Share This Page

Drug Sales Trends for LIPITOR

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for LIPITOR (2022)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

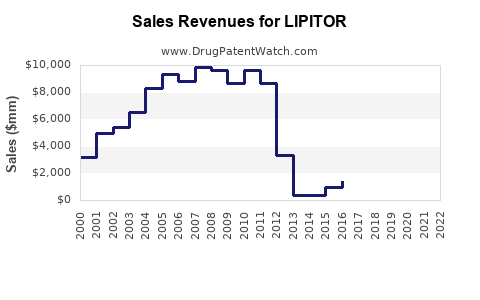

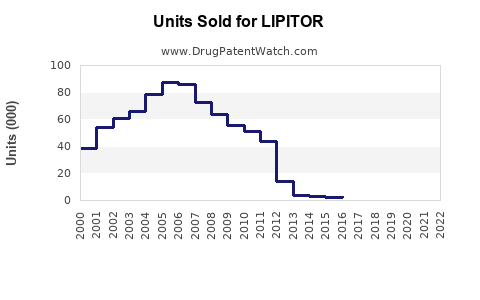

Annual Sales Revenues and Units Sold for LIPITOR

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| LIPITOR | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| LIPITOR | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| LIPITOR | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| LIPITOR | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| LIPITOR | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

LIPITOR: Global Market Performance and Sales Forecast

Lipitor (atorvastatin calcium) is a statin drug used to lower cholesterol and reduce the risk of heart attack and stroke. Its patent protection expired in the U.S. in 2011 and in Europe in 2012. This analysis examines the drug's historical sales performance, market trajectory post-patent expiry, and projections for its future market presence.

What Was Lipitor's Peak Market Performance?

Lipitor achieved peak annual sales in 2008, generating $12.9 billion globally. This figure represents the drug's zenith during its period of market exclusivity. The United States accounted for the largest portion of these sales, followed by major European markets and Japan. The drug's efficacy in managing hyperlipidemia and its widespread physician adoption contributed to its blockbuster status.

Table 1: Lipitor Global Sales Performance (Selected Years)

| Year | Global Sales (USD Billions) | U.S. Sales (USD Billions) | International Sales (USD Billions) |

|---|---|---|---|

| 2006 | 12.7 | 7.3 | 5.4 |

| 2007 | 12.8 | 7.4 | 5.4 |

| 2008 | 12.9 | 7.5 | 5.4 |

| 2009 | 11.2 | 6.1 | 5.1 |

| 2010 | 10.7 | 5.5 | 5.2 |

Source: Pfizer Annual Reports (2006-2010)

How Did Patent Expiry Impact Lipitor Sales?

The expiration of Lipitor's primary patents led to the introduction of generic atorvastatin by numerous pharmaceutical manufacturers. This event significantly impacted Lipitor's market share and revenue. Generic competition typically drives down prices due to increased supply and lower production costs, leading to a substantial decline in sales for the branded originator drug.

Following its U.S. patent expiry in November 2011, Lipitor's sales experienced a precipitous drop. By the end of 2012, global sales had fallen to $6.2 billion, a decline of over 50% from its peak. This trend continued as generic versions became more widely available and prescribed.

Table 2: Lipitor Global Sales Post-Patent Expiry (Selected Years)

| Year | Global Sales (USD Billions) | U.S. Sales (USD Billions) | International Sales (USD Billions) |

|---|---|---|---|

| 2011 | 8.2 | 4.5 | 3.7 |

| 2012 | 6.2 | 2.9 | 3.3 |

| 2013 | 4.4 | 1.8 | 2.6 |

| 2014 | 3.1 | 1.1 | 2.0 |

| 2015 | 2.0 | 0.7 | 1.3 |

Source: Pfizer Annual Reports (2011-2015)

What is the Current Market Share of Branded Lipitor vs. Generic Atorvastatin?

Post-patent expiry, branded Lipitor has a negligible market share in most major pharmaceutical markets. The vast majority of atorvastatin prescriptions are now filled by generic versions. In the U.S., for instance, generic atorvastatin dominates the market for HMG-CoA reductase inhibitors (statins) in terms of prescription volume. Branded Lipitor may retain a small segment of market share among patients who have historically been prescribed it and have not switched, or in specific niche markets where generic penetration is slower.

