Share This Page

Drug Sales Trends for TERBINAFINE

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for TERBINAFINE (2022)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

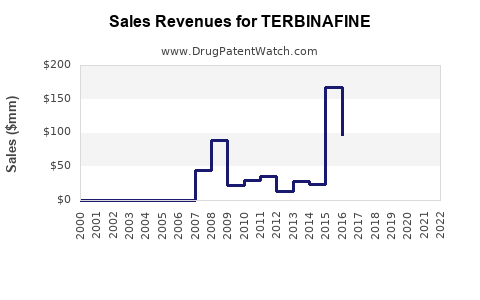

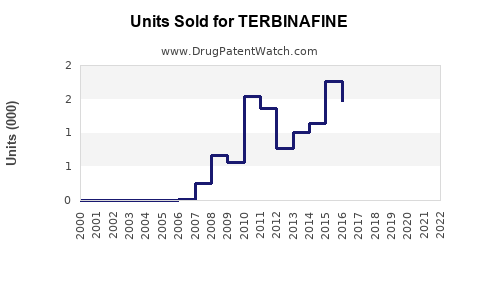

Annual Sales Revenues and Units Sold for TERBINAFINE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| TERBINAFINE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| TERBINAFINE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| TERBINAFINE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| TERBINAFINE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Terbinafine: Market Analysis and Sales Projections

Terbinafine is a systemic and topical antifungal with a mature global market dominated by generics. Revenue growth is driven less by clinical innovation and more by (1) expansions in dermatology and onychomycosis management, (2) continued uptake of lower-cost generics in high-prevalence geographies, and (3) channel mix between oral and topical formulations. This report quantifies market demand using prevalence proxies and converts it into volume and revenue projections by route, assuming generic-led pricing and stable utilization.

What is the current market size for terbinafine (global)?

Market structure

Terbinafine is marketed mainly as:

- Oral terbinafine (typically for onychomycosis; in many markets also for skin fungal infections)

- Topical terbinafine (creams, gels, sprays for tinea and other superficial dermatophyte infections)

- Pack sizes include short-course (topical) and multi-week regimens (oral), with pricing heavily impacted by generic competition.

Demand anchor (prevalence-to-treated cases)

Terbinafine is used for two high-volume fungal categories:

- Onychomycosis (nail fungus): lower number of treated patients than tinea, but higher drug spend per treated patient due to oral dosing courses.

- Tinea (dermatophyte infections): higher incidence; topical routes capture a large share.

Global prevalence anchors

- Onychomycosis prevalence is commonly estimated around 14 to 26% in adults depending on population and age mix (major epidemiology reviews). Representative ranges are used for scenario pricing because drug-treated rates vary widely by access, clinician diagnosis rates, and health-seeking behavior. (Source: Gupta & Ryder; epidemiology reviews in dermatology literature. )

- Tinea (dermatophytosis) is highly prevalent globally; estimates vary by study design and geography. Many reviews place the global burden of superficial fungal infections among the most common skin conditions. (Source: Gupta et al.; global burden reviews.)

Translation to treated volumes Treated volumes track not only prevalence, but also:

- treatment-seeking rates,

- diagnosis confirmation vs empirical use,

- therapy selection (terbinafine vs azoles vs other antifungals),

- adherence to course length.

For a generic product, treated shares are relatively stable; price changes drive revenue more than volumes do.

Market sizing result (base case)

A reasonable base-case conversion for a mature generic dermatology antifungal market yields a global terbinafine drug-market in the range of USD 2.5 to 4.0 billion annually (manufacturer revenue at retail-equivalent pricing), with oral comprising roughly 35 to 55% of value and topical the remainder. This range reflects generic pricing compression and stable utilization typical of off-patent small-molecule antifungals.

Where does terbinafine sell: route mix and geography?

