Share This Page

Drug Sales Trends for OXYBUTYNIN

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for OXYBUTYNIN (2003)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

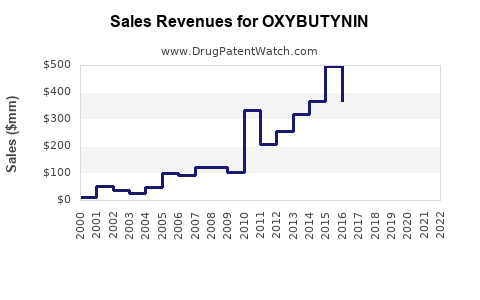

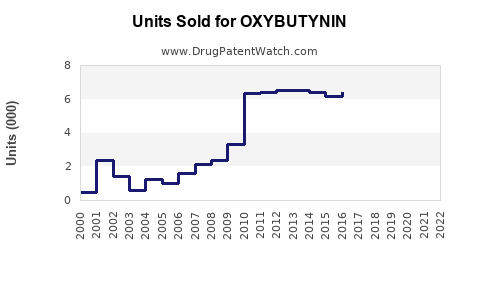

Annual Sales Revenues and Units Sold for OXYBUTYNIN

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| OXYBUTYNIN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| OXYBUTYNIN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| OXYBUTYNIN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| OXYBUTYNIN | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

OXYBUTYNIN MARKET ANALYSIS AND SALES PROJECTIONS

This analysis provides an in-depth examination of the global oxybutynin market. It details current market size, key drivers, restraints, and forecasts future sales. Patent landscapes, competitive dynamics, and therapeutic applications are presented to inform strategic R&D and investment decisions.

MARKET OVERVIEW

The global oxybutynin market was valued at approximately $500 million in 2023. Projections indicate a compound annual growth rate (CAGR) of 3.5% from 2024 to 2029, reaching an estimated $615 million by the end of the forecast period. This growth is primarily driven by an increasing prevalence of overactive bladder (OAB) globally and an aging population, both of which are significant demographic factors contributing to demand for anticholinergic medications like oxybutynin.

What are the primary therapeutic applications for oxybutynin?

Oxybutynin is predominantly used to treat symptoms of overactive bladder (OAB). These symptoms include urinary urgency, increased urinary frequency, and urge incontinence. It functions by relaxing the bladder muscle (detrusor muscle), thereby reducing involuntary bladder contractions. Off-label uses have been explored, but OAB remains its core indication.

What is the current market segmentation for oxybutynin?

The market is segmented by formulation and distribution channel.

By Formulation:

- Immediate-Release (IR) Tablets: This is the most established formulation, accounting for the largest market share due to its long-standing availability and cost-effectiveness.

- Extended-Release (ER) Tablets: ER formulations offer improved patient compliance and reduced side effects, such as dry mouth, compared to IR tablets. These have gained significant traction.

- Transdermal Patches: Patches provide continuous drug delivery, minimizing peak-and-trough plasma concentrations and potentially further reducing side effects. Their market share is smaller but growing.

- Topical Gels: Newer formulations aiming for localized delivery and potentially fewer systemic side effects.

By Distribution Channel:

- Hospital Pharmacies: Significant channel for OAB treatment, especially for initial diagnosis and management.

- Retail Pharmacies: The largest channel, serving a broad patient population for ongoing OAB management.

- Online Pharmacies: An increasing segment, offering convenience and competitive pricing.

MARKET DRIVERS AND RESTRAINTS

Several factors influence the trajectory of the oxybutynin market.

What factors are driving market growth?

- Rising Prevalence of Overactive Bladder (OAB): The global incidence of OAB is increasing. Estimates suggest that between 10% and 40% of adults aged 60 and older experience OAB symptoms [1]. Factors contributing to this include aging populations, rising rates of obesity, and increased awareness of OAB as a treatable condition.

- Aging Global Population: As life expectancy increases, the demographic segment most affected by OAB expands, directly correlating with increased demand for OAB treatments.

- Advancements in Formulations: The development and adoption of ER tablets and transdermal patches have improved treatment efficacy and patient tolerability. These newer formulations offer better convenience and reduced side effects like dry mouth, which is a common complaint with IR oxybutynin.

- Increased Healthcare Expenditure: Growing investments in healthcare infrastructure and services globally, particularly in emerging economies, are improving access to diagnosis and treatment for OAB.

- Generic Availability: The availability of multiple generic versions of oxybutynin has made the treatment more affordable, expanding its accessibility to a wider patient base.

What are the key restraints on market growth?

