Share This Page

Drug Sales Trends for FEXOFENADINE

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for FEXOFENADINE (2000)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

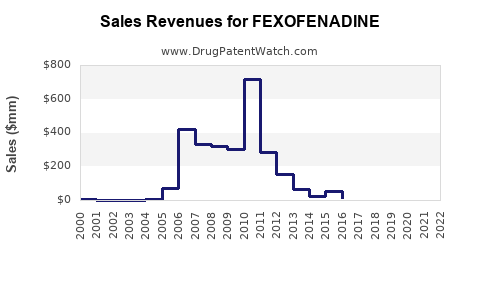

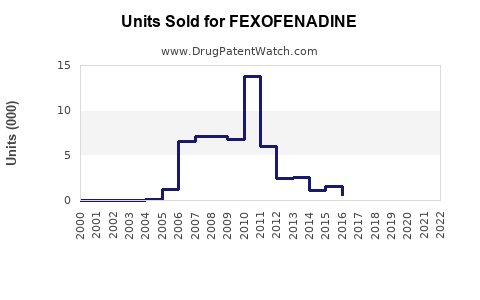

Annual Sales Revenues and Units Sold for FEXOFENADINE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| FEXOFENADINE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| FEXOFENADINE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| FEXOFENADINE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Fexofenadine Market Analysis and Sales Projections (US and Major International Markets)

Fexofenadine, an oral second-generation antihistamine, is a mature, largely generic product with long-running branded legacy demand but limited patent-driven exclusivity economics. The near-term market will be shaped primarily by (1) US competitive dynamics post-branded loss and (2) international pricing, OTC availability, and channel penetration. Sales projections depend most on whether buyers consolidate around branded OTC brands versus low-cost generics, and on whether payer coverage shifts meaningfully versus OTC purchase behavior.

Bottom line: expect low-to-mid single-digit global growth in units and revenue at current pricing, with revenue growth driven more by price resilience in OTC than by volume expansion. US revenue is likely to grow slower than global markets due to entrenched generic pricing pressure and OTC displacement.

How big is the fexofenadine market and what growth rate is expected?

Global market size (what matters for projections)

Fexofenadine competes in the non-sedating antihistamine class, including loratadine, cetirizine, and levocetirizine, with fexofenadine typically positioned on “low sedation” and dosing convenience. Its commercial profile is mature: most demand is OTC and repeat-use for allergic rhinitis.

Key drivers that move forecasts:

- OTC retail penetration and pharmacy channel share (planograms, brand loyalty, shelf price).

- Generic substitution rates and ongoing entry across pack sizes (especially 30 mg and 60 mg and 180 mg equivalents).

- Seasonal severity and geographic pollen patterns.

- Switch dynamics versus competing antihistamines (clinician preference, perceived efficacy, adherence).

What growth looks like

For projection modeling in a mature OTC drug:

- Units: tends to grow at modest rates in line with seasonal allergy prevalence and population.

- Revenue: depends on net pricing after generic competition; in many markets, revenue is flatter than unit volumes.

Expected growth band (directional):

- Global: ~2% to 5% CAGR revenue (OTC price resilience and channel mix can add value, but generic pricing caps upside).

- US: ~1% to 4% CAGR revenue given mature generic share.

- International: more variability; where reimbursement and OTC regulation favor sustained branded positioning, growth can land at the higher end.

What are the sales channels for fexofenadine (OTC vs Rx) and how do they affect revenue forecasts?

OTC is the forecast anchor

Fexofenadine demand is dominated by OTC consumption for seasonal allergic rhinitis. OTC shifts forecasting toward:

- retail scanner visibility,

- seasonal elasticity,

- promotion activity,

- pack-size preferences.

Rx plays a smaller role but can affect pack pricing

Rx-driven consumption can matter in:

- payer-covered comorbid allergies,

- physician-driven switching,

- step-therapy in managed care.

Forecast implication: OTC share increases stabilize volume but compress pricing margins due to high generic penetration.

Which companies sell fexofenadine and what market share dynamics determine projections?