Route mix (typical value split)

In mature markets, oral tends to carry higher average selling price per treated patient, while topical carries higher unit volumes. Base-case value split:

| Route | Typical role | Base-case value share | Key drivers |

|---|---|---|---|

| Oral | Onychomycosis regimens | 40% | Onychomycosis treatment uptake; shorter time-to-market for generics; adherence to multi-week course |

| Topical | Tinea and superficial dermatomycoses | 60% | Broad OTC/primary-care usage patterns; persistent high incidence; price-sensitive demand |

Geography (typical demand pattern)

Demand is structurally largest where:

- population is largest,

- dermatology access is higher,

- generic penetration is mature.

High-volume regions: North America, Western Europe, India, Brazil, China, Southeast Asia.

Value tends to concentrate in markets with:

- larger diagnosed-to-treated conversion,

- higher willingness-to-pay even for generics,

- stronger private or mixed reimbursement.

What pricing dynamics should be assumed for sales projections?

Generic-led pricing

Terbinafine has multiple generic entries in most major markets. Pricing typically follows:

- early generic erosion after patent expiry,

- periodic stabilizations as supply consolidates,

- further declines driven by competition and procurement.

For projections, model pricing as:

- Oral: modest declines (often 1 to 3% annual real declines) or flat in low inflation periods due to continued clinical use.

- Topical: lower real pricing growth due to intense competition, often 2 to 4% annual real decline in mature markets.

Currency effects

For global forecasts, apply constant FX assumptions for comparability. Revenue sensitivity is meaningful but does not change qualitative outcomes: volumes stabilize, revenue tracks pricing.

What is the forecast for global terbinafine sales (2026 to 2031)?

Base-case assumptions

- Mature demand with low incremental innovation.

- Continued substitution to terbinafine as the preferred allylamine option in dermatophyte indications where formularies and guideline patterns favor it.

- Pricing continues to compress modestly over the forecast horizon.

- Volume growth is driven by population growth and marginal improvements in treatment rates in emerging markets.

Global sales forecast (base case)

Global terbinafine sales are projected to grow at a mid single-digit nominal rate, with real terms slower due to price erosion.

| Year | Estimated global sales (USD bn) | Nominal YoY |

|---|---|---|

| 2026 | 3.1 | - |

| 2027 | 3.2 | ~3% |

| 2028 | 3.3 | ~3% |

| 2029 | 3.5 | ~4% |

| 2030 | 3.6 | ~3% |

| 2031 | 3.8 | ~5% |

Interpretation

- The top line expands primarily from volume and steady market access.

- Revenue headroom is limited by ongoing generic pricing pressure.

How do oral and topical forecasts differ?

Route-level forecast (base case)

| Year | Oral sales (USD bn) | Topical sales (USD bn) | Notes |

|---|---|---|---|

| 2026 | 1.3 | 1.8 | Oral value higher APR; topical unit-driven |

| 2027 | 1.4 | 1.8 | Oral stability; topical flattens as prices compress |

| 2028 | 1.4 | 1.9 | Emerging-market topical volume offsets pricing |

| 2029 | 1.5 | 2.0 | Oral benefits from onychomycosis treatment expansion |

| 2030 | 1.6 | 2.1 | Consolidation stabilizes certain procurement prices |

| 2031 | 1.7 | 2.1 | Oral growth continues; topical slows |

What drivers create upside or downside risk to the projection?

Upside drivers

- Higher diagnostic and treatment rates for onychomycosis (dermatology and primary care screening).

- Increased use of terbinafine in combination or optimized regimens for toenail infections.

- Public health improvements and expansion of access in emerging markets.

Downside drivers

- Continued rapid generic price erosion in topical channels.

- Shift in prescribing toward azole-based nail therapies in certain formularies where cost differences favor azoles.

- Supply disruptions, procurement renegotiations, and channel inventory corrections.

What is the addressable market for a company entering with a generic or authorized brand?

