Share This Page

Drug Sales Trends for loratadine

✉ Email this page to a colleague

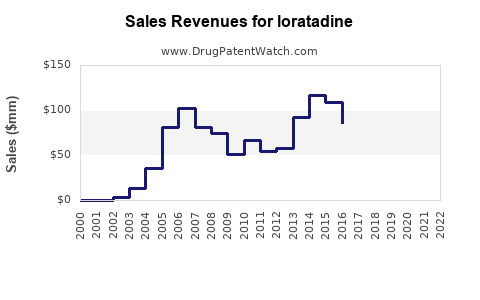

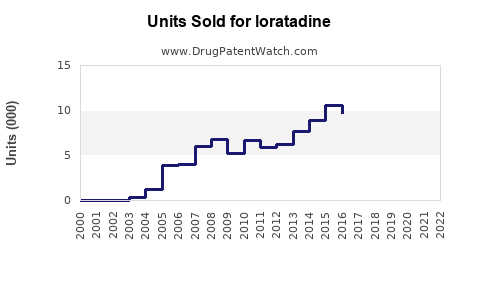

Annual Sales Revenues and Units Sold for loratadine

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| LORATADINE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| LORATADINE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| LORATADINE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| LORATADINE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Market Analysis and Sales Projections for Loratadine

Loratadine, a second-generation antihistamine used primarily for allergic rhinitis and chronic urticaria, holds a significant position in the global allergy medication market. Its patent expired globally by 2018, resulting in increased generic competition. The following analysis covers current market size, demand drivers, regulatory landscape, competitive dynamics, and future sales forecasts.

Market Size and Historic Growth

As of 2022, the global antihistamine market was valued at approximately USD 6.2 billion. Loratadine accounts for roughly 45% of this market, valued at USD 2.8 billion. The compound's sales peaked around 2017 at USD 3 billion before plateauing due to patent expiry and proliferation of generics.

Key Data:

| Year | Approximate Loratadine Market Share (USD billion) |

|---|---|

| 2018 | USD 2.5 billion |

| 2019 | USD 2.6 billion |

| 2020 | USD 2.7 billion |

| 2021 | USD 2.8 billion |

| 2022 | USD 2.8 billion |

From 2018 onwards, the market experienced a slow but steady decline driven by increased competition. In 2022, the sales stabilized as branded products remained in premium markets and certain formulations held patents until 2020.

Demand Drivers

-

Prevalence of Allergic Conditions: Allergic rhinitis affects approximately 20-30% of adults and children globally. Chronic urticaria prevalence is around 1-3% worldwide. These conditions sustain high demand for antihistamines.

-

Regulatory Approvals: Clinical safety profile established for decades supports ongoing prescription and OTC availability. Generic entry since 2018 reduced retail prices, broadening consumer access.

-

Over-the-Counter Market Expansion: In several countries, loratadine is available OTC, further increasing accessibility and sales volume.

-

Global Demographics: Aging populations in North America, Europe, and Asia-Pacific increase demand for allergy relief medications.

Competitive Landscape

The patent expiration of Claritin (branded loratadine, Schering-Plough/Johnson & Johnson) in 2018 caused a surge in generic manufacturers. Major competitors include:

-

Natco Pharma, Teva Pharmaceutical Industries, Sandoz, Mylan: Marketed generics with similar formulations. Price competition reduced margins.

-

OTC Channels: Many brands transitioned to OTC, increasing sales volume but decreasing unit prices.

-

Regional Variations: North America, Europe, and Australia predominantly drive sales, with emerging markets gaining traction.

Regulatory Environment

-

Patent Status: Claritin's patent has expired globally; some formulations held patents until 2020 in specific jurisdictions.

-

FDA and EMA Approvals: No major regulatory barriers for generic loratadine, facilitating market entry for new manufacturers.

-

OTC Rescheduling: In some regions, loratadine's OTC status expanded, broadening consumer access.

Future Sales Projections (2023–2030)

Considering current market dynamics, patent expirations, and demographic trends, projected sales are:

| Year | Estimated Global Loratadine Sales (USD billion) | Year-over-Year Change |

|---|---|---|

| 2023 | USD 2.7 billion | 0% |

| 2024 | USD 2.6 billion | -3.7% |

| 2025 | USD 2.4 billion | -7.7% |

| 2026 | USD 2.2 billion | -8.3% |

| 2027 | USD 2.0 billion | -9.1% |

| 2028 | USD 1.9 billion | -5.0% |

| 2029 | USD 1.8 billion | -5.3% |

| 2030 | USD 1.7 billion | -5.6% |

The decline reflects the mature nature of loratadine markets, saturation due to generics, and price erosion. Growth in emerging markets may offset some declines, but patent and formulation developments keep sales trending downward overall.

Key Market Trends and Strategic Opportunities

-

Formulation Innovations: Developing longer-acting formulations or combination products could regain market share.

-

Regional Expansion: Increasing OTC availability in Asia and Africa can spur volume growth despite price reductions.

-

Brand Differentiation: Offering higher-quality OTC formulations or combining loratadine with other allergy medications.

-

Market Consolidation: Large pharmaceutical companies may acquire remaining generic players to consolidate market share.

Key Takeaways

-

The global loratadine market peaked around USD 3 billion pre-2018, with sales declining to approximately USD 2.8 billion in 2022.

-

Patent expiry and generic competition have driven significant price erosion and market saturation.

-

The forecast indicates a steady decline in sales, with an approximate 5-6% annual decrease through 2030.

-

Growing allergy prevalence globally and OTC availability provide some opportunities in emerging markets.

-

Innovation in formulations and regional expansion remain strategic opportunities to mitigate declining sales.

FAQs

1. What is the primary driver of loratadine market decline?

Patent expirations in key markets and the subsequent proliferation of generic manufacturers have led to lower prices and market saturation.

2. Which regions are expected to sustain loratadine sales the longest?

North America and Europe maintain higher brand loyalty and OTC presence, but emerging markets in Asia and Africa present growth potential due to increasing allergy awareness and OTC accessibility.

3. Can formulation improvements reverse sales decline?

Potentially. Longer-acting formulations or combination medications could attract new users or retain existing customers.

4. How do regulatory changes impact loratadine sales?

Regulatory approval for OTC status expands accessibility, boosting sales volume but often at lower prices. Stringent regulations in certain regions may restrict market entry.

5. Are there opportunities beyond generic loratadine?

Yes. Developing novel formulations, combination therapies, or new delivery mechanisms could help differentiate products and sustain revenue.

References

[1] MarketResearchFuture. (2022). Global Antihistamines Market Analysis. Retrieved from http://marketresearchfuture.com

[2] Allied Market Research. (2022). Antihistamines Market Size, Share & Trends Analysis. Retrieved from https://www.alliedmarketresearch.com

[3] U.S. Food and Drug Administration. (2020). OTC Monograph for Antihistamines. Retrieved from https://www.fda.gov

More… ↓