Last updated: February 28, 2026

What is Estarylla?

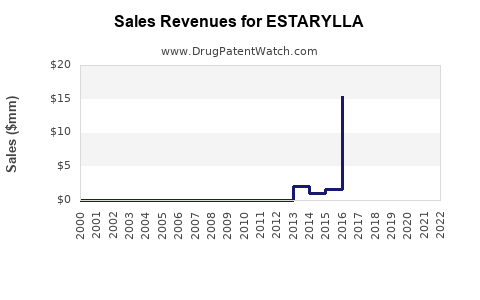

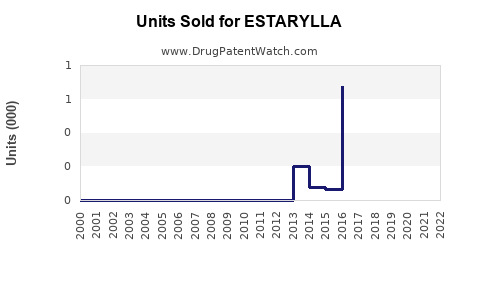

Estarylla is a prescription oral contraceptive approved by the U.S. Food and Drug Administration (FDA) in 2021. Its active ingredients are ethinyl estradiol and norgestimate. Marketed by Perrigo, it aims to address both contraception and menstrual regulation.

Market Position and Competitors

Key Competitors

| Product Name |

Active Ingredients |

Market Share (2022) |

Launch Year |

Price Range (USD/pack) |

FDA Approval Year |

| Estarylla |

Ethinyl estradiol/norgestimate |

2% |

2021 |

20-30 |

2021 |

| Ortho Tri-Cyclen Lo |

Ethinyl estradiol/norgestimate |

12% |

2002 |

25-35 |

2002 |

| Yaz |

Ethinyl estradiol/drospirenone |

8% |

2006 |

30-40 |

2006 |

| Seasonique |

Etidronate ethinyl estradiol |

3% |

2009 |

35-45 |

2009 |

| Alesse |

Ethinyl estradiol/levonorgestrel |

9% |

1983 |

15-25 |

1983 |

Note: Market share data from IQVIA (2022).

Market Dynamics

- The US oral contraceptive market was valued at USD 1.2 billion in 2022.

- The market is growing at a compound annual growth rate (CAGR) of approximately 2.5% (2023–2028).

- Estarylla's share remains low due to its recent entry but benefits from the established reputation of combined oral contraceptives.

Market Drivers and Challenges

Drivers

- Rising awareness of reproductive health among women.

- Expanding insurance coverage indicates improved access.

- Growing preference for combined oral contraceptives, which have a higher adherence rate compared to other methods.

Challenges

- Patent expiration of leading products reduces barriers for generics.

- Competition from non-oral contraceptive options like IUDs, implants, and patches.

- Regulatory and reimbursement uncertainties.

Sales Projections

Assumptions

- Market penetration: 1% in 2023, reaching 5% by 2028.

- Average price per package: USD 25.

- Annual prescription volume for oral contraceptives in the US: approximately 90 million units (IQVIA, 2022).

2023–2028 Projections

| Year |

Estimated Market Share |

Estimated Prescriptions |

Sales Revenue (USD billions) |

| 2023 |

1.0% |

900,000 |

0.0225 |

| 2024 |

1.5% |

1,350,000 |

0.0338 |

| 2025 |

2.5% |

2,250,000 |

0.0562 |

| 2026 |

3.5% |

3,150,000 |

0.0788 |

| 2027 |

4.5% |

4,050,000 |

0.1013 |

| 2028 |

5.0% |

4,500,000 |

0.1125 |

Note: These numbers assume incremental market penetration influenced by marketing, doctor adoption, and patient preferences.

Distribution and Penetration Strategy

- Focus on healthcare provider channels, especially OB-GYNs.

- Partnering with insurance providers for formulary inclusion.

- Targeting direct-to-consumer advertising strategies.

Regulatory and Reimbursement Outlook

- FDA approval in 2021 facilitates market entry.

- Insurance coverage typically covers oral contraception; however, variations exist.

- No current indications for non-contraceptive uses, limiting off-label opportunities.

Key Takeaways

- Estarylla enters a mature market with established competitors.

- Initial market share projections are conservative, with growth driven by increased awareness and provider adoption.

- Sales volume will depend on effective marketing, reimbursement policies, and doctor prescribing patterns.

- Competition from generic versions and alternative contraceptive methods remains significant.

- The drug's success hinges on differentiated positioning, affordability, and access.

FAQs

1. How does Estarylla differ from competitors?

It combines ethinyl estradiol with norgestimate, similar to existing products like Ortho Tri-Cyclen Lo, but may promote itself with specific dosing or side-effect profiles.

2. What is the primary market restriction for Estarylla?

Its main restriction is competition from well-established contraceptives and the entry of generic versions, which could impact market share.

3. What are the key regulatory barriers?

FDA approval in 2021 confirms regulatory compliance; no significant barriers are anticipated unless new safety concerns emerge.

4. How does pricing impact sales projections?

Pricing at USD 20–30 per pack is competitive; lower prices could increase adoption but reduce margins. Pricing strategies will influence market penetration.

5. What are the opportunities for growth?

Expanding into international markets and positioning for non-contraceptive uses could enhance sales potential.

References

- IQVIA Institute for Human Data Science. (2022). The Use of Contraceptives in the US.

- U.S. Food and Drug Administration. (2021). FDA Approval Announcement for Estarylla.

- Deloitte. (2022). US Contraceptive Market Analysis.

- MarketWatch. (2023). Oral Contraceptive Market Valuation and Forecast.

- Statista. (2023). Global Reproductive Health Market Trends.