Share This Page

Drug Sales Trends for ORACEA

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for ORACEA (2022)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

Annual Sales Revenues and Units Sold for ORACEA

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| ORACEA | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| ORACEA | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| ORACEA | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| ORACEA | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| ORACEA | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

ORACEA (DOXYCYCLINE HYCLATE) PATENT EXPIRATION AND MARKET IMPACT ANALYSIS

This report details the patent landscape and projected market performance for ORACEA (doxycycline hyclate), focusing on its upcoming patent expirations and the subsequent competitive and commercial implications. ORACEA, indicated for the treatment of inflammatory lesions and papules associated with moderate to severe rosacea, faces patent cliffs that will enable generic competition, necessitating strategic planning for stakeholders.

What is the Current Patent Status of ORACEA?

The primary patent protecting ORACEA is U.S. Patent No. 6,472,012, titled "Method of treating inflammatory lesions and papules of rosacea." This patent was granted on October 29, 2002. The listed expiration date for this patent was October 29, 2022.

While the '012 patent is the core compound patent, other related patents and exclusivities may have applied. However, key discussions and legal challenges have historically centered around this patent and its expiration. For instance, in litigation concerning ORACEA, the validity and enforceability of the '012 patent have been central issues [1].

The U.S. Food and Drug Administration (FDA) Orange Book lists ORACEA (doxycycline hyclate) 40 mg delayed-release capsules. The latest entry for this product and its associated patents as of recent reviews typically indicates that the primary patent protection has concluded or is nearing conclusion [2].

When Did Key Patents for ORACEA Expire or Become Vulnerable?

The most significant patent expiration for ORACEA, U.S. Patent No. 6,472,012, occurred on October 29, 2022. This date marked the termination of the primary patent term that protected the method of treating rosacea with a specific delayed-release formulation of doxycycline.

Prior to this expiration, the patent had been subject to legal challenges. Generic manufacturers often seek to invalidate existing patents or find ways to design around them. For example, in a 2014 patent infringement lawsuit filed by Galderma Laboratories L.P. (the marketer of ORACEA) against Teva Pharmaceuticals USA Inc., the validity of the '012 patent was contested [3]. Teva argued that the patent was invalid over prior art. While Galderma initially secured an injunction, subsequent legal proceedings, including appeals, scrutinized the patent's claims. These legal battles can sometimes lead to earlier invalidation or shorter remaining effective patent life, though in this instance, the patent appears to have run its original course.

Additional patents related to the formulation or manufacturing processes could exist, but the expiration of the '012 patent is the critical inflection point for market entry of generic versions of the specific ORACEA product. The expiry of this patent allows for the introduction of AB-rated generic equivalents without infringing on the core method-of-treatment patent.

What is the Market Size and Sales History of ORACEA?

ORACEA, marketed by Galderma Laboratories L.P. (and previously by Valeant Pharmaceuticals International Inc. after its acquisition of Medicis, which originally developed the drug), has held a significant position in the rosacea treatment market.

Sales Performance:

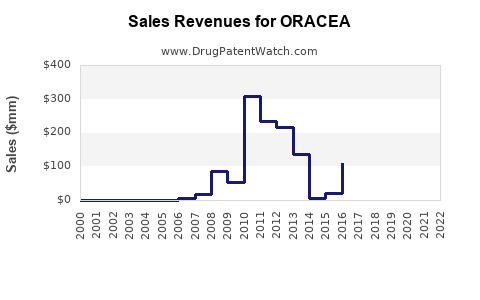

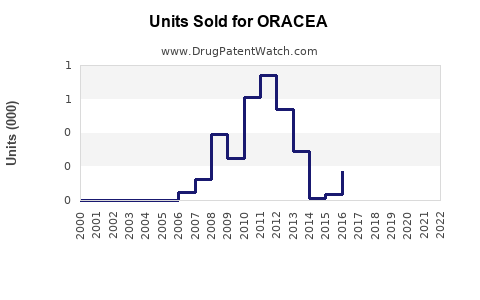

- 2018: Valeant Pharmaceuticals reported net sales of ORACEA were approximately $299 million globally [4].

- 2019: Galderma, having been spun off from Nestlé and re-established as an independent entity focused on dermatology, continued to market ORACEA. Specific sales figures for ORACEA in 2019 are often aggregated within broader product portfolios. However, given its established position, it remained a key revenue driver in the topical and oral acne and rosacea segments.

- 2020-2021: Sales for branded ORACEA likely experienced a gradual decline as market anticipation of generic entry grew. Precise figures for this period are challenging to isolate without access to Galderma's internal financial reporting.

- 2022 onwards: With the expiration of the primary patent in October 2022, branded ORACEA sales would be expected to fall sharply due to generic competition.

Market Size Estimation:

The global market for rosacea treatments is substantial and growing, driven by increasing prevalence and awareness.

- Prevalence: Rosacea affects an estimated 16 million people in the United States and more than 415 million worldwide [5].

