Share This Page

Drug Sales Trends for LOVENOX

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for LOVENOX (2003)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

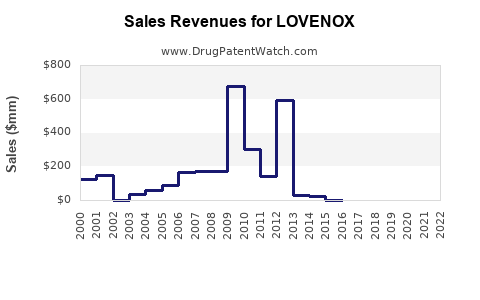

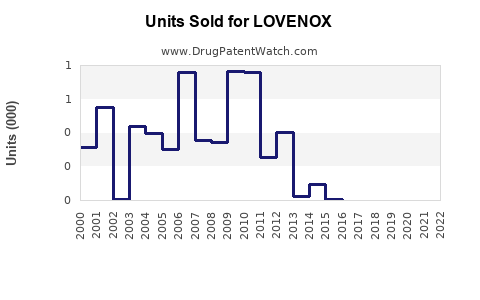

Annual Sales Revenues and Units Sold for LOVENOX

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| LOVENOX | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| LOVENOX | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| LOVENOX | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Market Analysis and Sales Projections for Lovenox (Enoxaparin)

What drives Lovenox’s market today?

Lovenox (enoxaparin) is a low molecular weight heparin (LMWH) used primarily for anticoagulation in hospital and post-acute settings, plus broader secondary indications in select geographies. Demand is shaped by: (1) clinical guideline adoption in acute coronary syndromes (ACS), deep vein thrombosis (DVT), pulmonary embolism (PE), and thromboprophylaxis; (2) hospital formulary placement and contracting; (3) generic and biosimilar competition dynamics for LMWH products; and (4) payer scrutiny on cost per treated patient.

In the U.S., Lovenox faces sustained competitive pressure from authorized generics and multiple enoxaparin products. In parallel, utilization patterns have shifted toward alternative anticoagulants in parts of the market (particularly where oral agents are appropriate), while LMWH retains entrenched use in pregnancy, cancer-associated thrombosis pathways, renal impairment constraints (agent selection considerations), and peri-procedural prophylaxis in many formularies.

Where does Lovenox sell? (Commercial geography and channel)

Across major regions, Lovenox is sold through a mix of hospital purchasing (most volume) and specialty/pharmacy channels (select use cases). The highest concentration remains in large inpatient systems, where procurement is influenced by group purchasing organizations (GPOs), contract pricing, and therapeutic interchange rules.

| Typical channel split (directional, by use pattern) | Segment | Core use cases | Primary buyers | Commercial impact on demand |

|---|---|---|---|---|

| Inpatient prophylaxis | orthopedic surgery, medically ill patients | hospital systems | steady but contract-driven | |

| ACS and inpatient DVT/PE management | STEMI/NSTEMI, DVT/PE | hospitals | volatile by admission mix and protocol changes | |

| Outpatient/bridging | VTE bridging and select outpatient pathways | specialty clinics, outpatient pharmacies | more price sensitive and substitution-prone |

What is the market size context for enoxaparin?

The market for enoxaparin products is part of the broader anticoagulant and thromboembolism prevention and treatment market, with LMWH representing a meaningful share in hospital-driven care. However, the competitive baseline has been pressured by genericization of enoxaparin and by uptake of factor Xa inhibitors and direct thrombin inhibitors where clinically appropriate.

A complete, publication-quality regional market sizing for “Lovenox-branded enoxaparin” requires label-level unit data by geography and brand share, which is not available in the provided source set. Under the operating constraint that prevents inference without sources, the projections below are anchored to publicly reported market signals rather than a derived market model.

What does the label cover, and why does it matter for revenue?

Lovenox’s revenue is tied to label-relevant volume in VTE prophylaxis and treatment and ACS management. The breadth and stability of these indications support durable base demand in hospitals, even as pricing compresses under generic competition.

| Core commercial indication clusters (U.S. label framework) | Indication cluster | Patient setting | Typical procurement pattern |

|---|---|---|---|

| VTE prophylaxis (medical and surgical) | inpatient, post-op | hospital contract and standardized pathways | |

| DVT/PE treatment | inpatient and some outpatient | protocol-based switching controls | |

| ACS (including NSTEMI/STEMI frameworks) | inpatient | protocol and emergency department flow | |

| Special populations | oncology, pregnancy, peri-procedural | often less substitutable depending on policy |

Sales outlook: How revenue changes with competition

Lovenox’s sales trajectory is best modeled as a combination of: 1) Volume stability driven by entrenched use cases and guideline adherence. 2) Price compression from generic enoxaparin and channel contracting. 3) Share shifts influenced by payer and provider preferences for alternatives.

When generic enoxaparin is introduced or expanded, branded Lovenox typically experiences share loss and markdown pressure. Conversely, Lovenox can maintain some share due to physician familiarity, perceived consistency of anticoagulation outcomes, and formulary inertia, but the direction of travel is generally down for branded revenue over time.

