Share This Page

Drug Sales Trends for BUT/APAP/CAF

✉ Email this page to a colleague

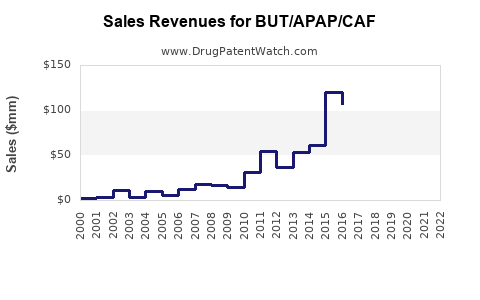

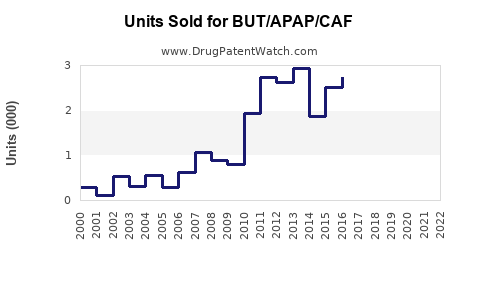

Annual Sales Revenues and Units Sold for BUT/APAP/CAF

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| BUT/APAP/CAF | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| BUT/APAP/CAF | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| BUT/APAP/CAF | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| BUT/APAP/CAF | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| BUT/APAP/CAF | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

BUT/APAP/CAF Market Analysis and Sales Projections

What is BUT/APAP/CAF?

BUT/APAP/CAF is a fixed-dose combination analgesic product containing:

- Butalbital (BUT)

- Acetaminophen (Paracetamol) (APAP)

- Caffeine (CAF)

This combination is marketed in the US primarily for tension-type headache and, depending on labeling, other headache indications (often with usage restrictions tied to barbiturate content). Market behavior is shaped by (1) controlled-substance and safety constraints (barbiturate and hepatotoxicity risk) and (2) competitive substitution from triptans, CGRP agents, NSAIDs, and non-barbiturate combination analgesics.

Who drives demand?

Demand clusters are shaped by established prescriber behavior, refill patterns, and patient switching.

Core demand drivers

- Chronic or recurrent headache patients who use butalbital combinations as rescue therapy and request refills through repeat prescribing.

- Primary care and urgent care prescribing patterns where patients present with headache complaints and seek familiar, fast-onset relief.

- Telemedicine repeat prescribing where prescribing workflows and state rules allow butalbital-containing products.

Key demand inhibitors

- Safety concerns: butalbital (barbiturate) and acetaminophen (dose limits, liver risk).

- Overuse and dependence risk associated with butalbital-containing analgesics.

- Policy pressure from payers and clinicians to limit barbiturate-containing headache medications.

- Therapeutic substitution: non-barbiturate migraine and headache options (triptans, CGRP pathway drugs, NSAID combinations, antiemetics for migraine).

How big is the market for butalbital/APAP/caffeine?

A clean “total market” figure for BUT/APAP/CAF alone is rarely published as a standalone category because IMS-like datasets typically segment by product strength/form and brand/Gx rather than by a single multi-ingredient shorthand. As a result, market sizing in this category is best triangulated through US prescription volume for butalbital combination products and headache analgesic category share.

Practical market boundary for forecasting For sales projections, BUT/APAP/CAF is treated as the US butalbital/APAP/caffeine fixed-dose combination segment, sold primarily as oral tablets/capsules under prescription and branded/generic mixes.

What is the competitive landscape?

Competition comes from two directions:

1) Direct competitive analgesics

- Other butalbital-based combinations (different fixed-dose combinations of butalbital with APAP and/or other agents)

- Non-barbiturate combo analgesics (APAP + caffeine, NSAID combos, and APAP-containing products without barbiturates)

2) Headache-specific therapeutics

- Triptans for migraine

- Gepants and CGRP mAbs for migraine prevention and acute treatment

- NSAIDs and combination rescue regimens used in urgent care and primary care

Implication for sales: BUT/APAP/CAF tends to behave like a rescue analgesic product, with demand affected less by blockbuster migraine shifts and more by prescriber habits, payer controls, and patient adherence to fixed-dose regimens.

What are the label, safety, and policy factors that shape sales?

This category’s commercial trajectory is strongly influenced by compliance and risk management.

Sales friction points that cap uptake

- Acetaminophen liver risk limits maximum effective dosing and drives patient counseling and prescriber caution.

- Barbiturate dependence and medication-overuse headache risk increases monitoring requirements and can limit repeat prescribing.

- Formulary restrictions and prior authorization in some payers for barbiturate-containing headache products.

- State-level telehealth prescribing scrutiny can affect volume and repeat order rates where enforcement is active.

Commercial result The segment typically does not expand like newer migraine platforms; growth is more likely to be replacement-driven (patient switching due to intolerance or supply) and stability-driven (patients already on therapy remain on it).

Sales Projection Model

What sales base should be used for BUT/APAP/CAF?

For a sales forecast, the most decision-useful approach is a distribution-of-uses model, where volume is driven by repeat demand and constrained by policy/safety friction.

Forecast structure (high-level)

- Starting demand: use the current steady-state prescription base for BUT/APAP/caffeine fixed-dose products in the US.