- Market Value: The global rosacea treatment market was valued at approximately USD 2.5 billion in 2021 and is projected to grow to USD 3.8 billion by 2030, with a compound annual growth rate (CAGR) of around 4.5% [5].

ORACEA, as a well-established oral therapy targeting inflammatory lesions, historically captured a significant share of this market. Its annual sales of around $300 million in the late 2010s indicate its substantial contribution to the overall rosacea therapeutic landscape. This segment of the market is characterized by a need for effective, well-tolerated oral agents, a niche ORACEA filled.

Who are the Potential Generic Competitors for ORACEA?

The expiration of U.S. Patent No. 6,472,012 on October 29, 2022, has opened the door for generic manufacturers to launch their versions of doxycycline hyclate 40 mg delayed-release capsules. Several pharmaceutical companies have historically been involved in the generic doxycycline market and are positioned to enter the ORACEA generic space.

Key players likely to be among the first to launch generic ORACEA include:

- Teva Pharmaceuticals USA Inc.: Teva has a significant presence in the generic doxycycline market and was previously involved in legal challenges concerning ORACEA patents, indicating a strategic interest.

- Apotex Inc.: As a large generic pharmaceutical company, Apotex is a probable entrant into this market.

- Dr. Reddy's Laboratories Ltd.: Known for its broad portfolio of generic drugs, including antibiotics, Dr. Reddy's is a potential competitor.

- Sun Pharmaceutical Industries Ltd.: Sun Pharma is another global pharmaceutical powerhouse with extensive generic product lines.

- Viatris Inc. (formerly Mylan N.V.): Viatris has a substantial footprint in the generic prescription drug market.

- Lannett Company, Inc.: Lannett also has a portfolio of generic oral solid dosage forms.

These companies possess the manufacturing capabilities, regulatory expertise, and distribution networks necessary to introduce generic alternatives. The speed of market entry for these competitors will depend on their Abbreviated New Drug Application (ANDA) approvals from the FDA and their strategic decisions regarding launch timing. The FDA's approval process for generics is designed to ensure bioequivalence to the branded product.

What are the Projected Sales Impacts of Generic Entry?

The introduction of generic competitors for ORACEA is expected to lead to a significant and rapid decline in the sales of the branded product. This phenomenon, known as the "patent cliff," is a predictable outcome in the pharmaceutical market.

Projected Sales Trajectory:

- Immediate Post-Expiration (Late 2022 - 2023): Upon the expiry of the primary patent and the FDA approval of one or more generic ANDAs, branded ORACEA sales will likely decrease by 50% to 70% within the first year of generic competition. This is due to direct price competition from generics, which are typically priced at a significant discount (often 30-50% lower than the branded drug).

- Mid-Term Impact (2024 - 2025): As more generic manufacturers enter the market, price erosion will accelerate. The number of competitors will influence the rate of decline. With potentially 3-5 major generic players, branded sales could drop by an additional 20% to 30% in this period. The total market share for branded ORACEA could be reduced to 10% to 20% of its pre-generic peak.

- Long-Term Impact (2026 onwards): Branded ORACEA sales will stabilize at a low level, primarily serving patients or physicians who specifically request the brand-name drug, or those with insurance plans that provide limited formulary coverage for generics. The market will be dominated by generic versions, with prices continuing to be competitive.

Factors Influencing Sales Impact:

- Number of Generic Entrants: A higher number of generic competitors leads to more aggressive price competition and a faster sales decline for the branded product.

- Pricing Strategies of Generic Manufacturers: The initial pricing and subsequent price adjustments by generic companies will directly affect market share distribution.

- Payer Formularies: Insurance companies and pharmacy benefit managers (PBMs) will strongly favor generic ORACEA on their formularies, increasing prescription volume for generics and decreasing it for the brand.

- Physician and Patient Prescribing Habits: While many physicians will switch to generics, some may continue prescribing the brand by name for a period. Patient adherence and preference can also play a role.

- Galderma's Lifecycle Management Strategies: Galderma may have strategies to mitigate the impact, such as promoting newer products or offering patient assistance programs, but these typically have limited long-term effect against substantial generic pricing pressure.

Based on historical data for similar branded drugs facing generic entry, a 60% to 80% decline in branded ORACEA sales within 18-24 months post-generic launch is a reasonable projection. The total market value for doxycycline hyclate 40 mg delayed-release capsules (including branded and generic) is expected to remain robust, driven by the prevalence of rosacea and the drug's established efficacy.

What are the Key Commercial and R&D Implications?

The patent expiration of ORACEA has significant commercial and R&D implications for both the innovator company (Galderma) and potential generic manufacturers.

For the Innovator (Galderma):

- Revenue Loss Mitigation: The primary implication is the projected sharp decline in ORACEA sales revenue. Galderma must focus on its pipeline of newer or more differentiated dermatology products and potentially explore lifecycle management strategies for ORACEA, though these are often limited once generic competition emerges.

- Portfolio Repositioning: Galderma will likely shift its commercial focus and marketing efforts towards its next-generation rosacea treatments or other high-growth dermatology areas.

