Last updated: February 14, 2026

Overview

Nitrostat (nitroglycerin) is a medication used primarily for the acute treatment of angina pectoris. It is a sublingual tablet administered for rapid relief of chest pain associated with coronary artery disease. Its market remains robust due to its established role in emergency cardiovascular care and the sustained prevalence of angina.

Market Size and Key Drivers

The global sublingual nitrate market generated approximately $600 million in 2022, projected to grow at a compound annual growth rate (CAGR) of 3% through 2028. Major factors include increasing cardiovascular disease prevalence, aging populations, and awareness of nitrate treatments.

Prevalence of Angina and Cardiovascular Disease

- Worldwide, over 100 million individuals have angina.

- In the US, an estimated 20 million adults have stable angina.[1]

- The global burden of coronary artery disease (CAD) is expected to increase by 4% annually.[2]

Product Position and Competition

Nitrostat competes with other forms of nitroglycerin (sprays, topical patches), other nitrates (isosorbide dinitrate/mononitrate), and non-nitrate medications like calcium channel blockers and beta-blockers.

Major competitors include:

- Nitrolingual (spray): fast onset, but less widely distributed

- Isordil (tablets): longer-acting, targeting chronic management

- Generic nitroglycerin formulations

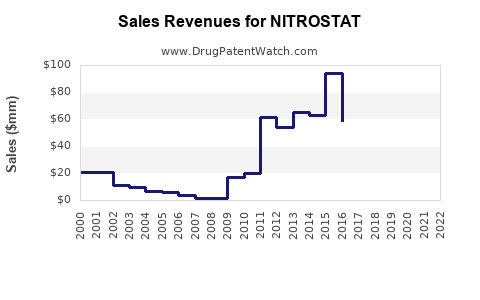

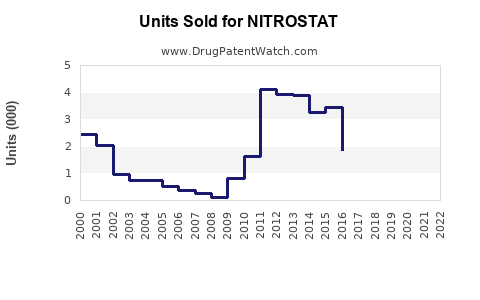

Sales Trends

In the US, Nitrostat's annual sales are estimated at approximately $70 million (2022), with low single-digit growth. The sales are influenced by:

- Prescribing habits

- Patients' preference for spray versus tablet

- Insurance formularies and reimbursement policies

Market Challenges

- Short shelf life and stability issues

- Strict storage requirements

- Availability of generics reducing pricing

Regulatory Environment

- Nitrostat received FDA approval in 1990

- It remains on the FDA's shortage list periodically due to manufacturing issues

- No current significant regulatory reforms impacting sales

Projections

Assuming steady market growth, sales are expected to increase by about 3% annually within the next five years, reaching approximately $90 million by 2028. Adoption of generic versions and emerging formulations could accelerate or slow growth.

Regional Analysis

- North America: Largest market, driven by high awareness, chronic disease management, and emergency medicine calls.

- Europe: Similar market dynamics, with incremental growth.

- Asia-Pacific: Growing due to population aging, increasing cardiovascular disease, and expanding healthcare infrastructure.

Potential Market Expansions

- Use in emergency kits and pre-hospital care settings

- Off-label applications for specific cardiac conditions

- New formulations (e.g., fast-dissolving or longer-acting variants)

Key Opportunities

- Expansion into ambulatory and outpatient care

- Price competition with generics

- Development of novel drug delivery systems to improve stability

Risks and Barriers

- Patent expiration leading to increased generic competition

- Regulatory challenges linked to manufacturing quality

- Shifts in treatment guidelines favoring alternative therapies

Key Takeaways

- Nitrostat remains a leading sublingual nitrates medication with an estimated US market size of $70 million in 2022.

- Market growth hinges on the rising prevalence of angina and CAD, projected at 3% CAGR through 2028.

- Competition from generics and alternative formulations will influence future sales.

- Strategic expansion into outpatient and emergency settings presents opportunities.

- Regulatory and manufacturing considerations impact supply stability and sales continuity.

Frequently Asked Questions

-

What factors influence Nitrostat's sales in the US?

Prescribing habits, patient preference for delivery forms, insurance coverage, and competition from generics.

-

How does Nitrostat compare to other nitrates?

It offers rapid relief via sublingual administration but faces competition from longer-acting options and alternative drug classes.

-

What is the outlook for generic versions?

Patent expirations increase generic availability, likely lowering prices and impacting brand sales.

-

Are there new formulations in development?

Emerging formulations aim to improve stability, onset time, and duration, which could alter market dynamics.

-

How is the global market evolving?

Growth is driven by increasing cardiovascular disease incidence, healthcare infrastructure expansion, and aging populations, especially in emerging markets.

References

[1] World Health Organization. Cardiovascular diseases, 2022.

[2] Global Burden of Disease Study, 2022.