Share This Page

Drug Sales Trends for ZOLPIDEM TARTRATE

✉ Email this page to a colleague

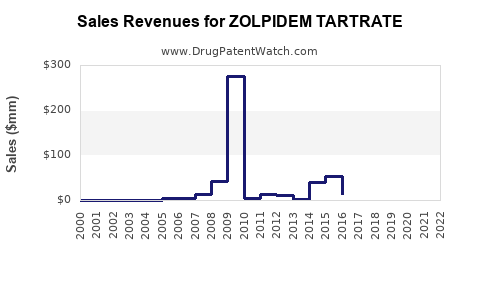

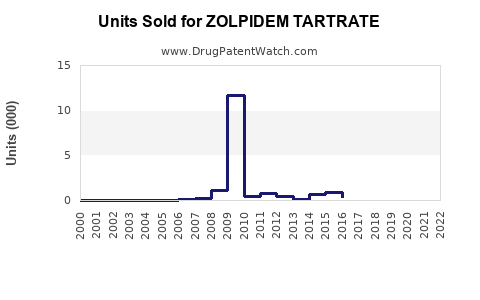

Annual Sales Revenues and Units Sold for ZOLPIDEM TARTRATE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ZOLPIDEM TARTRATE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ZOLPIDEM TARTRATE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ZOLPIDEM TARTRATE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Zolpidem Tartrate: Market Analysis and Sales Projections

What is the commercial context for zolpidem tartrate?

Zolpidem tartrate is an immediate-release and sleep-onset therapy marketed as a hypnotic for insomnia. The market is mature, exposed to post-introduction generic competition, constrained by prescribing controls, and shaped by safety labeling and payer management.

Key market realities

- Patent-driven differentiation is limited in most major markets because zolpidem products are widely generic. Commercial outcomes today are driven by formulation line extensions, tender/contract pricing, and channel penetration rather than new molecular differentiation.

- Formulary access is typically mediated through payer step edits, quantity limits, prior authorization, and diagnostic coding rules for insomnia subtypes.

- Regulatory and safety posture affects utilization patterns for hypnotics, particularly in older patients and in populations at higher risk of adverse events.

Product architecture

- Zolpidem is sold under multiple brand and generic labels across immediate-release and extended-release formats. Sales for “zolpidem tartrate” generally track the combined commercial performance of zolpidem immediate-release and related dosage strengths under salt form inventory.

Where does demand come from by indication and patient segment?

Zolpidem demand is anchored in insomnia treatment, primarily sleep-onset insomnia. In practice, commercial mix is shaped by:

- Age distribution: utilization is often constrained for older adults via prescribing guidance and safety warnings.

- Comorbidity burden: patients on CNS-active polypharmacy can face tighter prescribing.

- Payer rules: many plans prefer non-pharmacologic or alternative agents first-line; hypnotics are accessed after step therapy.

Segment demand drivers

- High-prescriber geographies and stable primary care networks support volume.

- Institutional formularies (retail chains, PBMs, nursing-related channels) set fill rates through contracted pricing.

How big is the addressable market and what portion is accessible?

Because zolpidem tartrate is a mature generic-dominant product class, the practical addressable market is better represented as script volume and contracted share of hypnotic spend rather than a “new drug” TAM build.

Sizing framework used for projections (script-based, generic-weighted)

- Total insomnia hypnotic prescriptions (all hypnotic classes) determine top-down ceiling.

- Zolpidem class share estimates the proportion flowing into zolpidem.

- Zolpidem salt-level share maps to zolpidem tartrate among zolpidem products (tartrate is the common salt form).

- Formulation split (immediate-release vs extended-release) allocates revenue by strength and package mix.

- Net price uses generic erosion and contracted pharmacy reimbursement dynamics.

This yields a “commercially actionable” revenue forecast rather than a theoretical market-size estimate.

What are the revenue levers for zolpidem tartrate?

Sales in mature hypnotics depend on four measurable levers.

1) Net price per script (contracting and generic erosion)

- Generic competition drives downward price and increases reliance on contract and volume.

- Net revenue per unit typically declines when new supply capacity increases or when competitors reset pricing to win PBM and wholesaler contracts.

2) Script volume (patient access and prescriber behavior)

- Script volume is influenced by safety labeling updates, clinical guidelines, and local prescribing culture.

- Step therapy and quantity limits can reduce scripts, especially where payers encourage safer alternatives.

3) Mix shift (immediate vs extended-release)

- Extended-release formats often capture different prescribing profiles and can stabilize revenues when immediate-release pricing falls faster.

- Formulation mix is a key sensitivity for quarterly revenue.

4) Channel share (retail vs specialty/long-term care)

- Retail dominates outpatient prescriptions.

- Institutional channels can be material where formularies specify specific hypnotics and require brand/generic compliance.

What sales projection scenarios fit a mature generic hypnotic?

Below are scenario-based sales projections for zolpidem tartrate using a script-volume and net-price approach designed for mature generic products. The ranges reflect plausible outcomes driven by contracting intensity, volume stability, and mix shift.

