Share This Page

Drug Sales Trends for irbesartan

✉ Email this page to a colleague

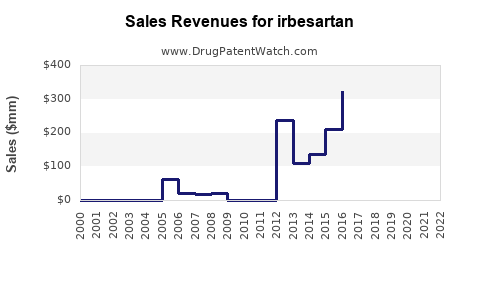

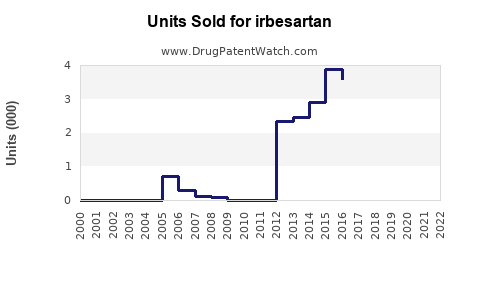

Annual Sales Revenues and Units Sold for irbesartan

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| IRBESARTAN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| IRBESARTAN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| IRBESARTAN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| IRBESARTAN | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| IRBESARTAN | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Irbesartan: Patent Expiration and Market Landscape Analysis

Irbesartan, an angiotensin II receptor blocker (ARB), faces widespread patent expiration, opening the market to generic competition and impacting originator sales. This analysis details the current patent status, competitive landscape, and projected market evolution for Irbesartan.

What is the Patent Status of Irbesartan?

The primary patents covering Irbesartan have expired in major markets. The compound patent for Irbesartan, initially held by Bristol-Myers Squibb and Sanofi-Synthelabo, expired in the United States in 2010 and in Europe in 2011.

- US Patent Expiration: Original compound patents for Irbesartan expired in 2010 [1].

- European Patent Expiration: Similar expirations occurred across key European markets by 2011 [1].

- Key Formulations & Manufacturing Process Patents: While compound patents have expired, some secondary patents related to specific crystalline forms, manufacturing processes, or combination therapies may still be in effect or have recently expired. For example, patents pertaining to specific polymorphs or novel synthesis routes could have extended market exclusivity in certain niches or for specific manufacturers. However, these generally do not prevent the market entry of generic Irbesartan if the core compound is off-patent.

Who are the Key Manufacturers and Competitors in the Irbesartan Market?

The Irbesartan market is characterized by the presence of the original innovators and a significant number of generic manufacturers.

Innovator Companies

- Sanofi: Co-developer of Irbesartan (marketed as Avapro in the US and Karvea in Europe) [2].

- Bristol-Myers Squibb: Co-developer of Irbesartan (marketed as Avapro in the US) [2].

Major Generic Manufacturers

Following patent expirations, numerous pharmaceutical companies have entered the market with generic Irbesartan. Key players include:

- Teva Pharmaceutical Industries Ltd.

- Mylan N.V. (now Viatris)

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy's Laboratories Ltd.

- Lupin Ltd.

- Aurobindo Pharma Ltd.

- Cipla Ltd.

- Accord Healthcare Ltd.

These companies compete on price, quality, and market access. The availability of multiple generic options leads to significant price erosion.

What is the Market Size and Sales Performance of Irbesartan?

The global market for Irbesartan has experienced a substantial decline in revenue for the originator products due to generic competition. However, the overall volume of Irbesartan prescriptions remains high, driven by its established efficacy and affordability as a generic drug.

- Peak Sales for Originator Products: Before widespread generic entry, Avapro/Karvea achieved peak annual sales exceeding $2.5 billion globally [3].

- Current Market Dynamics: Post-patent expiration, the combined sales of generic Irbesartan products are substantial in terms of volume, but the average selling price (ASP) is significantly lower than that of the branded product. Market research reports focusing on the ARB class indicate that generic Irbesartan continues to hold a notable share of the hypertension treatment market.

- Projected Market Value: While precise, up-to-the-minute global sales figures for generic Irbesartan are fragmented across multiple manufacturers, the overall therapeutic class market for ARBs is valued in the tens of billions of dollars annually. Irbesartan, as a widely prescribed generic, contributes a significant portion to this market's volume, even if its individual brand revenue is diminished.

How Does Irbesartan Compare to Other Angiotensin II Receptor Blockers (ARBs)?

Irbesartan belongs to the ARB class, a group of drugs that block the action of angiotensin II, a hormone that causes vasoconstriction and stimulates aldosterone secretion, thereby lowering blood pressure.

- Mechanism of Action: All ARBs share the same mechanism of action, blocking the AT1 receptor.

- Efficacy: Clinical trials demonstrate comparable efficacy in lowering blood pressure and managing cardiovascular risk among various ARBs, including Irbesartan, Losartan, Valsartan, Candesartan, and Olmesartan [4].

- Key Differences: Subtle differences exist in their pharmacokinetic profiles, metabolism, and potential side effects, though overall safety and efficacy are generally considered similar for most indications [4].

