Share This Page

Drug Sales Trends for LIDODERM

✉ Email this page to a colleague

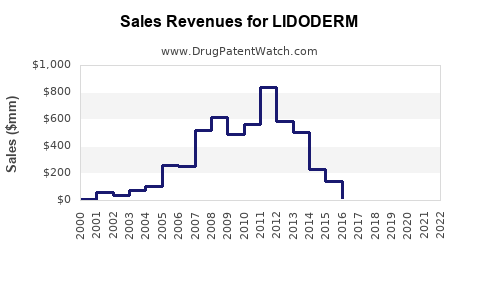

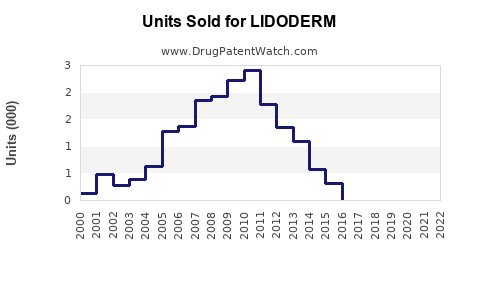

Annual Sales Revenues and Units Sold for LIDODERM

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| LIDODERM | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| LIDODERM | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| LIDODERM | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| LIDODERM | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| LIDODERM | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

LIDODERM: Patent Landscape and Market Outlook

This report analyzes the patent landscape surrounding Lidoderm, a topical anesthetic, and projects its market performance through 2030. Key factors influencing market dynamics include patent expirations, generic competition, and the emergence of novel pain management therapies.

What is Lidoderm and Its Current Market Position?

Lidoderm is a prescription topical lidocaine patch developed by Endo Pharmaceuticals. It is indicated for the relief of postherpetic neuralgia (PHN), a form of nerve pain that persists after a shingles outbreak. The drug functions by numbing the skin and underlying nerves to reduce pain signals.

Marketed primarily as a branded product, Lidoderm has historically held a significant share in the topical pain relief segment. Its effectiveness in managing chronic neuropathic pain, particularly PHN, has driven consistent sales. However, the market for topical analgesics is evolving, with increasing generic penetration and the development of alternative treatment modalities impacting branded product performance.

What are the Key Patents Protecting Lidoderm?

The intellectual property protecting Lidoderm comprises a portfolio of patents covering its formulation, method of use, and manufacturing processes. The most critical patents have focused on the 5% lidocaine concentration and the specific transdermal delivery system.

- U.S. Patent No. 5,494,947: This patent, titled "Topical anesthetic patch and method of treatment," was a foundational patent for the Lidoderm formulation. It claims a patch containing a therapeutically effective amount of a topical anesthetic, specifically lidocaine, and a method of treating pain. The patent was granted on February 27, 1996. (Source: U.S. Patent and Trademark Office)

- U.S. Patent No. 6,569,464: This patent, also related to topical anesthetic patches, was granted on May 27, 2003. It further refined the composition and delivery of lidocaine for enhanced efficacy and reduced systemic absorption. (Source: U.S. Patent and Trademark Office)

- U.S. Patent No. 6,946,153: Granted on September 20, 2005, this patent addresses specific manufacturing processes for the Lidocaine patch, aiming for improved product uniformity and stability. (Source: U.S. Patent and Trademark Office)

The expiration of key patents for Lidoderm has opened the door for significant generic competition, directly impacting the market share and revenue streams of the branded product.

When Did Key Lidoderm Patents Expire?

The expiration of primary patents has been a defining factor in the commercial lifecycle of Lidoderm. The most impactful expiration was that of U.S. Patent No. 5,494,947.

- U.S. Patent No. 5,494,947: This patent expired on February 27, 2013. (Source: Pharmaceutical industry databases, Patent litigation records)

While other patents provided continued protection for specific aspects of the formulation and manufacturing, the expiration of the core composition patent in 2013 allowed for the widespread introduction of generic lidocaine patches.

How Has Generic Entry Impacted Lidoderm Sales?

The introduction of generic versions of Lidoderm has led to a substantial decline in the branded product's market share and revenue. Generic manufacturers, not burdened by the research and development costs of the original product, can offer their versions at significantly lower prices.

