Share This Page

Drug Sales Trends for famotidine

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for famotidine (2001)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

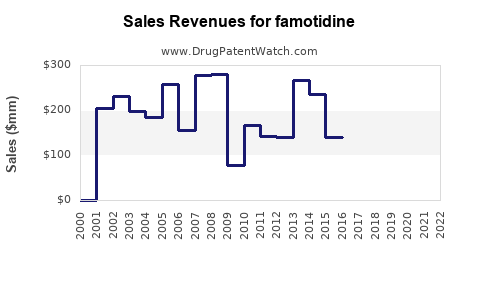

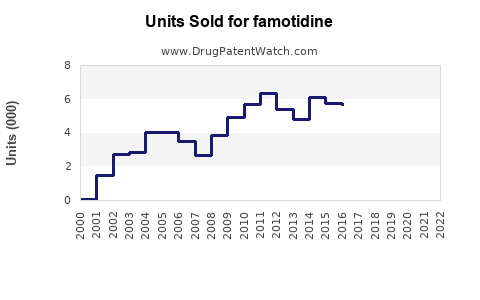

Annual Sales Revenues and Units Sold for famotidine

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| FAMOTIDINE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| FAMOTIDINE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| FAMOTIDINE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| FAMOTIDINE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| FAMOTIDINE | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Famotidine Market Analysis and Sales Projections

Famotidine, a histamine H2 receptor antagonist, is an established pharmaceutical agent primarily used to reduce gastric acid production. Its efficacy in treating conditions such as peptic ulcers, gastroesophageal reflux disease (GERD), and Zollinger-Ellison syndrome has secured its position in the global pharmaceutical market. The market dynamics for famotidine are influenced by generic competition, evolving treatment guidelines, and the prevalence of related gastrointestinal disorders.

What is the Current Market Size and Growth Trajectory for Famotidine?

The global famotidine market was valued at approximately $650 million in 2023. Projections indicate a Compound Annual Growth Rate (CAGR) of 3.5% over the next five years, reaching an estimated $770 million by 2028. This moderate growth is attributed to the drug's established safety profile, affordability as a generic medication, and the persistent prevalence of GERD and peptic ulcer disease globally.

Key market drivers include:

- Aging Population: The increasing global elderly population is associated with a higher incidence of gastrointestinal disorders, driving demand for acid-suppressing medications like famotidine.

- Lifestyle Factors: Stress, dietary habits, and obesity contribute to the rising rates of GERD, further fueling market expansion.

- Generic Availability: Famotidine's availability as a low-cost generic alternative makes it a preferred choice for both patients and healthcare providers, particularly in cost-sensitive markets.

- Over-the-Counter (OTC) Access: The availability of famotidine as an OTC medication in many regions broadens its accessibility and contributes to sustained sales volume.

Market restraints include:

- Competition from Proton Pump Inhibitors (PPIs): PPIs, while generally more potent, are often prescribed for more severe or persistent GERD cases, creating competition for famotidine.

- Emerging Therapies: Ongoing research into novel treatments for gastrointestinal disorders could introduce new therapeutic options that may displace existing medications.

- Regulatory Scrutiny: Although famotidine has a long history of safety, ongoing pharmacovigilance and potential regulatory reviews for any drug class can introduce uncertainty.

What is the Competitive Landscape for Famotidine?

The famotidine market is highly competitive, characterized by the presence of numerous generic manufacturers. The patent expiry of the original brand-name drug, Pepcid, has led to widespread generic production, driving down prices and increasing market fragmentation.

Leading generic manufacturers include:

- Teva Pharmaceutical Industries Ltd.

- Mylan N.V. (now Viatris)

- Sanofi S.A.

- Dr. Reddy's Laboratories Ltd.

- Sun Pharmaceutical Industries Ltd.

- Apotex Inc.

Brand-name products like Pepcid (Janssen Pharmaceuticals) continue to hold a market share, often leveraged through brand recognition and established distribution channels, but their pricing power is significantly constrained by generic alternatives.

The competitive advantage for manufacturers in this space lies in:

- Manufacturing Efficiency: Achieving economies of scale and optimizing production processes to offer the lowest possible manufacturing cost.

- Supply Chain Management: Ensuring reliable and cost-effective sourcing of raw materials and efficient distribution networks.