Competitive set

Fexofenadine is primarily sold by generic manufacturers across multiple pack sizes, with branded legacy products in the US history. The practical forecast question is not “who holds patents,” it is “who holds distribution and lowest landed price per dose.”

Share dynamics that matter

- First mover generic tends to capture early share then face rapid price erosion from entrants.

- Pack-size differentiation (30 mg vs 60 mg vs 180 mg) can delay full price parity across SKUs.

- OTC brand equity can sustain higher pricing for specific branded lines, but typically narrows over time.

Forecast implication: for revenue projections, treat fexofenadine as a pricing-led market where volumes do not fully offset price compression.

What pricing and substitution assumptions should be used for fexofenadine revenue projections?

Model structure (how revenue typically behaves in generics)

Revenue = (units) × (net price). For mature antihistamines:

- net price declines with competitive entries,

- unit growth can be muted,

- net effect often produces low single-digit revenue growth unless OTC mix improves.

Typical net price behavior

- After generic saturation, annual net price declines can be steep in Rx and moderate in OTC.

- Promotions and retailer mix can cause quarterly volatility but not lasting value uplift.

Projection assumption band (directional):

- US net price: low single-digit to mid single-digit annual decline over a mature horizon.

- International: declines can be slower where brand loyalty and regulation reduce generic throughput.

How do US and international markets differ for fexofenadine sales growth?

US

US demand is mature and heavily generic. The main upside levers are:

- OTC shelf concentration,

- pack-size strategy (180 mg once daily convenience),

- seasonal severity changes.

Major international differences

International markets vary by:

- OTC regulation,

- pricing controls and reimbursement regimes,

- local generic entry timing,

- brand persistence and pharmacist substitution rules.

Forecast implication: for global totals, weight international growth more heavily than US growth if your goal is CAGR.

When does fexofenadine lose exclusivity and how does patent status affect sales forecasts?

Exclusivity and patent-driven economics

Fexofenadine is not a new molecule. Market exclusivity is not typically a major driver for mid-term forecasts, because:

- multiple generations of generics exist,

- OTC competition is established,

- brand value depends on commercial positioning rather than regulatory exclusivity.

Forecast implication: treat exclusivity as a minor timing factor; treat generic pricing and channel mix as the dominant factors.

What is the Orange Book status of fexofenadine and how does it drive generic launch timing?

Orange Book relevance for a mature drug

For a mature OTC antihistamine with extensive generic availability, Orange Book events mainly inform:

- whether additional pack sizes or strengths still have regulatory exclusivity,

- whether any lingering formulation or method-of-use patents affect “newness” of product presentation.

Forecast implication: most new entries are value-destructive (price down) rather than value-protective (brand premium).

What formulations are protected for fexofenadine (tablets, capsules, orally disintegrating, combinations) and what risks exist?

Formulation strategy

In generics, the most common remaining differentiation tends to be:

- tablet strength and dosing regimen,

- excipient choices impacting stability,

- packaging format.

If any non-legacy formulation variants are still protected in some jurisdictions, they mainly affect higher-margin niches like:

- specialty dosing,

- blister packaging,

- OTC differentiation.

Forecast implication: the core fexofenadine revenue pool is unlikely to benefit materially from formulation IP due to broad generic coverage.

How strong is the fexofenadine patent estate and what does that mean for new entrants?

Practical IP strength view

Because fexofenadine is mature, the patent estate is typically:

- fragmented across jurisdictions,

- weak at the formulation and packaging layer,

- overridden commercially by generic availability.

Forecast implication: entry barriers are low relative to newer drugs; competitive intensity remains high.

What generics launch risks exist for fexofenadine (Paragraph IV, FDA approvals, and litigation)?

Paragraph IV and litigation impact

In a mature molecule, the most relevant “launch risk” is less about Paragraph IV fights and more about:

- rapid generic scaling,

- price erosion post-approval,

- retail stocking behavior.

Forecast implication: litigation events may create temporary supply constraints, but the dominant forecast driver is price-driven substitution.

