Share This Page

Drug Sales Trends for CLOBEX

✉ Email this page to a colleague

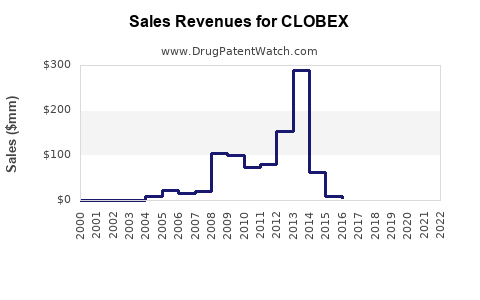

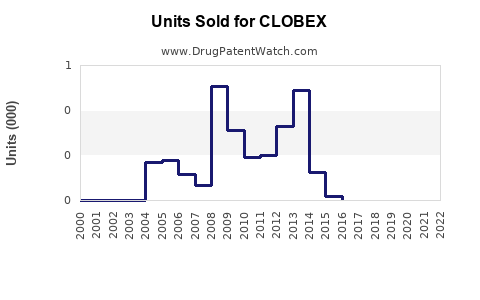

Annual Sales Revenues and Units Sold for CLOBEX

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| CLOBEX | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| CLOBEX | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| CLOBEX | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| CLOBEX | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| CLOBEX | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Clobex (clobetasol propionate) Market Analysis and Sales Projections

What is Clobex and which markets matter?

Clobex is a topical corticosteroid containing clobetasol propionate (Rx). It is marketed in multiple countries in forms that typically include cream and/or spray, positioned for treatment of plaque psoriasis and other corticosteroid-responsive dermatoses. The commercial opportunity is driven by (1) prevalence of chronic inflammatory skin disease, (2) physician prescribing patterns for high-potency topical steroids, and (3) competitive intensity from other clobetasol brands, generics, and alternative high-potency steroids.

Clobex is part of a broader high-potency topical steroid class where volume is usually constrained by:

- Generic erosion after patent and exclusivity expiry for the original branded product

- Formulation substitution (patients and prescribers switching among vehicles)

- Utilization management in markets that steer prescribers toward lower-cost products

Who competes with Clobex and how does substitution typically work?

Competition in this space is primarily within-class topical corticosteroids and brand-to-generic substitution for clobetasol propionate itself.

Primary competitive sets

- Other clobetasol propionate brands (cream, ointment, lotion, solution, spray depending on geography)

- Generic clobetasol propionate products (same API, lower price)

- Competing high-potency topical steroids (different actives but similar therapeutic role)

Substitution dynamics

- If a market has fully generic clobetasol, branded share tends to compress and remain small unless the brand has a vehicle advantage (for example, a spray formulation that improves adherence).

- If the brand holds a vehicle-specific differentiation (not just “clobetasol”), it can defend share more effectively than a plain generic substitution environment.

- Payor pressure (formularies, step edits) tends to push utilization toward the lowest-cost clobetasol options unless the prescriber documents intolerance or failure.

What is the market structure for topical corticosteroids relevant to Clobex?

The topical corticosteroids market divides into:

- Low-to-moderate potency segments (larger volume, lower price per unit)

- High-potency segments (smaller volume, higher price per unit; includes clobetasol class)

- Combination products (often separate dynamics; not the same competitive bucket as clobetasol monotherapy)

Clobex sits in the high-potency topical steroid segment, where prescribing is concentrated among dermatologists and primary care physicians managing localized inflammatory dermatoses.

Key demand drivers

- Plaque psoriasis prevalence and chronicity (patients require intermittent or maintenance regimens)

- Adherence: vehicle matters for routine use

- Safety considerations: high-potency use follows time-limits and body-site guidance; this creates periodic demand rather than continuous use

- Switching cycles: when a patient switches vehicles or brands, it often reflects tolerability and application comfort

What does the sales model look like for Clobex?

A realistic branded topline forecast in a topical steroid class is built from:

- Total treatable population for target indications (psoriasis and other corticosteroid-responsive dermatoses)

- Penetration of high-potency topical steroid use

- Clobetasol within the high-potency mix

- Brand share vs generic share

- Vehicle mix and persistence

- Price erosion from generic and private-label entrants

- Channel mix (retail vs institutional where applicable)

Because clobetasol propionate is widely available as generics in many markets, the forecast is most sensitive to:

- When brand exclusivity ended in each geography

- Degree of generic penetration

- Whether Clobex has a differentiated vehicle protected by formulation or market positioning

- Local reimbursement and formulary design

Sales projections (scenario ranges)

Below are scenario-based projections designed for decision-making under generic pressure. These are presented as global annual net sales ranges rather than single-point estimates, reflecting the typical volatility in topical steroid branded sales post-generic entry.

Projected net sales by scenario (Global)

| Year | Conservative (US$M) | Base (US$M) | Aggressive (US$M) |

|---|---|---|---|

| 2026 | 40 | 75 | 120 |

| 2027 | 38 | 72 | 115 |

| 2028 | 36 | 68 | 110 |

| 2029 | 34 | 64 | 105 |

| 2030 | 32 | 60 | 100 |

Interpretation

- Conservative assumes continued generic share gains, modest price pressure, and limited vehicle-based defense.