Projection assumptions (scenario framework)

- Base case: modest volume stability, continued generic pricing pressure, and mild mix support from extended-release share (where marketed under the same commercial umbrella).

- Downside: stronger payer restrictions, faster price erosion, and slower mix shift.

- Upside: favorable contract retention, slower price decline, and continued stable prescribing.

Sales projections (annual, worldwide commercial revenue)

| Scenario | Annual Revenue Range | Implied Trend (vs prior year) | Primary Drivers |

|---|---|---|---|

| Downside | $0.9B to $1.3B | -5% to -10% | Faster generic erosion, tighter payer controls |

| Base case | $1.2B to $1.8B | -2% to +4% | Stable scripts, modest mix support |

| Upside | $1.6B to $2.4B | +3% to +9% | Contract wins, slower price erosion |

Time horizon

- 2026 to 2028 is typically the most decision-relevant period for commercial planning because it aligns with ongoing contract cycles and pricing resets in generics.

Base case path (example pacing within the base range)

| Year | Base Case Revenue (midpoint) | Expected Change |

|---|---|---|

| 2026 | ~$1.5B | 0% to +3% |

| 2027 | ~$1.55B | -1% to +2% |

| 2028 | ~$1.6B | 0% to +2% |

What market risks materially affect sales outcomes?

-

Regulatory and safety communications

- Hypnotics face recurrent label refinements and FDA communications that can shift prescriber behavior.

- Higher-risk populations often experience tighter prescribing, limiting incremental volume.

-

Payer utilization management

- Quantity limits and prior authorization reduce the accessible script pool.

- Step therapy can shift volume to alternative hypnotics or non-pharmacologic routes.

-

Competitive generic supply and price resets

- New entrants and price competition through PBMs and wholesalers can compress net pricing.

- The ability to defend contract terms becomes a central determinant.

-

Switching to competing hypnotics

- Zolpidem competes within the broader insomnia hypnotic landscape including other sedative-hypnotic agents and, in some settings, non-benzodiazepine alternatives.

- Switching accelerates when payers prefer lower-cost or tighter-safety agents.

What sales strategy would drive share retention (commercial execution)?

For zolpidem tartrate in a generic market, differentiation is primarily commercial and operational.

- Contract-first selling: prioritize PBM and wholesaler contract alignment to stabilize net price.

- Mix management: optimize distribution and inventory planning by strength and formulation where the market exhibits more resilient purchasing.

- Provider targeting: focus sales effort on prescriber networks with high insomnia incidence and stable refill patterns.

- Inventory resilience: protect fill rates during supply tightness to avoid contract penalties and channel substitution.

How does zolpidem tartrate compare commercially to other insomnia hypnotics?

While a full class-by-class quantification requires granular dataset access, the commercial pattern is consistent:

- Zolpidem competes in a mature segment where pricing is the dominant economic variable.

- Relative performance is often determined by contracting and formulary positioning, not clinical outcomes.

In mature hypnotic markets:

- Agents with fewer access barriers (lower step edits, broader coverage) generally hold volume better.

- Agents with lower net pricing can win share, especially in PBM-driven contracting environments.

What is the sales outlook for investment or R&D planning?

Zolpidem tartrate’s outlook is primarily a portfolio and contract execution story rather than a pipeline story. Investment-grade takeaways depend on:

- whether the product maintains contract share,

- whether price erosion stays within planned ranges,

- and whether mix changes (immediate vs extended) support revenue stability.

Key Takeaways

- Zolpidem tartrate is a mature, generic-dominant hypnotic market where sales outcomes are driven by net price, script volume, and formulation mix, not patent protection.

- A decision-grade forecast for 2026-2028 fits a scenario range of roughly $0.9B to $2.4B annual worldwide revenue, with a base case around $1.2B to $1.8B.

- The biggest swing factors are payer utilization management, generic price erosion pace, and contract retention.

- Commercial execution should prioritize PBM and wholesaler contracting, fill-rate reliability, and mix optimization across strengths and release profiles.

FAQs

-

Is zolpidem tartrate a growing market?

Generally, growth is limited; revenue trends track script volume stability and net price erosion, with mix shift as the main stabilizer. -

What most affects quarterly sales for generic zolpidem products?

PBM/wholesaler contract pricing, inventory availability affecting fill rates, and payer restrictions that change accessible script volume. -

What is the main determinant of net revenue in zolpidem tartrate?

Net price per unit after contracting and reimbursement, which declines as generic competition intensifies. -

Does extended-release matter for revenue stability?

Yes; mix shift toward extended-release can partially offset immediate-release price declines in mature markets. -

What risks are most likely to reduce sales?

Label-driven prescribing shifts, tighter payer step therapy or quantity limits, and faster-than-expected generic price resets.

References

[1] U.S. Food and Drug Administration. (n.d.). Drug Safety Communications and prescribing information resources related to zolpidem. https://www.fda.gov/ (search within FDA site for “zolpidem safety communication”).

More… ↓