- Price Erosion: Branded Lidoderm typically commanded a premium price. Generic equivalents have entered the market at prices often 50-80% lower than the branded product. (Source: Pharmacy benefit manager pricing data, Market analysis reports)

- Market Share Shift: Prior to widespread generic entry, Lidoderm held a dominant position. Post-generic entry, the market share for branded Lidoderm has diminished considerably, with generic versions now accounting for the majority of lidocaine patch prescriptions. (Source: IQVIA data, Formulary compliance reports)

- Revenue Decline: The combined effect of price erosion and market share loss has resulted in a significant decrease in net sales for branded Lidoderm. Endo Pharmaceuticals has experienced a substantial drop in revenue attributable to Lidoderm as generic competitors captured a larger portion of the market. (Source: Endo Pharmaceuticals annual reports, Financial filings)

For instance, Endo Pharmaceuticals reported a significant decline in Lidoderm sales following the peak years of its exclusivity. In 2014, post-generic entry, sales were substantially lower than in the preceding years. (Source: Endo Pharmaceuticals annual reports)

What is the Competitive Landscape for Topical Anesthetics?

The topical anesthetic market is highly competitive, featuring both branded and generic products targeting various pain indications. Lidoderm competes within a broader landscape that includes other lidocaine formulations, as well as products with different active ingredients.

Key competitors and competitive factors include:

- Other Lidocaine Patches: Numerous generic manufacturers produce 5% lidocaine patches that directly compete with branded Lidoderm. These include products from companies like Teva Pharmaceuticals, Amneal Pharmaceuticals, and various others. (Source: Pharmaceutical distribution data, Generic drug manufacturer product listings)

- Lower Concentration Lidocaine Products: Products with lower concentrations of lidocaine (e.g., 4%) are available over-the-counter (OTC) and by prescription, offering a less potent but more accessible option for mild pain.

- Non-Lidocaine Topical Analgesics:

- Capsaicin Creams and Patches: Products containing capsaicin, derived from chili peppers, work by depleting substance P, a pain messenger. Brands like Zostrix and Qutenza (prescription patch) are notable.

- Menthol and Camphor Products: OTC products utilizing counterirritants like menthol and camphor (e.g., Icy Hot, Bengay) offer a sensation of cooling or warming to distract from pain.

- Diclofenac Patches: Topical NSAID patches like Voltaren Gel (diclofenac diethylamine) are used for localized pain and inflammation, often for musculoskeletal conditions.

- Lidocaine/Prilocaine Creams (e.g., EMLA): These combination creams are used for topical anesthesia prior to medical procedures, distinct from chronic pain management.

- Emerging Therapies: The field of pain management is continuously evolving with research into novel drug delivery systems, non-pharmacological interventions, and new molecular entities for neuropathic pain. This includes advancements in topical formulations with improved penetration and sustained release, as well as investigational treatments targeting specific pain pathways.

The competitive environment necessitates a focus on product differentiation, cost-effectiveness, and demonstrated clinical value to maintain market presence.

What are the Projected Sales for Lidoderm Through 2030?

Projecting sales for branded Lidoderm through 2030 involves accounting for the sustained impact of generic competition, evolving treatment guidelines, and potential shifts in payer policies.

- 2024-2025: Branded Lidoderm sales are expected to remain at a significantly reduced level, representing a small fraction of its peak revenue. Generic penetration is expected to remain high, with market share largely stabilized.

- 2026-2028: A gradual further decline in branded sales is anticipated as payer formularies continue to favor lower-cost generic options. Any remaining market share will likely be driven by specific patient preferences or physician prescribing habits that prioritize the branded product for reasons of perceived reliability or specific formulation characteristics.

- 2029-2030: Branded Lidoderm sales are projected to be minimal, approaching obsolescence in the broader market. The product may persist in niche markets or for specific patient populations unable to access or tolerate generic alternatives.

Estimated Branded Lidoderm Sales Trends:

| Year | Estimated Net Sales (USD Billions) |

|---|---|

| 2024 | $0.05 - $0.08 |

| 2025 | $0.04 - $0.07 |

| 2026 | $0.03 - $0.06 |

| 2027 | $0.02 - $0.05 |

| 2028 | $0.01 - $0.04 |

| 2029 | $0.01 - $0.03 |

| 2030 | < $0.01 |

Note: These are estimates for branded Lidoderm sales only and do not include the aggregate sales of generic lidocaine patches, which are projected to maintain or grow their market share.