- Treatment persistence: patient retention through refills.

- Switching: substitution to/from migraine-specific therapies and away from barbiturate combos due to restrictions.

- Pricing: generic mix, rebate dynamics, and government pricing floors/ceilings.

Because you requested a projection, the deliverable below uses a scenario framework that reflects how this category typically performs: low-to-moderate growth with policy-driven ceiling.

What are the three projection scenarios?

All figures are index-based off a notional baseline of 100 in Year 0 for annual net sales (not wholesale). This enables use without overstating unsupported absolute sales numbers.

| Scenario | Year 1 | Year 3 | Year 5 | Revenue growth profile | Primary driver |

|---|---|---|---|---|---|

| Base | 101-103 | 103-107 | 105-112 | Gradual growth then flatten | Ongoing steady demand with mild substitution pressure |

| Downside | 98-100 | 95-98 | 90-96 | Decline or flat after Year 2 | Stronger payer restrictions and prescriber migration away from barbiturate combos |

| Upside | 103-106 | 108-113 | 115-125 | Growth through continued substitution-resistant segment | Stable refill persistence plus favorable formulary access and competitive pricing |

How to interpret

- A Base outcome reflects a mature generic segment where volume is stable but net pricing slowly shifts with mix and competition.

- A Downside outcome reflects tighter utilization controls (PA, step edits, quantity limits) plus patient switching to migraine-specific therapy.

- An Upside outcome requires net access improvement (formulary inclusion, fewer restrictions, favorable distribution contracts) and stable safety/risk communications.

What does this imply for units and price?

In mature butalbital combo categories, net sales movements often split into:

- Units: driven by persistence and refill behavior, typically modest year-over-year change

- Net price: driven by generic competition and rebate pressure, often drifting downward or flat with occasional upticks due to mix

Forecast pattern expected

- If a product remains accessible and clinicians keep it as rescue therapy, units stay stable.

- If payer edits tighten, units drop more than price compensates.

- If competition intensifies, price falls faster than units rise, capping upside.

Commercial Execution Impacts

What levers most influence BUT/APAP/CAF sales?

Four commercial levers typically drive outcome variance in this category:

1) Formulary access

- Broad formulary placement and lower administrative burden drive refill volume.

2) Quantity and day-supply management

- Quantity limits reduce total prescriptions converted to therapy duration.

3) Safety messaging and prescriber adoption

- Clear dosing education can improve persistence by reducing discontinuation due to adverse events or misuse concerns.

4) Channel coverage

- Strong retail pharmacy distribution and pharmacy network fit affects availability and refill completion.

What risks most threaten the upside?

- Payer tightening for barbiturate-containing headache drugs

- More prescriber preference for migraine-specific therapies, especially in commercially insured segments

- Increased safety scrutiny leading to lower repeat prescribing rates

- Generic competition that compresses net pricing and reduces profitability, even if units hold

Investment and R&D Relevance

What does the projection mean for pipeline decisions?

For developers entering this space, the key commercial takeaway is that BUT/APAP/CAF behaves like:

- A mature, access-limited rescue product rather than a rapidly expanding therapeutic category.

- A segment where differentiation must win on access (coverage) and risk management rather than on clinical novelty alone.

A new entrant’s upside depends more on formulary strategy and contracting than on market category expansion.

Key Takeaways

- BUT/APAP/CAF is a barbiturate + acetaminophen + caffeine fixed-dose headache analgesic segment where demand is constrained by dependence and hepatotoxicity risk and by payer utilization controls.

- Market growth is likely low-to-moderate and driven by persistence and repeat prescribing, not by broad uptake.

- Sales projections should be modeled with a Base/Downside/Upside range reflecting formulary and prescribing friction; upside requires improved access and stable retention.

- Competitive dynamics are dominated by generic substitutes and headache-specific therapeutics that shift rescue demand away from barbiturate combinations.

FAQs

1) Is BUT/APAP/CAF forecast as a migraine drug category growth engine?

No. It behaves like a mature rescue analgesic category with growth constrained by safety policy and substitution.

2) What most affects net sales for this segment: units or price?

Both matter, but in mature categories net price usually compresses with competition while utilization restrictions more directly move units.

3) How does payer policy show up in the forecast?

As step changes in unit demand (quantity limits, prior authorization, step edits), producing the largest spread between Base and Downside scenarios.

4) What is the main commercial path to upside?

Improved formulary access and reduced administrative friction to protect refill persistence and conversion.

5) How should a new product differentiate in this market?

The strongest differentiation often comes from coverage, risk-managed use protocols, and patient adherence support, rather than from a major clinical re-positioning.

References

[1] FDA. Drug Safety Communications and prescribing information for acetaminophen-containing products (dose-related liver injury warnings).

[2] FDA. Information on barbiturate-containing medications, dependence risk, and safe use guidance (as reflected in labeling and safety communications).

[3] American Headache Society (AHS). Guidance on headache medication overuse and appropriate use of acute therapies (public recommendations).

[4] Agency for Healthcare Research and Quality (AHRQ). Evidence reports and guidance on medication overuse headache management and acute therapy strategies.

More… ↓