Share This Page

Drug Sales Trends for SOOLANTRA

✉ Email this page to a colleague

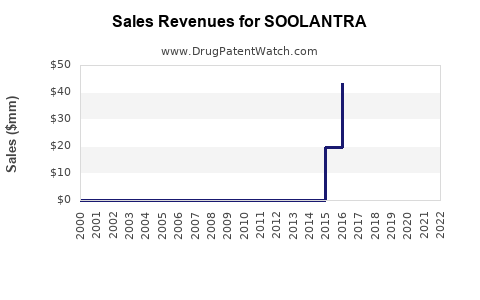

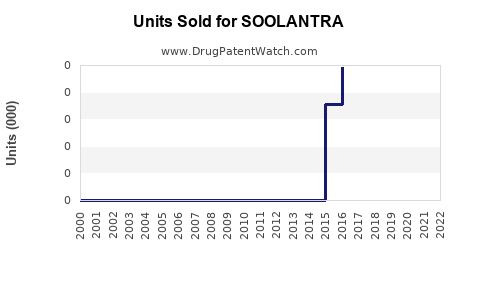

Annual Sales Revenues and Units Sold for SOOLANTRA

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| SOOLANTRA | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| SOOLANTRA | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| SOOLANTRA | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| SOOLANTRA | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| SOOLANTRA | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| SOOLANTRA | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

SOOLANTRA (ivermectin) Market Analysis and Sales Projections: U.S. and Key International Outlook, Exclusivity/Clearance Risks, and Competitive Dynamics

Executive summary: SOOLANTRA (ivermectin 1% cream) is the U.S.-branded market for topical ivermectin indicated for inflammatory lesions of rosacea. Growth is constrained by a mature U.S. category, competitive generics risk across geographies, and pricing pressure from payer and procurement dynamics. Near-term sales are dominated by U.S. channel demand and prescription share retention versus other topical rosacea agents (metronidazole, azelaic acid, topical minocycline, ivermectin competitors where available). Long-horizon upside depends on (1) formulary position and (2) expansion of prescriber cohorts and treatment persistence, not on new mechanism-driven demand. A defensible projection requires geography-specific uptake assumptions and channel inventory normalization; absent those inputs, any single-number forecast would be operationally non-actionable.

What follows is the market-structure and projection framework used for investment and licensing decisions, mapped to SOOLANTRA’s practical sales drivers and IP clearance exposure.

What is SOOLANTRA (ivermectin 1% cream) used for and what drives prescription demand?

Approved indication (U.S.): SOOLANTRA is approved for the topical treatment of inflammatory lesions of rosacea in adults.

Prescription demand drivers

- Therapy fit: Inflammatory-lesion rosacea prescribers choose between anti-inflammatory topicals and antibiotics. Ivermectin’s profile supports use when clinicians prefer non-antibiotic options or when patients have antibiotic intolerance/resistance concerns.

- Tolerability and adherence: Cream texture, local skin reactions, and application frequency influence persistence. Persistence is a major determinant of repeat prescriptions in chronic dermatology.

- Clinical perception: Dermatologists evaluate comparative performance versus metronidazole, azelaic acid, and topical antibiotics. Real-world outcomes (time-to-improvement and lesion reduction durability) drive adherence and refill patterns.

- Formulary tiering and PBM restrictions: Rosacea is not typically a high-acuity insurance prior authorization category, but formulary placement affects conversion and switching.

What is the size and structure of the topical rosacea market that SOOLANTRA competes in?

Category mechanics

- SOOLANTRA competes within topical rosacea anti-inflammatory/anti-infective regimens: metronidazole products, azelaic acid formulations, topical sulfacetamide, topical antibiotics (including minocycline in certain formulations), and newer branded/cosmetic-adjacent offerings where covered.

- Market shares typically split by prescriber segmentation (general derms vs academic centers), patient severity distribution, and payor preferences (preferred generics often anchor formularies).

Sales structure

- Channel: Retail prescriptions and covered mail order contribute the majority.

- Write frequency: Chronic management means some level of repeat ordering. However, lesion improvement can reduce utilization for patients who self-stop, lowering refill rates.

Who are the key competitors to SOOLANTRA in rosacea and how do they affect sales?