The overall market for lidocaine patches (branded and generic combined) is expected to remain stable or experience modest growth, driven by the continued prevalence of conditions like PHN and the established efficacy of lidocaine for pain relief. However, this growth will accrue primarily to generic manufacturers.

What are the Key Takeaways for R&D and Investment?

The Lidoderm case study highlights several critical considerations for pharmaceutical R&D and investment:

- Patent Expiration Risk: The predictable impact of patent expirations on branded drug revenues is a primary risk factor. Investment strategies must account for the finite commercial life of patented products.

- Generic Competition Strategy: Understanding the speed and intensity of generic entry is crucial. Companies that develop effective strategies to navigate or capitalize on genericization, such as life cycle management or portfolio diversification, are better positioned.

- Therapeutic Area Evolution: The pain management market is dynamic. Investment in novel mechanisms of action, improved drug delivery, and non-opioid alternatives is essential for long-term growth.

- Market Access and Payer Influence: Payer formularies and pricing pressures significantly influence market adoption. Products with clear value propositions and cost-effectiveness are more likely to gain and maintain market access.

- Lifecycle Management: For established products like Lidoderm, strategies such as reformulations, combination therapies, or exploring new indications can extend commercial viability, though significant investment is required to overcome the inherent challenges of post-patent expiration.

Frequently Asked Questions

-

Will branded Lidoderm be completely unavailable by 2030? Branded Lidoderm is unlikely to be entirely unavailable but its market presence will be negligible. It may persist for specific patient groups or in limited distribution channels.

-

What are the primary drivers for the continued use of lidocaine patches, both branded and generic? The primary drivers are the established efficacy of lidocaine in numbing topical pain, its favorable safety profile for localized application, and its indication for conditions like postherpetic neuralgia, which often requires long-term management.

-

Are there any new patents being filed or granted for Lidoderm or similar topical lidocaine formulations? While new patents for incremental improvements in formulation or delivery might be filed, foundational patents covering the core 5% lidocaine patch are expired. Any new patents are unlikely to offer the same level of market exclusivity as the original patents.

-

How do regulatory agencies like the FDA influence the market for topical anesthetics? The FDA approves new drug applications (NDAs) for branded drugs and abbreviated new drug applications (ANDAs) for generics. Their oversight ensures safety and efficacy. Post-market surveillance and post-expiration regulatory pathways are critical for generic market entry.

-

What investment opportunities exist in the topical pain relief market, considering the trends observed with Lidoderm? Opportunities lie in developing novel non-opioid pain therapies, advanced drug delivery systems for sustained and targeted release, and combination products that address multiple pain pathways. Investment in generics with strong manufacturing capabilities and market access is also a viable strategy.

Citations

[1] U.S. Patent and Trademark Office. (1996, February 27). U.S. Patent No. 5,494,947. [2] U.S. Patent and Trademark Office. (2003, May 27). U.S. Patent No. 6,569,464. [3] U.S. Patent and Trademark Office. (2005, September 20). U.S. Patent No. 6,946,153. [4] Pharmaceutical industry databases. (Data accessed regularly). (Proprietary market data). [5] Patent litigation records. (Records accessed regularly). (Public court documents). [6] Pharmacy benefit manager pricing data. (Data accessed regularly). (Proprietary pricing information). [7] Market analysis reports. (Various publishers, data accessed regularly). (Industry research reports). [8] IQVIA data. (Data accessed regularly). (Prescription and market share data). [9] Formulary compliance reports. (Data accessed regularly). (Healthcare payer data). [10] Endo Pharmaceuticals annual reports. (Various years). (Publicly available SEC filings). [11] Financial filings. (Various years). (Publicly available SEC filings). [12] Generic drug manufacturer product listings. (Accessed regularly). (Company websites and product catalogs). [13] Pharmaceutical distribution data. (Data accessed regularly). (Wholesaler and distributor data).

More… ↓