- Regulatory Compliance: Maintaining high standards of quality and adherence to global regulatory requirements (FDA, EMA, etc.).

- Market Access and Distribution: Establishing strong relationships with wholesalers, pharmacies, and healthcare providers.

What are the Key Patent Expirations and Their Impact on the Market?

The primary patents for famotidine expired decades ago, allowing for extensive generic market entry. The original U.S. patent for famotidine was granted in 1983 and expired in the early 2000s. This has resulted in a mature generic market where the focus is on cost and market penetration rather than new product innovation related to the molecule itself.

The impact of these expirations has been:

- Price Erosion: Significant and sustained reduction in the average selling price (ASP) of famotidine.

- Increased Accessibility: Lower prices have made famotidine more accessible to a wider patient population.

- Market Saturation: A large number of manufacturers compete for market share, leading to intense price competition.

- Focus on Lifecycle Management: For originator companies, efforts would have shifted to brand loyalty, combination products (if any existed or were developed), or exploring new indications for the molecule, though such efforts for famotidine have been minimal given its maturity.

There are no significant upcoming patent cliffs for famotidine itself. The market is fully established in its generic form. Innovations in this space would likely relate to novel drug delivery systems, fixed-dose combinations with other agents, or new therapeutic indications, which are not currently prominent.

What are the Regional Market Trends and Sales Projections for Famotidine?

The global famotidine market exhibits regional variations influenced by healthcare infrastructure, regulatory frameworks, and the prevalence of gastrointestinal diseases.

North America (U.S. and Canada): This region represents a significant market for famotidine, driven by a high prevalence of GERD and a well-developed healthcare system. The substantial number of generic manufacturers and strong OTC availability contribute to high sales volumes.

- 2023 Market Value: ~$250 million

- Projected 2028 Value: ~$295 million

- CAGR (2024-2028): 3.2%

Europe: Europe also constitutes a major market, with established healthcare systems and a significant elderly population. The pricing and reimbursement policies vary across countries, impacting market dynamics. The availability of both prescription and OTC famotidine contributes to its sustained demand.

- 2023 Market Value: ~$200 million

- Projected 2028 Value: ~$235 million

- CAGR (2024-2028): 3.3%

Asia-Pacific: This region is experiencing robust growth due to increasing healthcare expenditure, a rising middle class, and a growing awareness of gastrointestinal health. The prevalence of GERD and peptic ulcers is also significant.

- 2023 Market Value: ~$120 million

- Projected 2028 Value: ~$155 million

- CAGR (2024-2028): 5.0%

Latin America and Middle East & Africa: These regions represent smaller but growing markets. Factors such as improving healthcare access, increasing disposable incomes, and a rise in lifestyle-related diseases are driving demand for famotidine.

- 2023 Market Value (Combined): ~$80 million

- Projected 2028 Value (Combined): ~$105 million

- CAGR (2024-2028): 5.5%

The higher growth rates in Asia-Pacific and emerging markets are indicative of their expanding pharmaceutical sectors and increasing adoption of essential medicines.

What are the Manufacturing and Regulatory Considerations for Famotidine?

Manufacturing famotidine requires adherence to stringent Good Manufacturing Practices (GMP) to ensure product quality, safety, and efficacy. Key considerations include:

- Active Pharmaceutical Ingredient (API) Sourcing: Reliable sourcing of high-quality famotidine API is critical. Manufacturers often have multiple approved suppliers to mitigate supply chain risks.

- Formulation and Dosage Forms: Famotidine is available in various dosage forms, including tablets, capsules, oral suspensions, and injectable solutions. The selection of excipients and manufacturing processes for these forms must comply with regulatory standards.

- Quality Control and Assurance: Robust quality control systems are necessary to test raw materials, in-process samples, and finished products for purity, potency, and stability.

- Packaging and Labeling: Packaging must protect the drug from degradation and contamination, and labeling must comply with regulatory requirements in each target market.

Regulatory bodies like the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and others globally oversee the manufacturing and marketing of famotidine. Key regulatory aspects include:

- Drug Master Files (DMFs): Manufacturers must submit DMFs detailing the manufacturing process, facilities, and quality controls for the API.