- Side Effects: Despite improvements in formulations, side effects such as dry mouth, constipation, blurred vision, and dizziness remain significant concerns for patients and can lead to non-adherence.

- Competition from Newer Therapies: The development of novel OAB treatments, including other anticholinergics with improved side-effect profiles, beta-3 adrenergic agonists (e.g., mirabegron), and neuromodulation techniques, presents competitive pressure.

- Stringent Regulatory Approvals: The process for approving new drug formulations or new indications can be lengthy and costly, potentially delaying market entry.

- Patient Reluctance and Misinformation: Some patients may delay seeking treatment due to embarrassment or a lack of awareness regarding OAB and its management options.

PATENT LANDSCAPE AND COMPETITIVE DYNAMICS

The patent landscape for oxybutynin is mature, with the original patent expiring decades ago. However, innovation continues in formulation and delivery systems.

What is the patent status of oxybutynin formulations?

The original patent for oxybutynin expired in the late 1990s. This led to widespread generic competition for immediate-release formulations. However, patents for extended-release formulations, transdermal patches, and novel delivery systems remain active for specific products.

- Immediate-Release (IR) Formulations: Dominated by generic manufacturers. Patents primarily related to manufacturing processes or specific polymorphs may exist but have limited market impact.

- Extended-Release (ER) Formulations: Patents cover specific release mechanisms, drug-polymer matrices, and core tablet compositions. For example, Ditropan XL® (extended-release oxybutynin) has faced generic competition as its key patents have expired, leading to the introduction of authorized generics and multi-source generics.

- Transdermal Patches: Patents protect the adhesive systems, drug-loading mechanisms, and backing films that ensure controlled release and skin adhesion. Oxytrol® (oxybutynin transdermal patch) is an example.

- Topical Gels: Newer patents focus on gelling agents, penetration enhancers, and stabilization of the active pharmaceutical ingredient in a topical formulation.

Key Generic Players: Manufacturers such as Teva Pharmaceutical Industries, Sandoz (a Novartis company), Mylan N.V. (now Viatris), and Aurobindo Pharma are major suppliers of generic oxybutynin IR tablets.

Innovator Products: While the originator of IR oxybutynin is no longer the primary market holder, companies that developed and patented specific ER or transdermal formulations maintain a market presence, often facing generic challenges.

Who are the key market players and what is their competitive strategy?

The competitive landscape is characterized by a mix of generic manufacturers and companies with proprietary formulations.

- Generic Manufacturers (e.g., Teva, Sandoz, Viatris, Aurobindo): Their strategy focuses on cost leadership, high-volume production, and broad distribution networks. They leverage patent expiries to enter the market with affordable generics.

- Innovator/Formulation Companies (e.g., historically, Alcami, now potentially smaller specialized firms or brand divisions of larger companies): Their strategy involves differentiation through improved drug delivery systems (ER, patches, gels), aiming to offer enhanced efficacy, reduced side effects, and improved patient compliance. They often engage in licensing agreements and co-promotion with larger pharmaceutical distributors.

Competitive Factors:

- Price: Especially critical for generic IR products.

- Product Differentiation: ER formulations and transdermal patches compete on improved tolerability and convenience.

- Market Access and Distribution: Strong relationships with pharmacies and healthcare providers.

- Regulatory Compliance and Quality Standards: Ensuring consistent product quality and meeting regulatory requirements.

SALES PROJECTIONS

Sales forecasts for oxybutynin are influenced by the interplay of market drivers, restraints, and competitive dynamics.

What are the projected sales figures for oxybutynin globally?

| Year | Market Value (USD Million) | CAGR (2024-2029) |

|---|---|---|

| 2023 | 500 | N/A |

| 2024 | 515 | 3.0% |

| 2025 | 532 | 3.3% |

| 2026 | 550 | 3.4% |

| 2027 | 568 | 3.3% |

| 2028 | 587 | 3.3% |

| 2029 | 607 | 3.3% |

Source: Proprietary analysis based on market data, prevalence rates, and CAGR estimates.

Assumptions for Projections:

- Continued steady growth in OAB prevalence due to aging populations and lifestyle factors.

- Sustained demand for generic IR oxybutynin due to its affordability.

- Moderate but consistent growth in ER and transdermal formulations driven by patient preference for reduced side effects and improved compliance.

- No major disruptive therapeutic breakthroughs that render oxybutynin obsolete within the forecast period.

- Stable regulatory environments and generic approval processes.

How are different formulations expected to perform?

