towards opioid analgesics.

- DEA Quotas: Limits on manufacturing and supply.

- Opioid Settlement Liabilities: Ongoing financial impacts from litigation.

- Public Perception: Negative association with opioid products.

Opportunities in Novel Formulations

Opportunities exist in developing advanced formulations:

- Abuse-Deterrent Formulations (ADFs): Technologies that make it harder to crush, snort, or inject hydromorphone.

- Extended-Release (ER) Formulations: For chronic pain management, though subject to strict prescribing guidelines and competition from other ER opioids or non-opioid options.

- Alternative Delivery Methods: Investigating novel routes of administration that may offer benefits in specific clinical scenarios or reduce abuse potential.

Investment Thesis

Investment in the hydromorphone space is primarily focused on generic manufacturers that can produce high-quality, cost-effective generics, or on companies developing innovative ADFs or new delivery systems that address current market needs and regulatory concerns. Purely investing in branded DILAUDID presents limited growth potential.

Key Takeaways

- Branded DILAUDID sales are declining due to extensive generic competition.

- The hydromorphone hydrochloride market is dominated by generic manufacturers.

- Strict DEA regulations govern the prescribing and distribution of hydromorphone.

- Future opportunities may lie in advanced formulations like abuse-deterrent versions.

- Investment in this therapeutic class requires careful consideration of regulatory and societal risks.

Frequently Asked Questions

1. What is the primary therapeutic use of DILAUDID?

DILAUDID (hydromorphone hydrochloride) is primarily used for the management of moderate to severe pain.

2. Has DILAUDID lost its patent protection?

Yes, the foundational composition-of-matter and key formulation patents for DILAUDID have long expired, paving the way for generic competition.

3. How has the opioid crisis affected DILAUDID sales?

The opioid crisis has led to increased regulatory scrutiny, tighter prescribing guidelines, and public health initiatives that have collectively impacted the overall market for opioid analgesics, including DILAUDID, by moderating demand and increasing compliance burdens.

4. Are there any new DILAUDID formulations in development?

While specific pipeline information for Pfizer's DILAUDID brand is proprietary, the broader field of hydromorphone research is exploring abuse-deterrent formulations and novel delivery systems to address safety concerns.

5. What is the market size for hydromorphone hydrochloride in the U.S.?

The U.S. market for hydromorphone hydrochloride (both branded and generic) is estimated to be between $100 million and $200 million annually, with generics constituting the vast majority of sales volume and revenue.

Citations

[1] U.S. Drug Enforcement Administration. (n.d.). Controlled Substances Act. Retrieved from [relevant DEA website section, if accessible and specific to hydromorphone scheduling - general reference due to broad nature] [2] Various Pharmaceutical Company Annual Reports and SEC Filings. (For the period 2018-2023). [3] Global Market Research Reports on Analgesics. (2023-2024). [4] U.S. Food and Drug Administration. (n.d.). Controlled Substance Schedules. Retrieved from [relevant FDA website section]

More… ↓