- Market Dynamics Shift: The company will no longer hold a dominant position in the oral doxycycline for rosacea segment and must compete on a different basis (e.g., service, support) if it continues to market the branded product.

For Generic Manufacturers:

- Market Entry Opportunity: The expiration presents a clear opportunity to enter a mature market with a well-recognized product. Generic companies can leverage existing manufacturing capacity for doxycycline.

- Pricing and Market Share Competition: The key challenge will be achieving profitability in a highly competitive generic market characterized by aggressive pricing. Early market entry and securing favorable formulary placement with payers are critical.

- Supply Chain Management: Ensuring a robust and consistent supply chain for the active pharmaceutical ingredient (API) and finished product is paramount to capture market share.

- Regulatory Compliance: Adherence to FDA regulations for ANDA approval and manufacturing quality is non-negotiable.

R&D Implications:

- Focus on Next-Generation Therapies: For innovator companies, the patent cliff necessitates ongoing R&D investment in novel treatments for rosacea. This could include drugs with different mechanisms of action, improved efficacy, better tolerability profiles, or new delivery systems. Examples might include topical JAK inhibitors, novel antibiotic formulations, or treatments targeting inflammatory pathways beyond MMPs.

- Development of Combination Therapies: R&D may explore combining doxycycline with other active ingredients to create novel patented formulations or address more complex rosacea presentations.

- New Indications or Formulations: While less common for older molecules like doxycycline, innovative R&D could theoretically seek new indications or novel delivery formulations for doxycycline (though patentability of such claims would be challenging post-core patent expiry).

- Biosimilar/Biologic Development (Not applicable here): For small molecule drugs like ORACEA, the focus is on generic substitution, not biosimilar development which applies to biologic drugs.

The successful navigation of this post-patent period depends on strategic planning, efficient execution of market entry by generics, and continued innovation by the innovator to maintain market relevance.

Key Takeaways

- Patent Expiration: The primary patent for ORACEA (doxycycline hyclate 40 mg delayed-release capsules), U.S. Patent No. 6,472,012, expired on October 29, 2022.

- Generic Entry: This expiration has enabled the market entry of generic doxycycline hyclate 40 mg delayed-release capsules.

- Market Impact: Branded ORACEA sales are projected to decline significantly, potentially by 60% to 80% within 18-24 months post-generic launch due to price competition and formulary shifts.

- Competitive Landscape: Major generic manufacturers including Teva, Apotex, Dr. Reddy's, Sun Pharma, and Viatris are positioned to compete in this market.

- Strategic Imperatives: Innovator companies must focus on pipeline development and portfolio diversification, while generic companies must prioritize rapid market entry, competitive pricing, and supply chain efficiency.

Frequently Asked Questions

-

Will ORACEA be completely unavailable after its patent expires? No, the branded ORACEA product may continue to be available, but its market share and pricing power will be severely diminished by the introduction of lower-cost generic alternatives.

-

How quickly can generic versions of ORACEA enter the market after patent expiration? Generic entry can occur as soon as the FDA approves one or more Abbreviated New Drug Applications (ANDAs) for doxycycline hyclate 40 mg delayed-release capsules. This approval process can take several months to over a year following patent expiration.

-

What is the primary mechanism of action for ORACEA and its generic equivalents? ORACEA and generic doxycycline hyclate 40 mg delayed-release capsules function by exerting anti-inflammatory and antimicrobial effects. While the exact anti-inflammatory mechanisms in rosacea are not fully elucidated, doxycycline is believed to modulate the immune response and reduce the production of inflammatory mediators.

-

Are there any advantages to choosing branded ORACEA over a generic version? For a bioequivalent generic drug, there are typically no therapeutic advantages. Any perceived advantages would likely stem from physician preference, specific payer coverage, or established patient familiarity with the brand. Regulatory agencies like the FDA ensure generics are therapeutically equivalent to their brand-name counterparts.

-

How does the cost of generic doxycycline hyclate compare to branded ORACEA? Generic doxycycline hyclate 40 mg delayed-release capsules are expected to be significantly less expensive than branded ORACEA. Price differences of 30% to 50% are common upon initial generic launch, with further erosion occurring as more competitors enter the market.

Citations

[1] U.S. District Court for the District of New Jersey. (2014). Galderma Laboratories L.P. v. Teva Pharmaceuticals USA, Inc. Civil Action No. 13-7272 (JLL). [2] U.S. Food & Drug Administration. (n.d.). Approved Drug Products with Therapeutic Equivalence Evaluations (The Orange Book). Retrieved from https://www.accessdata.fda.gov/scripts/cder/ob/default.cfm [3] Reuters. (2014, September 29). Teva wins ruling in Galderma's Oracea patent case. Retrieved from https://www.reuters.com/article/us-teva-galderma-patent-idUSKCN0GO09K20140929 [4] Valeant Pharmaceuticals International Inc. (2019). 2018 Annual Report. [5] Global Market Insights. (2022). Rosacea Treatment Market Size, Share & Trends Analysis Report. (Note: Specific report title and publication date may vary slightly based on access).

More… ↓