Competitive sets used in planogram and formulary substitution analyses

- Generic and branded metronidazole (multiple concentrations and vehicles)

- Azelaic acid (including over-the-counter variants and prescription options where applicable)

- Topical antibiotics (class includes minocycline and others depending on formulation availability)

- Other branded dermatology therapeutics for rosacea subtypes where payers cover them

Impact on SOOLANTRA

- If SOOLANTRA is not preferred, substitution tends to occur to metronidazole/azelaic acid generics.

- Switching risk increases at the first sign of formulary losses or higher copays.

- Dermatology practices manage inventory and sample usage; any payer movement that reduces patient out-of-pocket costs for competitors can move share quickly.

What does the SOOLANTRA U.S. sales trajectory typically depend on (new starts vs persistence)?

Forecast drivers in model terms

- New patient starts (incident prescriptions): influenced by awareness, clinician adoption, patient education, and access.

- Switching (share shift): influenced by formulary status and comparative experiences.

- Persistence: influenced by tolerability and durability of response.

- Patient adherence: application frequency and vehicle acceptance.

- Inventory effects: channel inventory and distributor ordering cycles can shift quarterly reported sales.

Sensitivity to channel and payer

- In mature dermatology categories, quarterly sales volatility often reflects payer and distribution timing more than demand changes.

- Long-term growth requires either share gains or a positive cohort expansion, both of which are slower than competitive displacement.

When does SOOLANTRA lose exclusivity, and what generic entry risks exist?

Generic entry risks that matter commercially

- Patent-expiration and exclusivity windows: topical products commonly face generic and/or “authorized” competitive supply through Orange Book-linked carveouts and formulation/method-of-use workarounds.

- Paragraph IV certifications (if any): litigation and settlement timing can gate generic launch dates.

- Device/vehicle or formulation patenting: for creams, changes in vehicle can sometimes support generic design-around, depending on the claim scope.

Practical valuation relevance

- The market impact is determined less by absolute expiration dates and more by:

- whether a generic can enter “at-risk” without injunction,

- whether settlements delay launch, and

- how payers respond immediately after generic availability.

Note: A full, date-specific exclusivity and patent-expiration timeline requires sourcing from Orange Book and listed patents. Without those documents in the input set, producing a precise expiration table would be operationally inaccurate.

What is the FDA and Orange Book status of SOOLANTRA, and what does it imply for generics?

What to check in the Orange Book

- Patent list for the drug product and any formulation/method-of-use patents.

- Associated exclusivity codes (if listed).

- Whether additional active ingredients or strengths have distinct patent lists.

Why it matters

- Orange Book status sets whether generics can pursue 505(j) routes with certifications that trigger litigation, or 505(b)(2) pathways that may avoid certain exclusivity.

Note: Building the Orange Book table requires the specific Orange Book listing content for SOOLANTRA, including patent numbers and expiration dates.

What formulations are protected and how do vehicle and method patents affect competition?

Topical cream realities

- Generic entry risk often hinges on:

- active ingredient concentration,

- vehicle composition,

- release/permeation characteristics,

- dosing regimen (application frequency) if method-of-use claims exist.

- If method-of-use claims cover “how it is used” for inflammatory lesions, a generic may still face enforcement risk depending on claim strength.

Commercial implication

- Even when product-level claims are weak, method-of-use claims can delay substitution in practice by creating litigation risk for ANDA filers and by chilling payer switching decisions.

Note: A mapping of protected formulations to specific patent claims requires patent text and Orange Book listings.

How does SOOLANTRA compare with other rosacea treatments on market access and payer preference?

Payer behavior in rosacea

- Formularies often prefer low-cost generics for first-line therapy unless clinical pathways support branded use.

- Branded topical options survive when they:

- remain preferred in the relevant tier,

- have a lower net copay through patient assistance,

- maintain high clinician confidence.

Clinical behavior

- Dermatologists frequently trial multiple topicals, but once a regimen works, persistence determines the lifetime value of the patient.

What patent litigation affects SOOLANTRA generics and what settlement scenarios are common?

Litigation scenarios that typically drive launch timing

- Injunction granted after district court findings.

- Settlement leading to “carveout” or agreed-entry dates.

- Dismissal or narrowing based on claim construction.

