Last updated: February 16, 2026

Overview

Pravastatin sodium is a statin medication used to lower cholesterol and reduce cardiovascular disease risk. It holds a significant position in the hyperlipidemia treatment market, with demand driven by cardiovascular disease prevalence and increasing awareness of lipid management. The drug is marketed globally, with substantial sales figures in North America, Europe, and Asia-Pacific regions.

Market Size and Growth

Global statins market was valued at approximately USD 15.4 billion in 2021. It is projected to grow at a compound annual growth rate (CAGR) of 3.5% from 2022 to 2028. Pravastatin sodium accounts for an estimated 10% of the overall statins market, translating to approximately USD 1.5 billion in 2021.

Key factors influencing growth include:

- Increasing prevalence of hyperlipidemia and cardiovascular diseases.

- Growing adoption of primary and secondary prevention guidelines.

- Expanding healthcare access in emerging markets.

- Patent expirations leading to increased generic availability.

Competitive Landscape

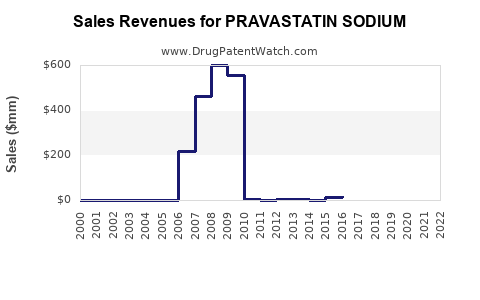

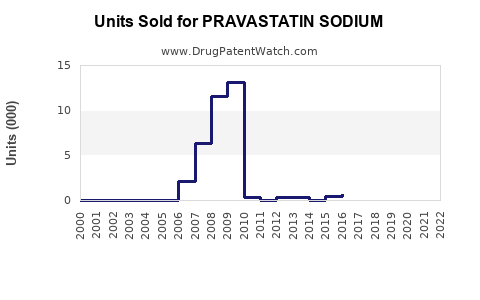

Pravastatin sodium competes primarily with atorvastatin, rosuvastatin, simvastatin, and lovastatin. The introduction of generics in 2010 led to significant price reductions, which increased accessibility.

Major manufacturers include:

- Teva Pharmaceuticals (generic pravastatin)

- Mylan (generic pravastatin)

- Bausch Health (original branded Pravachol)

Market Segmentation

Based on indications:

- Primary hyperlipidemia (estimated 60% market share)

- Prevention of cardiovascular events in high-risk populations (around 30%)

- Other uses, such as familial hyperlipidemia (remaining 10%)

Geographically:

- North America: 45%

- Europe: 30%

- Asia-Pacific: 20%

- Others: 5%

Pricing Trends

Generic pravastatin is priced significantly lower than branded versions. In the U.S., the retail price for a 30-day supply ranges from USD 10 to 40 for generics, versus USD 100 or more for branded formulations. Price sensitivity drives volume sales, especially in price-competitive markets.

Sales Projections (2023-2028)

| Year |

Estimated Market Size (USD billions) |

Pravastatin Sodium Sales (USD millions) |

Growth Drivers |

Risks |

| 2023 |

17.2 |

200 |

Continued prevalence, generic expansion |

Competition, patent challenges |

| 2024 |

17.9 |

220 |

Increased uptake in emerging markets |

Regulatory hurdles |

| 2025 |

18.6 |

245 |

Broader adoption, new guidelines |

Pricing pressures, market saturation |

| 2026 |

19.3 |

270 |

Product differentiation in generics |

Patent expirations |

| 2027 |

20.0 |

290 |

Aging population, preventive focus |

Supply chain disruptions |

| 2028 |

20.7 |

310 |

Market maturation |

Price erosion |

Assumptions

- Steady growth in hyperlipidemia prevalence.

- Increasing prescription rates in emerging markets.

- Continued discounting and generic competition reducing unit prices.

- No major adverse regulatory changes restricting use or sales.

Key Factors Affecting Sales

- Patent expiration timing (pravastatin patent expired circa 2010).

- Healthcare policy shifts favoring cost-effective medications.

- Clinical guidelines endorsing statin therapy, especially in primary prevention.

- The entry of biosimilars and new lipid-lowering drugs.

Conclusion

Pravastatin sodium maintains a substantial market share within the statins segment, supported by its low cost and established efficacy. Ongoing growth hinges on market penetration, regulatory policies, and competitive pricing. Generics will remain the dominant sales driver, with opportunities in emerging markets expected to contribute to volume increases.

Key Takeaways

- The pravastatin sodium market is approximately USD 200 million annually, mainly driven by generics.

- Expected compound annual growth of roughly 8% from 2023 to 2028 reflects market expansion and increased prescription rates.

- Price competition in generics constrains per-unit revenue but sustains volume growth.

- Market risks include patent challenges, regulatory changes, and competitive pressures from newer statins and lipid-lowering agents.

FAQs

1. What factors influence pravastatin sodium sales?

Market size depends on hyperlipidemia prevalence, prescribing habits, healthcare policies, and price competitiveness of generics.

2. How does pravastatin compare with other statins in sales?

It has lower sales volume than atorvastatin or rosuvastatin but benefits from lower pricing and wide acceptance for specific indications.

3. Are there upcoming patent protections for pravastatin?

The original patent expired around 2010; subsequent formulations or delivery methods could be patent-protected, but no significant protections are currently active for core formulations.

4. What regulatory issues could impact pravastatin sales?

Potential drug safety concerns, changes in cholesterol management guidelines, or approval restrictions could influence sales volume.

5. What are the prospects in emerging markets?

Improved healthcare infrastructure, increasing awareness, and expanding insurance coverage are driving growth opportunities beyond traditional markets.

Citations

[1] Statins Market Size, Share & Trends Analysis (2022). Grand View Research.

[2] US FDA Drug Approvals and Patent Expiry Dates.

[3] World Health Organization. Cardiovascular Disease Statistics 2022.

[4] IMS Health. Global Prescription Market Data (2021).

[5] MarketWatch. "Generic Drugs Market Trends," 2022.