- Market Positioning: Losartan is often the most widely prescribed ARB due to its earlier patent expiry and established generic status. Valsartan has also seen significant generic penetration. Irbesartan remains a competitive option, particularly where physicians have established prescribing habits or specific patient responses favor it.

- Indications: Irbesartan is primarily indicated for the treatment of hypertension and diabetic nephropathy in patients with type 2 diabetes and hypertension [5]. Other ARBs may have additional or slightly different approved indications.

What are the Projected Market Trends for Irbesartan?

The market for Irbesartan is expected to remain stable in terms of volume, driven by its established role in hypertension management. Price competition will continue to be the dominant factor.

- Generic Market Dominance: The market will continue to be dominated by generic manufacturers.

- Price Erosion: Ongoing price erosion due to intense competition among generic suppliers will persist.

- Therapeutic Class Dynamics: The ARB class as a whole faces competition from other antihypertensive drug classes, including ACE inhibitors, calcium channel blockers, and diuretics, as well as newer classes like SGLT2 inhibitors (though primarily for cardiovascular outcomes in specific populations).

- Market Volume Stability: Prescription volumes are expected to remain relatively stable, reflecting the ongoing need for effective and affordable hypertension treatment.

- Emerging Markets: Growth opportunities may exist in emerging markets where access to branded generics or established generics is expanding.

- Combination Therapies: While the core Irbesartan patent has expired, future market activity might involve novel fixed-dose combination products (e.g., Irbesartan with a diuretic or calcium channel blocker) if new patents are granted for specific formulations or synergistic benefits. However, these are less likely to drive significant growth for Irbesartan as a standalone molecule.

What are the Regulatory Considerations for Irbesartan?

Regulatory bodies play a crucial role in ensuring the quality, safety, and efficacy of generic Irbesartan.

- FDA Approval Process (US): Generic manufacturers must demonstrate bioequivalence to the reference listed drug (RLD) through Abbreviated New Drug Applications (ANDAs) [6].

- EMA Approval Process (EU): Similar processes exist in the European Union, requiring demonstration of quality, safety, and efficacy through marketing authorization applications.

- Quality Standards: Manufacturers must adhere to strict Good Manufacturing Practices (GMP) to ensure consistent product quality.

- Pharmacovigilance: Post-market surveillance and pharmacovigilance activities are mandatory to monitor for adverse events.

- Labeling Requirements: Generic products must carry appropriate labeling, including indications, contraindications, warnings, and adverse reactions, consistent with the RLD.

Key Takeaways

- Irbesartan's core compound patents have expired globally, paving the way for extensive generic competition.

- The market is characterized by numerous generic manufacturers competing primarily on price, leading to significant price erosion from originator sales.

- While originator sales have declined sharply, the volume of Irbesartan prescriptions remains substantial due to its established efficacy and affordability.

- Irbesartan competes within the broader ARB class, where efficacy and safety profiles are generally similar across agents, leading to therapy choice often being driven by cost and physician preference.

- Market projections indicate continued dominance by generic players, stable prescription volumes, and ongoing price pressures.

Frequently Asked Questions

-

Q1: Can originator companies re-establish market exclusivity for Irbesartan? Originator companies typically cannot re-establish market exclusivity for the base compound once primary patents expire. Limited opportunities might arise through novel formulations, new combination therapies, or specific manufacturing process patents, but these are less common for older, off-patent molecules.

-

Q2: What is the primary therapeutic advantage of Irbesartan over older antihypertensive drugs? Irbesartan, as an ARB, targets the renin-angiotensin-aldosterone system (RAAS) with potentially fewer side effects (e.g., cough) compared to ACE inhibitors. Its efficacy in reducing blood pressure and protecting kidney function in diabetic patients is a key therapeutic benefit.

-

Q3: How do generic Irbesartan prices compare to branded Avapro/Karvea? Generic Irbesartan prices are typically 70-90% lower than the peak prices of branded Avapro/Karvea, reflecting the intense competition and the removal of R&D and marketing costs associated with branded products.

-

Q4: Are there any significant safety concerns unique to Irbesartan compared to other ARBs? While all ARBs carry similar warnings regarding pregnancy, hypotension, and hyperkalemia, Irbesartan has not demonstrated significantly unique safety concerns that differentiate it substantially from other ARBs in widespread clinical use. Individual patient responses can vary.

-

Q5: What is the expected impact of biosimil drugs on the Irbesartan market? Biosimil drugs apply to biologic medications, not small-molecule drugs like Irbesartan. Therefore, biosimil competition is not a factor in the Irbesartan market. The market is solely influenced by generic competition.

Citations

[1] U.S. Food & Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. Retrieved from [FDA Orange Book database] [2] Sanofi. (2007). Bristol-Myers Squibb and Sanofi-Aventis Announce Agreement to Settle Avapro Litigation. [Press Release]. [3] Company Annual Reports (various, e.g., Bristol-Myers Squibb, Sanofi). Data points aggregated from historical financial disclosures. [4] Consensus Statement on the Management of Hypertension. (2018). American Heart Association/American College of Cardiology. [5] Plosker, G. L., & Jarvis, B. (2006). Irbesartan. Drugs, 66(2), 183-200. [6] U.S. Food & Drug Administration. (2020). ANDA Basics. Retrieved from [FDA ANDA Information]

More… ↓