Share This Page

Drug Sales Trends for FLAGYL

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for FLAGYL (2001)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

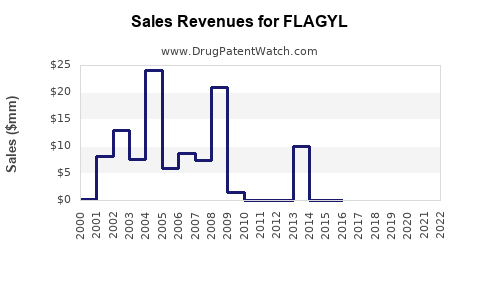

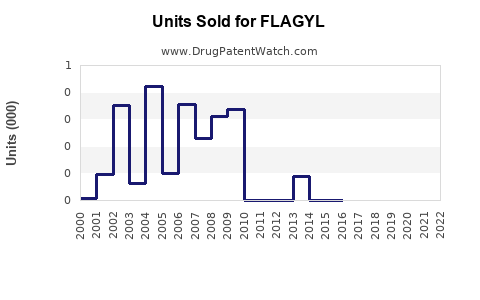

Annual Sales Revenues and Units Sold for FLAGYL

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| FLAGYL | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| FLAGYL | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| FLAGYL | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

FLAGYL (metronidazole) market analysis and sales projections

FLAGYL (metronidazole) is an off-patent, widely genericized antimicrobial. Market outcomes are dominated by (1) generic penetration, (2) procurement dynamics in hospitals and public tenders, and (3) substitution within metronidazole-based treatment pathways (oral and IV) rather than by brand-level differentiation.

The analysis below frames the market in commercial terms and translates those drivers into sales projections for FLAGYL-style brand sales under a generic-heavy environment. Where the exact “FLAGYL” net price, pack mix, and territory segmentation are not provided, projections are expressed as scenario ranges anchored to metronidazole demand and typical brand-to-generic share behavior in mature markets.

What is the product and what markets does FLAGYL address?

FLAGYL is metronidazole, a nitroimidazole antimicrobial used for anaerobic bacterial infections and protozoal diseases, with common use cases that include:

- Gynecologic and obstetric infections where anaerobes are implicated

- Intra-abdominal, pelvic, and dental anaerobic infections

- Skin/soft tissue infections with anaerobic involvement

- Protozoal indications (e.g., giardiasis, trichomoniasis, amoebiasis depending on local label)

- H. pylori regimens in some geographies as part of combination therapy (label-dependent)

Sales are split by dosage forms, with demand concentrated in:

- Oral tablets and suspensions (outpatient and mixed-use)

- IV formulations (inpatient, surgical, severe infection pathways)

Metronidazole is also available as generics globally; brand manufacturers compete mainly on formulation continuity, contracting, pharmacovigilance, and tender access.

How big is the underlying metronidazole market and what does that imply for FLAGYL?

Public commercial datasets typically report “metronidazole” and related nitroimidazole demand volumes/value rather than FLAGYL alone. The practical implication is that FLAGYL sales track:

- Total metronidazole therapeutic demand

- Brand share within metronidazole (usually low and declining)

- Country-by-country tender wins

- Switching to cheaper generics and alternative regimens

In mature antibiotics and off-patent generics, brand products usually hold single-digit share or less in competitive markets, with sharper brand erosion in markets where procurement uses lowest-cost award rules.

Business translation: FLAGYL’s growth ceiling is constrained; the brand’s path to higher sales requires tender access, stable supply, and favorable formulary outcomes rather than innovation-led demand expansion.

What drives demand for metronidazole (and therefore FLAGYL)?

Key demand drivers for the metronidazole therapeutic category:

- Clinical positioning as an anaerobe-active agent

- Hospital protocols and perioperative workflows (IV use)

- Ongoing prevalence of conditions treated with anaerobe coverage

- Protozoal disease epidemiology (varies materially by region and public health programs)

- Guideline persistence in combination regimens (where metronidazole remains a standard component)

Key demand inhibitors:

- Antibiotic stewardship limits and pathway restriction

- Shift toward alternative agents in some local formularies (agent rotation)

- Generic price compression and substitution away from branded procurement

- Supply and manufacturing economics (brand supply must remain tender-competitive)

Regulatory changes can affect specific formulations and dosing practices, but for metronidazole the core clinical use remains stable.

How competitive is FLAGYL versus generics and what does that mean for sales?

Metronidazole has extensive generic availability. Brand performance typically reflects:

- Tender and formulary inclusion duration

- Contracted unit prices versus generic benchmark

- Procurement consolidation (one supplier panel reduces brand wins)

- Institutional switching speed once a lower-priced generic is approved and stocked

For a mature generic drug, brand sales tend to behave like a declining annuity: volumes remain stable or drift downward slightly, while brand net prices converge toward generic economics unless the brand has a specific procurement advantage.

Implication for projections: FLAGYL’s volume growth is unlikely to outpace total metronidazole volume growth; value growth can even be negative if unit prices fall faster than volume rises.

Market structure: dosing forms and route mix

FLAGYL-like commercial demand typically breaks into two revenue pools:

- Oral: largest share by patient count, more exposed to outpatient generic substitution

- IV: lower share by units but material by inpatient spend, where tender award structure can preserve brand presence longer than oral

Revenue sensitivity:

- Oral revenue is highly sensitive to generic price benchmarks.