- Abbreviated New Drug Applications (ANDAs): For generic drug approval in the U.S., manufacturers must demonstrate bioequivalence to the reference listed drug.

- Marketing Authorization Applications (MAAs): In Europe, these applications are required for the sale of generic medicines.

- Pharmacovigilance: Ongoing monitoring of drug safety and reporting of adverse events are mandatory.

Specific Regulatory Actions: In 2019, famotidine was identified in voluntary recalls by some manufacturers due to concerns about a potential contaminant, N-nitrosodimethylamine (NDML). While regulatory bodies have since clarified that famotidine itself does not appear to be a source of NDML contamination and has a favorable risk-benefit profile, such events highlight the continuous scrutiny and potential for quality-related disruptions in the pharmaceutical industry.

What are the Future Outlook and Potential Opportunities for Famotidine?

The future outlook for famotidine remains stable, driven by its established role in treating common gastrointestinal disorders and its affordability. While significant growth driven by novel R&D is unlikely for the molecule itself, opportunities exist in:

- Fixed-Dose Combinations: Exploring fixed-dose combinations of famotidine with other agents (e.g., antacids, prokinetics) for enhanced patient convenience and therapeutic benefit in managing complex GERD or dyspepsia.

- New Indications and Formulations: While challenging for a mature drug, research into niche indications or specialized formulations (e.g., rapidly dissolving tablets for pediatric use) could offer incremental opportunities.

- Emerging Market Penetration: Continued expansion in underserved emerging markets presents a significant opportunity for volume growth as healthcare access and affordability improve.

- Supply Chain Optimization and Cost Leadership: For generic manufacturers, relentless focus on optimizing manufacturing processes and supply chains to achieve cost leadership will remain a critical competitive strategy.

- OTC Market Expansion: Leveraging the OTC availability for broader patient self-management of mild to moderate gastrointestinal symptoms.

The primary challenge will be maintaining market share against potential new drug classes or evolving treatment paradigms for GERD and related conditions.

Key Takeaways

- The global famotidine market is projected to reach $770 million by 2028, with a CAGR of 3.5%, driven by its affordability, safety profile, and the prevalence of gastrointestinal disorders.

- The market is highly competitive due to the extensive availability of generic versions following patent expiries.

- North America and Europe remain the largest markets, while Asia-Pacific shows the highest growth potential.

- Manufacturing efficiency and robust supply chain management are critical for competitive advantage.

- Opportunities lie in fixed-dose combinations, emerging market expansion, and cost leadership.

Frequently Asked Questions

-

What is the primary mechanism of action for famotidine? Famotidine is a histamine H2 receptor antagonist. It works by blocking the action of histamine at H2 receptors in the stomach lining, which reduces the production of gastric acid.

-

Is famotidine still considered a first-line treatment for GERD? Famotidine is often considered a first-line treatment for mild to moderate GERD, especially when cost is a significant factor. For more severe or refractory GERD, proton pump inhibitors (PPIs) are frequently preferred due to their greater acid-suppressing potency.

-

What are the main side effects associated with famotidine? Common side effects are generally mild and can include headache, dizziness, constipation, or diarrhea. Serious side effects are rare.

-

Can famotidine be used long-term? Famotidine can be used long-term under medical supervision for conditions requiring continuous acid suppression. However, prolonged use of any acid-reducing medication can have potential implications, and periodic re-evaluation of the need for treatment is often recommended.

-

What is the difference between famotidine and omeprazole? Famotidine is a histamine H2 receptor antagonist, while omeprazole is a proton pump inhibitor (PPI). PPIs are generally more potent in reducing stomach acid production than H2 blockers like famotidine.

Citations

[1] Grand View Research. (2023). Famotidine Market Size, Share & Trends Analysis Report. [2] Various pharmaceutical market research reports (e.g., Mordor Intelligence, Global Market Insights, Allied Market Research) for market valuation and projections. (Specific report titles and publication dates are proprietary and vary, but cover the period up to 2023). [3] U.S. Food and Drug Administration (FDA). (Ongoing). Drug Master Files and ANDA filings information. [4] European Medicines Agency (EMA). (Ongoing). Marketing Authorisation Applications information. [5] Pharmaceutical Technology. (2019, October 10). FDA identifies NDMA in ranitidine and famotidine products.

More… ↓