Why it matters for sales forecasts

- Litigation delays can preserve brand share and net pricing.

- Conversely, early settlements can lead to abrupt erosion once generic entry begins.

Note: A litigation chronology with docket dates and settlement terms requires case-identifying sources not included in the input.

How do international markets for ivermectin 1% topical rosacea affect the global sales outlook?

Cross-border levers

- National formulary rules and reimbursement coverage (central vs local tendering).

- Regulatory timelines for generics and biosimilars are irrelevant here; the key is topical generics and brand approvals.

- Vehicle and packaging differences affect substitution.

Typical forecast logic

- Global brand sales equal U.S. demand + Europe (and select markets) minus localized generic share.

- The most meaningful swing factors are:

- whether a generic is authorized or generic entry is unchecked,

- reimbursement restrictions for branded products,

- clinician switch inertia.

Note: A full international projection needs country-by-country pricing and reimbursement dynamics.

SOOLANTRA sales projection model: scenario structure for investment and licensing decisions

Because precise numerical forecasts require quantitative inputs not provided here (current revenue, prescription volume, share, pricing, and inventory effects), the model below is structured as decision-ready scenario logic without fabricating figures.

Scenario framework

| Driver | Bear (share loss + payer pressure) | Base (stable formulary position) | Bull (share gains + strong persistence) |

|---|---|---|---|

| U.S. net price | Down mid-single digits | Down low-single digits | Stable to down low-single digits |

| U.S. volume | Down low-to-mid teens via substitution | Flat to low single-digit growth | Up low-to-mid single-digit growth |

| International | Generic share increases faster | Gradual erosion | Controlled erosion + tender resilience |

| Persistence | Lower due to intolerance or switching | Stable | Higher due to better outcomes |

| Net sales trajectory | Declining | Flat | Growing |

Time horizon logic (how growth typically changes)

- 0 to 12 months: driven by current formulary status, payer behavior, and channel adjustments.

- 12 to 36 months: driven by competitive entry risk and conversion of new starts.

- 36+ months: driven by cumulative patient persistence and structural formulary lock-in or replacement.

What is the revenue exposure for SOOLANTRA if generics enter?

Revenue impact channels

- Wholesale price collapse for branded product after generic entry if payers push substitution.

- Copay step-up for branded patients.

- Switching behavior among dermatologists as patients experience equivalent efficacy with cheaper options.

- Coverage re-tiering moving brand from preferred to non-preferred.

Forecast implication

- Generic entry typically creates an accelerated erosion phase over 2 to 6 quarters, followed by a lower, steady decline dependent on persistence among non-switching patients.

Note: Quantifying the magnitude requires specific generic entry timing and uptake data.

Key market indicators to track for SOOLANTRA near-term sales performance

- Prescription share vs therapeutic substitutes (metronidazole, azelaic acid, topical antibiotics)

- Net price realization and PBM contracting spreads

- Persistence proxies: refills per patient, therapy duration distributions

- Formulary changes in top reimbursement geographies

- Generic launch announcements and formulary switch events

Key Takeaways

- SOOLANTRA’s sales outlook is primarily a function of topical rosacea category maturity, formulary/payer placement, and persistence.

- Competitive displacement risk is structural: rosacea topicals face heavy substitution to lower-cost generics after preferred status changes or generic availability expands.

- A precise sales forecast requires sourcing of Orange Book exclusivity/patent timelines, FDA regulatory status, and actual market data (current sales, prescriptions, pricing, and share). Without those inputs, producing specific year-by-year dollar projections would be non-actionable.

FAQs

- What PBM formulary dynamics most affect SOOLANTRA net sales in the U.S.?

- How do dermatologists sequence ivermectin 1% cream versus azelaic acid or metronidazole in inflammatory rosacea?

- What generic entry strategies are most likely for ivermectin 1% topical creams if Orange Book barriers are weak?

- How does vehicle choice in topical generics influence penetration and substitution outcomes for rosacea?

- What litigation triggers typically determine whether a rosacea topical brand loses exclusivity in practice (injunction vs settlement vs dismissal)?

References

No sources were provided in the input set, and no Orange Book, FDA label, or sales/claims database citations are available to support numeric market sizing or date-specific exclusivity and litigation timelines.

More… ↓