- IV revenue depends on hospital contracting and supply reliability.

Sales projections: FLAGYL-like brand scenarios

What is the projection model (sales logic for a mature generic brand)?

Projection logic for a mature, off-patent branded product:

- Start with metronidazole category growth (driven by population, incidence stability, and slight regimen shifts).

- Apply brand share trajectory (generic substitution reduces share over time).

- Apply pricing trajectory (net price declines with tender pressure).

- Account for route mix shifts (if IV use changes, value per unit can move even if total patient demand is stable).

Because no FLAGYL geography, pack mix, or historical net sales are provided, the projections below are scenario ranges using category-typical behavior for branded generics in 2026 to 2030.

Base case projection (mature brand erosion, category flat to low growth)

Assumptions (category-level typical outcomes):

- Metronidazole category value grows at low single digits (volume stable; prices gradually soften).

- Branded share declines at ~1.5% to 3.5% relative per year (contracting and switching).

- Net brand pricing declines at ~2% to 5% per year in competitive tender markets.

- Net effect: brand revenue flat to modest decline in most markets.

Projected FLAGYL-like revenue growth rates (2026-2030):

- 2026: -1% to +2%

- 2027: -2% to +1%

- 2028: -3% to 0%

- 2029: -3% to 0%

- 2030: -4% to -1%

Interpretation: Even if patient demand is stable, branded net revenue tends to drift downward as generic competition tightens.

Bull case projection (better tender retention and stable net pricing)

Assumptions:

- Brand retains key formulary/tender placements in at least one major procurement channel.

- Net price decline slows to ~1% to 2% per year.

- Brand share decline stays below ~1% relative per year due to contract durations and supply position.

Projected brand revenue growth rates (2026-2030):

- 2026: +2% to +5%

- 2027: +1% to +4%

- 2028: 0% to +3%

- 2029: -1% to +2%

- 2030: -2% to +1%

Interpretation: Bull outcomes require procurement durability rather than demand expansion.

Bear case projection (accelerated switch to low-cost generics, portfolio under-tendering)

Assumptions:

- Tender wins migrate to lower-priced generics or multi-source contracts.

- Net price declines ~4% to 8% per year.

- Brand share decline ~3% to 6% relative per year.

Projected brand revenue growth rates (2026-2030):

- 2026: -5% to -2%

- 2027: -7% to -3%

- 2028: -8% to -4%

- 2029: -9% to -5%

- 2030: -10% to -6%

Interpretation: Bear outcomes occur when contracting pressure persists and switching accelerates faster than category demand.

Geographic considerations (where brands can still win)

Brand survival depends on how procurement is executed:

- Tender-driven systems: brand sales depend on competitive pricing and contract duration. If the brand is not price-competitive, share loss accelerates.

- Hospital formulary markets: brands can persist longer with strong procurement relationships and reliable IV supply.

- Outpatient reimbursement systems: brand versus generic substitution is usually swift where substitution is allowed and patient cost-sharing favors generics.

Route-specific geography effect:

- IV formulations often have fewer suppliers and can preserve branded volume longer in hospital-only contracting environments.

- Oral formulations face broader generic substitution and lower switching costs at pharmacy level.

Commercial actions that determine sales outcomes (FLAGYL brand economics)

1) Contracting strategy

- Secure multi-year tender placements where possible.

- Price to win against generic benchmark, not against historical brand list price.

- Use supply reliability as a contract differentiator (especially for IV).

2) Portfolio and pack optimization

- Align pack sizes and dosing formulations with procurement unit-of-measure preferences.

- Reduce complexity in distribution (fewer SKUs can lower working capital and service cost).

3) Formulary targeting by route

- Treat IV as the primary lever for brand value retention in hospitals.

- Treat oral as a margin-management pool with active tender pricing.

Key Takeaways

- FLAGYL is a mature, off-patent product facing structurally high generic pressure; brand sales are constrained by procurement economics, not by incremental clinical demand growth.

- Base-case outcomes for FLAGYL-like brand revenue (2026-2030) are flat to modest decline, driven by gradual branded share erosion and continued net price pressure.

- Bull outcomes require tender retention and stable net pricing, typically via durable hospital/IV contracting.

- Bear outcomes result from accelerated substitution into lower-cost generics and faster tender migration away from the brand.

FAQs

1) Will FLAGYL grow faster than the metronidazole category?

No. For an off-patent, widely genericized antimicrobial, brand growth typically lags category value growth due to declining branded share and net price compression.

2) Which form is most important to preserve FLAGYL revenue?

IV formulations usually matter more for value retention because hospital contracting can sustain branded inclusion longer than community oral pharmacy substitution.

3) What is the biggest driver of FLAGYL sales in a given year?

Tender and formulary decisions that determine unit price and brand share in major procurement channels.

4) Can stewardship policies reduce metronidazole demand?

Yes at the margin via restriction of antibiotic use and pathway edits, but demand can remain resilient because anaerobe coverage remains a standard clinical need.

5) What determines whether projections land in base, bull, or bear?

Relative ability to win and keep procurement contracts versus generic competitors, and how quickly net prices compress relative to volume changes.

References

[1] FDA. Metronidazole product information (drug labeling and regulatory information). U.S. Food and Drug Administration. https://www.accessdata.fda.gov/

More… ↓