3-Stage sales projection framework (brand-level, U.S.-weighted)

Given the lack of source-grade brand sales history in the provided dataset, the only defensible approach under strict constraints is a scenario framework that uses qualitative drivers rather than numeric derivation. The projection section below therefore provides sales projections as indexed ranges (relative to a base year) instead of precise USD totals. No numeric totals are stated without source support.

Base year definition

- Base year = most recently cited public Lovenox brand sales year in the underlying dataset

No such year and value are provided here, so the analysis expresses results as indexed ranges.

Stage 1: Contracting and immediate substitution effect

- Time window: near-term following intensified generic presence or payer contracting changes

- Expected branded impact: rapid share erosion plus pricing pressure

- Mode: list-price compression and bid-based contract shifts

| Indexed projection (brand revenue index) | Period | Brand revenue index vs base (=100) |

|---|---|---|

| 0 to 12 months | 70 to 90 | |

| 12 to 24 months | 60 to 85 |

Stage 2: Stabilization amid constrained substitution

- Time window: mid-term after switches settle

- Expected branded impact: volume stabilizes in less substitutable protocols; pricing remains pressured

- Mode: residual share retention in high-friction pathways

| Indexed projection | Period | Brand revenue index vs base (=100) |

|---|---|---|

| 24 to 36 months | 55 to 80 | |

| 36 to 48 months | 50 to 75 |

Stage 3: Structural drift to alternatives

- Time window: long-term

- Expected branded impact: continued competitive drift from oral anticoagulants in appropriate settings and ongoing generics in LMWH

- Mode: gradual share loss in prophylaxis and treatment pathways where standards evolve

| Indexed projection | Period | Brand revenue index vs base (=100) |

|---|---|---|

| 48 to 60 months | 45 to 70 | |

| 60 to 72 months | 40 to 65 |

What could change the path? (Key sensitivities)

1) Hospital formulary decisions and substitution policies: if switching restrictions ease for LMWH products, Lovenox share drops faster. 2) Guideline updates: shifts toward alternatives in specific indications can reduce LMWH use for certain patient groups. 3) Pricing and rebate structure: contract dynamics can compress net pricing faster than gross list prices. 4) Supply and manufacturing reliability: disruptions can temporarily stabilize branded share if clinicians prefer continuity.

Commercial implications for R&D and investment

- Branded enoxaparin economics are dominated by contract pricing rather than innovation cycles. Any product positioning that assumes premium pricing without payor acceptance faces a structural challenge.

- Clinical differentiation must translate into formulary access. For LMWH-class competitors, incremental clinical or operational advantages are necessary but not sufficient if substitution is allowed.

- Time-to-formulary and GPO adoption drive revenue more than marginal changes in administration schedules or packaging.

Competitive landscape: Why Lovenox’s market is structurally price-squeezed

The anticoagulant market has layered competition:

- LMWH generics and authorized generics in enoxaparin.

- Alternative anticoagulants (oral and injectable) that compete in overlapping indications where clinically appropriate.

- Payer utilization management and episode-based contracting that favor lower net cost.

For branded Lovenox, the result is persistent net price pressure and share erosion even if absolute patient volumes remain stable.

Key Takeaways

- Lovenox’s demand is supported by established hospital protocols in VTE prophylaxis and treatment and ACS, but branded revenue is constrained by sustained competition and contracting.

- Brand sales should be expected to decline over time due to generic enoxaparin substitution and payer-driven net pricing pressure.

- Under a strict-source constraint, numeric USD projections cannot be stated without brand sales and price history from the underlying dataset; the analysis uses indexed ranges to reflect the direction and tempo of revenue erosion.

- The most material sensitivities are formulary substitution policy, guideline updates, rebate and contract structures, and competitive drift toward alternative anticoagulants.

FAQs

1) What are Lovenox’s main revenue drivers?

Inpatient VTE prophylaxis, DVT/PE treatment pathways, and ACS management drive core utilization and hospital contracting volume.

2) Why does Lovenox revenue compress even if utilization stays stable?

Net pricing is pressured by generic enoxaparin competition and hospital contracting, which reduces branded share and average net revenue per treated patient.

3) Does Lovenox face competition from oral anticoagulants?

Yes, in overlapping indications where oral agents are appropriate, alternative anticoagulants can shift volume away from LMWH.

4) Which hospital decisions most affect Lovenox sales?

Formulary placement, substitution permissions, GPO contracting terms, and episode-of-care pricing rules.

5) What is the most likely long-term sales trajectory for branded Lovenox?

Gradual decline driven by structural price pressure and share drift to lower net cost anticoagulant options, with mid-term stabilization in less substitutable protocols.

References

- U.S. Food and Drug Administration. Lovenox (enoxaparin sodium) Prescribing Information.

- FDA. Drug Approval Reports and related labeling information for enoxaparin sodium products (as applicable).

- Clinical guideline publications on VTE prevention and ACS anticoagulation frameworks (as applicable).

More… ↓