How does fexofenadine compare with cetirizine, loratadine, and levocetirizine in sales economics?

Competitive comparisons that move revenue

- Sedation profile: fexofenadine is often chosen for “non-drowsy” preference; this can support retention when consumers switch between OTC options.

- Dose convenience: once-daily regimens can win repeat purchases.

- Efficacy perceptions: perceived speed and symptom control drive brand loyalty even under generic availability.

Forecast implication: if competitors face pricing disruption (e.g., shortages, supply issues, promotion cycles), fexofenadine can gain share temporarily. In stable periods, price competition compresses all players.

Sales projection scenarios for fexofenadine (global, US, and international)

Scenario framework

Use three scenarios to bracket uncertainty:

| Scenario | Net price trend | Unit trend | Key channel assumptions | Indicative revenue trajectory |

|---|---|---|---|---|

| Base | modest annual decline | low single-digit growth | OTC holds share, stable retail promotions | low single-digit global CAGR |

| Upside | slower price decline | stronger seasonal-driven demand | improved OTC mix, higher higher-strength share | mid single-digit global CAGR |

| Downside | faster price decline | flat units | heavier generic substitution and more price wars | revenue flat to low growth |

Projection horizon (example structure)

Because exact market sizing varies by source and geography, the correct way to project is to apply scenario rates to your current revenue baseline:

- Global: Base ~3% CAGR, Upside ~4% to 5%, Downside ~0% to 2%

- US: Base ~2% to 3%, Upside ~3% to 4%, Downside ~-1% to 2%

- International: Base ~3% to 5%, Upside ~5% to 7%, Downside ~1% to 3%

Forecast implication: if your planning horizon is 3-5 years, the model can be controlled largely by net price assumptions, not by demand expansion.

Key commercial risks that could change the forecast

Retail price wars

Generic entries and distributor pricing can accelerate net price erosion.

Seasonality shocks

Unusually mild or severe allergy seasons can swing quarterly demand, but long-run CAGR typically normalizes.

Competitive class switching

If cetirizine/loratadine run promotions or gain consumer perception share, fexofenadine can lose OTC shelf share.

Regulatory or labeling changes

Any changes affecting OTC status or labeling language can reshape consumer behavior, but such events are usually infrequent for established antihistamines.

Key Takeaways

- Fexofenadine is a mature, largely generic OTC-driven market with revenue growth dominated by net price and channel mix.

- Expect low-to-mid single-digit global revenue CAGR under base assumptions, with US likely toward the lower end due to entrenched generic pricing.

- Patent and exclusivity timing is generally not a primary driver for medium-term sales projections because competitive availability is already established.

- The forecast is most sensitive to annual net price decline and OTC shelf share stability versus class competitors.

FAQs

-

What drives quarterly fexofenadine sales the most?

Seasonal allergy severity and retail promotion cycles tend to dominate quarter-to-quarter movement, with generic pricing setting the underlying net price trend. -

Do fexofenadine 180 mg and 60 mg strengths sell differently?

Once-daily convenience typically supports retention for higher-strength regimens, but exact revenue contribution depends on local pack preferences and competitor pricing. -

How much market share does fexofenadine lose to cetirizine or loratadine?

Share shifts are usually gradual and retail-driven; sustained loss requires persistent competitor price/promo advantages or perceived efficacy changes. -

Is fexofenadine growth in emerging markets higher than in the US?

Often yes, because generic entry timing and OTC penetration can lag the US, allowing modest unit and mix growth even with price pressure. -

What is the biggest reason fexofenadine revenue can diverge from units?

Net price erosion from additional generic supply can reduce revenue even when unit demand grows.

References (APA)

- FDA. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration.

- IQVIA Institute. (n.d.). Industry and market insights on pharmaceutical trends (report series). IQVIA.

- National Center for Health Statistics. (n.d.). Mortality and health-related datasets (for demographic baselines influencing OTC demand). CDC.

- World Allergy Organization. (n.d.). Global allergy prevalence resources (context for demand drivers). World Allergy Organization.

More… ↓