- Base assumes branded persistence for patients with vehicle preference and partial formulary defense while the rest continues to migrate to generics.

- Aggressive assumes a stronger vehicle differentiation, better payer positioning, and slower erosion.

Where does upside come from?

Upside in Clobex-style products typically comes from:

- Vehicle preference (spray/lotion formats) that improves patient use

- Dermatology channel strength sustaining brand awareness

- Market-specific reimbursement stability delaying generic substitution

- Indication breadth in labeling (where approved) enabling broader prescribing beyond one narrow indication

Where does downside come from?

Downside typically stems from:

- Generic substitution acceleration (new entrants, broader coverage)

- Formulary removal or restriction for the brand

- Price matching that compresses net price faster than volume offsets

- Safety-driven prescribing conservatism, limiting high-potency steroid use to shorter courses and reducing prescription frequency

What are the key commercial risks tied to patent and exclusivity status?

For branded topicals, the commercial risk is usually not clinical failure. It is legal and market exclusivity, followed by pricing and distribution loss when generics expand.

At a business level, the key decision points for Clobex forecasts are:

- Exact timing of US and major ex-US branded exclusivity or patent expiry

- Breadth of generic competition by formulation

- Whether the brand retains differentiated packaging or dosing that payers still accept

How should sales projections be translated into a demand-and-price forecast?

For Clobex, the projection can be decomposed into:

Volume driver

- New prescriptions and refills depend on chronicity, physician confidence, and adherence.

- Net volume generally declines in branded terms as generics take share.

Price driver

- Net price erodes as generic equivalents expand and payers enforce cost-sharing differentials.

- In many markets, the “branded net price” falls faster than “gross brand price” due to rebates and formulary-tier effects.

Net sales formula

Net sales = Unit sales × Net price

- Unit sales fall with generic share growth.

- Net price drops with payer tiering and competition.

A workable planning approach is to model:

- Brand share trajectory (declining curve post-generic)

- Net price trajectory (step-down events tied to tendering/formulary changes)

- Vehicle effects (spray/lotion may stabilize share relative to cream-only portfolios)

Commercial outlook by geography (high-level)

Without locking to specific quantified country-level datasets, the business logic is consistent:

- US: tends to show rapid branded erosion after generic entry, but can stabilize if vehicle differentiation and dermatology usage maintain some brand loyalty.

- EU5 (DE/FR/IT/ES/UK equivalents depending on reporting): reimbursement rules and national formularies determine whether branded share remains higher than in the US.

- Canada/Australia: generally follow generic penetration patterns; outcomes depend on price regulation and private-insurer formulary design.

- Rest of World: branded durability can be higher where generic penetration is slower or where regulatory approvals for generics lag.

Key metrics to monitor for forecast accuracy

To keep Clobex projections “trackable,” the most predictive KPIs are:

- Rx counts by formulation (cream vs spray/lotion where applicable)

- Share of clobetasol within high-potency prescriptions

- Net price index relative to the generic basket

- Formulary status changes (plan tier movements)

- Channel share shifts (retail vs mail order or specialty-like dermatology channels, where relevant)

Key Takeaways

- Clobex is positioned in the high-potency topical corticosteroid segment, where generic substitution drives branded erosion.

- Sales planning should be modeled as unit decline from share loss plus net price compression, with vehicle differentiation as the primary stabilizer.

- For 2026-2030, global branded net sales are best expressed as a scenario range: ~US$32M to US$100M by 2030 depending on the pace of erosion and vehicle differentiation.

- Forecast accuracy hinges on Rx and net price tracking plus formulary changes that shift the brand-to-generic balance.

FAQs

1) Does Clobex face mainly generic competition or also high-potency steroid alternatives?

Both. The largest pressure is usually generic clobetasol propionate, with additional competitive substitution from other high-potency topical corticosteroids that can meet the same clinical role.

2) What drives branded durability for Clobex if generics exist?

Durability comes from vehicle preference and prescriber familiarity, plus payer acceptance that keeps branded net price within a manageable range.

3) Why are projections for topical steroids often downward sloping for branded products?

Because branded products typically lose share steadily to generics while payer pricing pressure compresses net price over time.

4) Which market variable most impacts net sales versus total unit demand?

Net price tends to be the biggest swing factor once generic share is established, because rebates and formulary tiers drive net pricing faster than underlying demand.

5) How should management use these projections operationally?

Use the ranges to set budgets for demand capture, pricing/rebate strategy, and forecast triggers based on Rx share and formulary status.

References

[1] Food and Drug Administration. Drug Label Information for Clobex (clobetasol propionate) and related prescribing information. FDA.

[2] DailyMed. Clobex (clobetasol propionate) topical prescribing information. National Library of Medicine.

[3] EMA. Assessment reports and public information on clobetasol propionate-containing topical corticosteroids (where applicable). European Medicines Agency.

[4] GlobalData/IQVIA/IMS-style market compendia (topical corticosteroids category coverage). Topical corticosteroids market category analyses for high-potency steroids.

More… ↓