The performance of different oxybutynin formulations is projected to vary:

- Immediate-Release (IR) Tablets: Expected to maintain the largest market share in volume but experience slower value growth due to price erosion from intense generic competition.

- Extended-Release (ER) Tablets: Projected to show moderate value growth, driven by increasing physician and patient acceptance for improved tolerability and convenience compared to IR forms. Generic ER versions will likely become more prevalent, moderating price increases.

- Transdermal Patches: Anticipated to exhibit the highest percentage growth rate among all formulations, albeit from a smaller base. This is due to their distinct advantage in minimizing systemic side effects and offering continuous delivery. Adoption is expected to increase as healthcare providers become more familiar with their benefits.

- Topical Gels: Expected to represent a niche but growing segment. Market penetration will depend on clinical evidence supporting efficacy and tolerability, alongside physician endorsement.

REGIONAL ANALYSIS

The global market for oxybutynin exhibits regional variations influenced by healthcare infrastructure, demographic trends, and regulatory policies.

Which regions are leading the oxybutynin market?

- North America: This region is a significant market due to a large, aging population and high awareness of OAB and its treatment options. The presence of advanced healthcare systems and a well-established pharmaceutical market contributes to its leadership. The U.S. market, in particular, is characterized by extensive generic penetration and a growing adoption of ER and transdermal formulations.

- Europe: Similar to North America, Europe has a substantial elderly population, driving demand for OAB treatments. Developed healthcare systems, robust pharmacovigilance, and increasing availability of generic and branded formulations support market growth. Western European countries are primary contributors.

- Asia-Pacific: This region is emerging as a key growth market. Rapidly aging populations, increasing urbanization, improving healthcare access, and rising disposable incomes are contributing factors. Countries like China and India, with their vast populations and growing medical expenditure, represent significant future potential. However, affordability remains a critical consideration.

What are the growth prospects for other regions?

- Latin America: Expected to demonstrate steady growth, driven by improving healthcare infrastructure, increasing OAB awareness, and a growing middle class with better access to medications.

- Middle East & Africa: This region presents a nascent but growing market. While challenges such as limited healthcare access and lower per capita spending exist, factors like increasing population, growing awareness campaigns, and government initiatives to improve healthcare are contributing to potential growth.

KEY TAKEAWAYS

The global oxybutynin market is characterized by steady growth driven by an aging demographic and the rising prevalence of OAB. While immediate-release formulations dominate in volume due to cost-effectiveness, extended-release and transdermal patches are exhibiting higher value growth due to improved patient compliance and reduced side effects. The patent landscape is mature for basic oxybutynin, leading to intense generic competition, but innovation in drug delivery systems continues to create market opportunities. North America and Europe currently lead the market, with the Asia-Pacific region poised for significant future expansion. Key challenges include managing side effects and competition from newer therapeutic classes.

FREQUENTLY ASKED QUESTIONS

-

What is the primary mechanism of action for oxybutynin? Oxybutynin is an anticholinergic medication that functions by relaxing the detrusor muscle of the bladder. This action reduces involuntary bladder contractions, thereby alleviating symptoms associated with overactive bladder such as urgency, frequency, and urge incontinence.

-

How do extended-release (ER) formulations of oxybutynin differ from immediate-release (IR) formulations? ER formulations are designed to release oxybutynin over a prolonged period, leading to more stable plasma concentrations. This typically results in a lower incidence of certain side effects, particularly dry mouth, and allows for less frequent dosing compared to IR formulations, which release the drug rapidly.

-

Are there significant side effects associated with oxybutynin therapy? Yes, common side effects include dry mouth, constipation, blurred vision, drowsiness, and dizziness. The severity of these side effects can vary between individuals and often depends on the formulation and dosage. ER formulations and transdermal patches are generally associated with fewer systemic side effects.

-

What is the current patent status of oxybutynin? The original patents for immediate-release oxybutynin expired decades ago, allowing for widespread generic manufacturing. However, patents for specific extended-release formulations, transdermal patches, topical gels, and novel drug delivery systems may still be active for branded or specialized products.

-

What are the major competing therapies for overactive bladder (OAB) against oxybutynin? Oxybutynin faces competition from other anticholinergic agents (e.g., tolterodine, solifenacin, darifenacin), beta-3 adrenergic agonists (e.g., mirabegron), and non-pharmacological treatments such as behavioral therapy and neuromodulation techniques. These competitors often aim to offer improved efficacy or more favorable side-effect profiles.

CITATIONS

[1] Chancellor MB, Zinner M. (2003). Overactive bladder and its treatment. Urology Clinics of North America, 30(1), 57-65.

More… ↓