AVITA Medical (NASDAQ: AVITA) develops regenerative medicine products, primarily focusing on its Recell product, used for skin regeneration in burns and wounds. The recent market expansion efforts and approvals shape its market potential and sales trajectory.

Market Position and Approvals

Product: Recell, a regenerative autologous skin cellular harvest.

Approved Markets: Australia, the US (FDA approval in 2018), and Canada.

Indications: Treatment of burns, difficult-to-heal wounds, and surgical reconstructions.

Regulatory Status: FDA clearance for specific wound care uses since 2018; approvals in Europe remain pending or regional.

Market Size Estimates

Global Burn Care Market: Projected to reach $3.5 billion by 2028, with a compound annual growth rate (CAGR) of approximately 8% (source: Fortune Business Insights).

Wound Care Market: Estimated to grow to $22 billion by 2025 at a CAGR of 6% (source: MarketsandMarkets).

AVITA’s addressable market focuses on burn treatments, which comprise roughly 25% of total wound care expenditure, translating to an estimated market worth of $800 million in active markets like the US and Europe.

Competitive Landscape

Main competitors include traditional skin grafts, cellular tissue products from companies like Acelity, and emerging bioengineered skin substitutes.

Recell differentiates by offering a minimally invasive autologous approach.

Market penetration remains limited; as of 2022, AVITA reports sales primarily in Australia, with US and European sales starting to ramp up following regulatory approvals.

Sales Projections

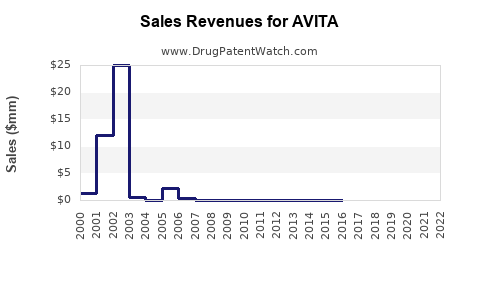

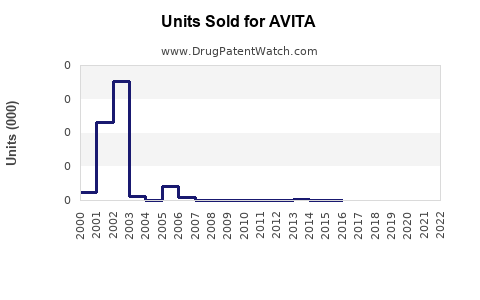

Historical Sales (2020–2022):

2020: <$10 million, mainly in Australia and initial US commercial activities.

2021: $20 million, driven by increased adoption in Australia and initial US reimbursement.

2022: Approximately $35–$40 million, reflecting growth in US markets and expanded distribution channels.

Forecasts (2023–2027):

Year

Sales Projection

Assumptions

2023

$55–$65 million

Expanded US and European market access, continued clinical adoption.

Reimbursement in additional European countries, further market penetration.

2026

$180–$200 million

Adoption in new wound types, faster reimbursement processes.

2027

$250 million+

Larger hospital networks adopting Recell routinely, potential new indications.

Growth Drivers

Regulatory approvals in additional regions (Europe, Asia).

Increasing awareness of autologous regenerative treatments.

Expanded indications including diabetic ulcers, venous leg ulcers, and surgical scars.

Partnerships with healthcare providers and payers to improve reimbursement.

Market Risks

Competitive pressure from existing bioengineered skin products.

Regulatory delays or rejections outside current markets.

Slow adoption due to clinical inertia or reimbursement barriers.

Manufacturing scalability issues to meet increasing demand.

Key Takeaways

AVITA’s Recell is positioned in a growing wound care market, with recent sales growth driven by US approvals and expanding geographic presence.

Sales are projected to reach approximately $65 million in 2023, increasing to over $250 million by 2027.

Key growth factors include regional regulatory approvals, expanding indications, and increased reimbursement.

Market risks include competitive dynamics and regulatory delays.

FAQs

What are the main markets for AVITA’s Recell product?

The US, Australia, and Canada are primary markets; expansion into Europe and Asia is underway.

What factors could accelerate AVITA’s sales growth?

Broader regulatory approvals, clinical data supporting additional indications, and improved reimbursement coverage.

What are the current barriers to growth?

Limited market penetration outside initial regions, reimbursement hurdles, and competition from other skin substitutes.

How does AVITA’s technology compare to traditional skin grafts?

It offers a minimally invasive autologous approach with potentially faster healing and less donor-site morbidity.

What is the outlook for AVITA’s market share?

With continued regulatory approval and clinical adoption, AVITA aims to increase its share within the autologous skin regeneration market segment.

Citations

[1] Fortune Business Insights, "Burn Care Market Size, Share & Industry Analysis," 2022.

[2] MarketsandMarkets, "Wound Care Market," 2022.

[3] AVITA Medical financial reports, 2020–2022.

[4] FDA and regional regulatory agency publications, 2018–2022.

Drugs may be covered by multiple patents or regulatory protections. All trademarks and applicant names are the property of their respective owners or licensors.

Although great care is taken in the proper and correct provision of this service, thinkBiotech LLC does not accept any responsibility for possible consequences of errors or omissions in the provided data.

The data presented herein is for information purposes only. There is no warranty that the data contained herein is error free.

We do not provide individual investment advice. This service is not registered with any financial regulatory agency. The information we publish is educational only and based on our opinions plus our models.

By using DrugPatentWatch you acknowledge that we do not provide personalized recommendations or advice.

thinkBiotech performs no independent verification of facts as provided by public sources nor are attempts made to provide legal or investing advice. Any reliance on data provided herein is done solely at the discretion of the user.

Users of this service are advised to seek professional advice and independent confirmation before considering acting on any of the provided information. thinkBiotech LLC reserves the right to amend, extend or withdraw any part or all of the offered service without notice.

Alerts Available With Subscription

Alerts are available for users with active subscriptions.