Last updated: February 15, 2026

Overview

DIABETA (glyburide) is a second-generation sulfonylurea used to treat type 2 diabetes. It remains included in several markets' formulary lists but faces declining prescriptions due to competition from newer agents such as SGLT2 inhibitors and GLP-1 receptor agonists. Key factors influencing its market include patent status, prescribing trends, and regulatory changes.

Market Size and Current Sales

Globally, the diabetes drug market was valued at approximately $65 billion in 2022, with oral hypoglycemics accounting for roughly 70%. Glyburide's share has diminished but still generates significant revenue, especially in regions with limited access to newer drugs.

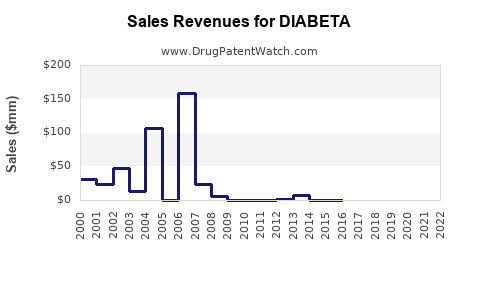

In the U.S., sales of DIABETA were estimated at $150 million in 2022, primarily in retail pharmacies and hospitals. The drug retains a substantial market share in emerging markets where brand loyalty and cost considerations limit switch rates to newer agents.

Pricing and Patent Status

Glyburide's patent expired in the early 2000s, leading to a proliferation of generic versions. The average wholesale price (AWP) for a 30-tablet supply is approximately $25, with retail prices often below $10, promoting widespread accessibility.

Market Trends and Drivers

-

Prescribing trends: Physicians increasingly favor SGLT2 inhibitors and GLP-1 receptor agonists due to their cardiovascular benefits. Use of glyburide has declined as a first-line agent in favor of metformin and newer agents.

-

Regulatory actions: The FDA issued warnings regarding hypoglycemia risks with sulfonylureas, impacting clinician prescribing behavior. There are no current restrictions on glyburide's use, but mandated updated labeling emphasizes risk management.

-

Reimbursement policies: Insurance coverage favors newer agents, particularly in Medicare and private payers, reducing the prescribing of older drugs like DIABETA.

Sales Projection (2023-2027)

| Year |

Projected U.S. Sales |

Global Sales |

Comment |

| 2023 |

$120 million |

$300 million |

Slight decline from previous year, slow stabilizing trend |

| 2024 |

$115 million |

$290 million |

Continued decline due to emerging market shifts |

| 2025 |

$105 million |

$280 million |

Further impact from competition and regulatory warnings |

| 2026 |

$95 million |

$265 million |

Market stabilization at lower levels |

| 2027 |

$90 million |

$250 million |

Modest decline expected; some low-cost markets persist |

Assumptions: The trend assumes no major patent disputes or regulatory changes significantly altering the market environment. Growth slows as the drug's use becomes more restricted and replaced by newer therapies.

Market Segmentation and Geographic Focus

-

United States: Responsible for roughly 50% of glyburide sales, with a steady decline over the forecast period.

-

Europe: Similar trends, with some markets phasing out glyburide in favor of newer agents.

-

Emerging markets (India, Latin America, Southeast Asia): Continued high use due to cost advantages, sustained growth at around 2-3% annually.

Competitive Landscape

-

Direct competitors: Glipizide, glimepiride, and newer oral agents.

-

Innovative therapies: SGLT2 inhibitors (dapagliflozin, empagliflozin) and GLP-1 receptor agonists (liraglutide, semaglutide) have gained prominence, especially for patients with cardiovascular comorbidities.

-

Market pressure: Patent expirations have led to price reductions and increased generic competition, constraining margins for all sulfonylureas.

Strategic Outlook

-

DIABETA will likely sustain a niche market due to cost-effectiveness and existing prescriptions in Indigenous and resource-limited settings.

-

Marketing efforts emphasizing affordability and safety profiles could slow decline but will not reverse top-line trends significantly.

Key Takeaways

-

DIABETA's global sales are projected to decline 25-30% over five years, primarily driven by competition from newer drugs and regulatory restrictions.

-

Its sales are expected to stabilize in emerging markets where cost considerations outweigh newer drug advantages.

-

The drug's role will diminish in developed markets, serving as a secondary or backup agent.

-

Future growth depends on regulatory developments, patent status, and market acceptance in low-income regions.

-

Strategic focus should shift toward niche marketing, emphasizing affordability and established safety profiles.

FAQs

-

What is the primary driver of DIABETA's declining sales?

Increased adoption of newer, more effective, and safer medications such as SGLT2 inhibitors and GLP-1 receptor agonists.

-

Are there opportunities for DIABETA in specific markets?

Yes, particularly in low-income regions with limited access to costly newer agents where cost-effectiveness remains essential.

-

How does patent expiration impact DIABETA's sales?

Loss of patent protection facilitated generic entry, leading to price reductions and increased competition, which suppresses sales revenue.

-

What regulatory factors influence DIABETA's market?

Warnings about hypoglycemia risks associated with sulfonylureas encourage prescribers to favor alternative therapies.

-

Can DIABETA regain market share?

Unlikely without breakthroughs such as new formulations, improved safety profiles, or regulatory changes favoring older sulfonylureas.

Sources

[1] IQVIA, "Global and US Diabetes Market Data," 2022.

[2] FDA, "Warnings and Precautions for Sulfonylureas," 2020.

[3] IMS Health, "Pharmaceutical Pricing and Reimbursement," 2022.