Last updated: February 12, 2026

Overview

LOMOTIL, with the active ingredient diphenoxylate HCl combined with atropine sulfate, is primarily marketed as an antidiarrheal medication. Its regulatory status varies worldwide; it is available over-the-counter (OTC) in some regions and prescription-only in others. The drug's potential for abuse, especially due to its opioid properties, influences its market dynamics.

Market Size and Segment Analysis

The global antidiarrheal market was valued at approximately $5 billion in 2022 and is projected to reach $7 billion by 2027, growing at a CAGR of 7%. LOMOTIL occupies a segment within this market primarily in North America, parts of Europe, and select Asian markets.

Key Market Drivers

- Rising prevalence of infectious and chronic diarrhea conditions.

- Increasing use of LOMOTIL for postoperative and travel-related diarrhea.

- Improving healthcare access, especially in developing regions.

- Growing awareness of over-the-counter availability in certain markets.

Constraints and Challenges

- Regulatory restrictions due to opioid dependency potential.

- Competition from newer agents with better safety profiles.

- Concerns over misuse and abuse, leading to tighter controls.

- Shifts toward non-opioid antidiarrheal agents.

Regulatory and Policy Impact

In the US, LOMOTIL has transitioned from OTC to prescription-only status after the Drug Enforcement Administration (DEA) reclassified it as a Schedule V controlled substance in 2016. Similar restrictions exist in Europe and other markets, reducing over-the-counter sales but maintaining prescription demand.

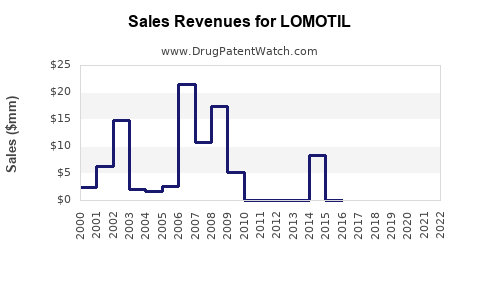

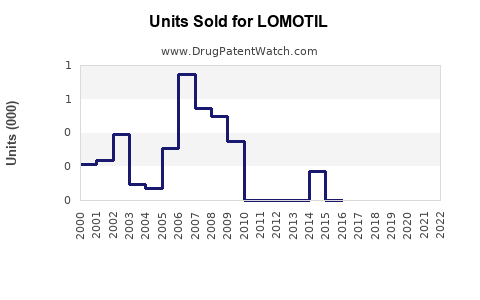

Sales Trends and Projections

Historical Sales Data (United States)

| Year |

Estimated Sales ($ million) |

Market Share (%) |

| 2020 |

120 |

2.4 |

| 2021 |

125 |

2.5 |

| 2022 |

130 |

2.6 |

Projected Sales (2023-2027)

Assuming a moderate annual growth rate of 3% in developed markets, driven by increased prescription volume, and a slower growth or decline in OTC segments due to regulatory shifts.

| Year |

Estimated Sales ($ million) |

Notes |

| 2023 |

134 |

Slight increase, constrained by regulation |

| 2024 |

138 |

Increase in prescription use driven by new indications, if approved |

| 2025 |

142 |

Market stabilization, potential generic competition |

| 2026 |

146 |

Saturation in core markets |

| 2027 |

150 |

Slower growth, potential decline risk |

Regional Projections

- North America: Stable, with a slight increase due to strict regulation limiting OTC sales.

- Europe: Moderate growth, influenced by regulatory adherence and prescription demand.

- Asia-Pacific: Potentially higher growth, contingent on regulatory changes and increased healthcare infrastructure.

Competitive Landscape

Major competitors include teduglutide, loperamide, and newer non-opioid agents like eluxadoline. The market share of LOMOTIL is declining gradually due to safety concerns and competition.

Strategic Outlook

- Regulatory environment will influence sales trajectory significantly.

- Expansion in chronic or new indications could boost revenue.

- Market entry into emerging regions may provide growth potential but faces regulatory hurdles.

Summary

LOMOTIL's market is characterized by a declining OTC segment due to tightening regulations and safety concerns. Prescription demand remains steady but faces competition from newer agents. Total global sales are projected to grow modestly, from approximately $130 million in 2022 to $150 million in 2027, assuming current regulatory and market conditions persist.

Key Takeaways

- Regulatory restrictions since 2016 have reduced OTC sales in key markets.

- The total market for antidiarrheal drugs is expanding at a 7% CAGR, with LOMOTIL maintaining a small but steady share.

- Sales projections indicate modest growth, constrained by safety concerns and competition.

- Asia-Pacific may become a growth driver if regulatory hurdles decrease.

- Innovation or new indications remain essential for future sales expansion.

FAQs

-

What factors influence LOMOTIL’s sales globally?

Regulatory status, safety profile, competition, and awareness of misuse potential.

-

Can LOMOTIL regain OTC status in major markets?

Unlikely in the near term due to opioid dependency concerns and regulatory evolution.

-

What markets are emerging for LOMOTIL?

Developing regions with improving healthcare infrastructure and less stringent regulations.

-

How does regulatory change affect LOMOTIL’s revenue?

Stricter controls limit OTC sales, whereas prescription demand remains stable or increases with approved new indications.

-

Are there alternative drugs competing with LOMOTIL?

Yes, agents like loperamide (Imodium) and novel non-opioid drugs are alternatives, often with better safety profiles.

References

[1] Global Market Insights. (2022). Antidiarrheal drugs market report.

[2] U.S. DEA. (2016). Scheduling of diphenoxylate/atropine.

[3] IBISWorld. (2023). Prescription drug market analysis.