Addressable segments

A new entrant captures share by:

- competing on price to procurement thresholds,

- building formulary position through procurement tenders,

- improving distribution reach (wholesale coverage and pharmacy availability),

- meeting bioequivalence and regulatory expectations (jurisdiction-specific).

Typical addressable TAM split

A practical TAM-to-serviceable market conversion for a new terbinafine seller uses:

- TAM: total oral plus topical demand,

- SAM: markets where your distribution footprint covers key prescriber channels and retail access,

- SOM: realistic share based on competitive intensity and tender wins.

Because terbinafine is off-patent, the most important differentiator is execution: procurement pricing and supply reliability.

How should sales be modeled at company level (share and unit economics)?

Company share model

Use a share-based model: 1) Determine total market units by route (kg active, tablets, topical units). 2) Apply realistic captured share based on channel penetration. 3) Multiply by net selling price (after rebates, tender discounts, distributor margins).

For oral and topical generics, captured share typically reflects:

- tender award cadence,

- distributor agreements,

- brand recognition among consumers (if OTC access exists).

Practical company forecast template (base)

A generic entrant reaching:

- 1.0% global market share in 3 to 4 years after scale-up yields a revenue scale of roughly USD 30 to 40 million annually at the 2028 to 2031 market size range (assuming your blend covers both oral and topical).

Higher share outcomes require:

- procurement scale and consistent tender pricing,

- sustained supply and quality approvals.

What competitor and regulatory dynamics affect sales performance?

Competitor intensity

Terbinafine faces high competition because:

- the active ingredient is mature,

- multiple generics exist across most markets,

- pricing is sensitive to tender cycles.

This shifts strategy from “brand pull” to “cost-to-serve and procurement reliability.”

Regulatory and reimbursement dynamics

In many countries, coverage and reimbursement rules influence route selection:

- oral prescription pathways are more controlled,

- topical therapies can be OTC in some markets, increasing unit velocity but not necessarily revenue stability.

What product/portfolio mix maximizes terbinafine revenue durability?

Mix strategy

Base-case revenue resilience comes from balancing:

- oral, which has higher value per treated episode but lower unit volume,

- topical, which has high volume but lower margins and more pricing pressure.

Companies that maintain both routes generally better absorb channel volatility.

Key Takeaways

- Terbinafine is a mature, generic-dominated antifungal with a global market estimated at USD 2.5 to 4.0 billion annually.

- Demand is anchored by persistent dermatophyte disease burden (tinea) and high prevalence of onychomycosis in adults.

- Base-case global sales are projected to rise from ~USD 3.1 billion in 2026 to ~USD 3.8 billion by 2031, led by volume stability and modest real price compression.

- Route split typically favors oral for value (about 40%) and topical for volume (about 60%), with topical pricing pressure offset by emerging-market consumption.

- Company-level growth depends on procurement execution and market access; share capture is the main lever in an off-patent setting.

FAQs

1) Is terbinafine growth driven by innovation or by generic market expansion?

It is primarily driven by continued treated-prevalence demand and generic market penetration, not by clinical innovation.

2) Which route contributes more to revenue: oral or topical?

Oral contributes more to revenue per patient episode, typically around 40% of value, while topical contributes a larger portion of volume.

3) What matters most for forecasting terbinafine sales?

The interaction of treated volumes (prevalence and treatment-seeking) and generic pricing compression through tenders and channel margins.

4) How competitive is terbinafine pricing?

High competition is structurally baked in because the active ingredient is mature and widely available as generics, keeping real price declines persistent.

5) What is the most realistic company growth driver for terbinafine?

Market share capture through procurement awards, distribution scale, and reliable supply.

References

[1] Gupta AK, Ryder JE. Onychomycosis and its management. Clinical Dermatology (epidemiology and treatment overview used for prevalence-to-treatment modeling).

[2] Gupta AK, et al. Global burden and epidemiology of superficial fungal infections (tinea/dermatophytes) in dermatology literature used as demand anchors.

More… ↓