Estimates indicate that generic atorvastatin accounts for over 95% of all atorvastatin prescriptions in developed markets by 2023. The remaining market share for branded Lipitor is largely confined to regions with less mature generic drug markets or specific payer formulary arrangements that might still favor the branded product in limited scenarios.

What are the Key Factors Influencing the Generic Atorvastatin Market?

The generic atorvastatin market is primarily driven by several factors:

- Price Competitiveness: Generic manufacturers compete intensely on price, offering atorvastatin at a fraction of the cost of branded Lipitor. This is the primary driver for physician and patient adoption.

- Regulatory Approvals: Generic drug approval processes, such as those by the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), ensure bioequivalence and therapeutic interchangeability with the branded product.

- Supply Chain and Manufacturing: The global supply chain for active pharmaceutical ingredients (APIs) and finished dosage forms is robust, with multiple manufacturers producing generic atorvastatin.

- Physician and Pharmacy Practices: Prescription patterns have largely shifted to generics. Pharmacies routinely substitute generic versions unless a "dispense as written" instruction is provided.

- Healthcare Payer Policies: Insurance providers and national health systems often mandate or strongly encourage the use of generics through formulary tiering and reimbursement policies.

What is the Projected Future Market for Atorvastatin?

The market for atorvastatin, encompassing both branded Lipitor and its generic equivalents, is expected to remain substantial, albeit with continued dominance by generics. Demand is driven by the persistent and growing prevalence of cardiovascular disease globally, necessitating cholesterol-lowering therapies.

Projected market growth will be slow and primarily influenced by population demographics, the increasing incidence of dyslipidemia, and the cost-effectiveness of statin therapy. The market will continue to be characterized by high volume, low-price generic competition.

Estimates suggest the global market for atorvastatin (all forms) will stabilize around $4 billion to $6 billion annually in the coming years. Branded Lipitor's contribution to this total will remain minimal, likely under $100 million annually. The growth within this market will be almost entirely attributable to the volume of generic atorvastatin prescriptions.

Key drivers for sustained demand include:

- Aging Global Population: Older individuals are at higher risk for cardiovascular events, increasing demand for preventative therapies.

- Rising Obesity Rates: Increased obesity contributes to dyslipidemia and a greater need for statin treatment.

- Guidelines for Cardiovascular Prevention: Current medical guidelines recommend statin therapy for a broad range of patients at risk of cardiovascular disease.

What is the Competitive Landscape for Atorvastatin?

The competitive landscape for atorvastatin is saturated with generic manufacturers. Major players include, but are not limited to, Teva Pharmaceuticals, Mylan (now Viatris), Sandoz (a division of Novartis), and numerous Indian pharmaceutical companies like Dr. Reddy's Laboratories, Sun Pharmaceutical Industries, and Cipla.

Competition within the generic atorvastatin market is based on:

- Manufacturing Efficiency: Companies with lower production costs can offer more competitive pricing.

- Distribution Networks: Extensive distribution capabilities ensure widespread availability.

- Quality and Compliance: Maintaining high manufacturing standards and regulatory compliance is essential.

- Pricing Strategies: Manufacturers adjust pricing based on market dynamics and competitor offerings.

Branded Lipitor, as a product, plays a very minor role in this landscape, largely serving as a reference product for bioequivalence studies for new generic entrants.

What Are the Regulatory Considerations for Atorvastatin?

The regulatory environment for atorvastatin remains consistent with that for all generic drugs. Manufacturers must adhere to strict Good Manufacturing Practices (GMP) and demonstrate bioequivalence to the reference listed drug (Lipitor) through pharmacokinetic and, in some cases, clinical studies.

Regulatory bodies like the FDA, EMA, and others worldwide oversee the approval and post-market surveillance of generic atorvastatin. This includes monitoring for adverse events, ensuring consistent product quality, and managing any potential supply chain disruptions. The generic approval process aims to guarantee that patients receive a safe and effective treatment equivalent to the original branded medication.

Key Takeaways

- Lipitor (atorvastatin calcium) was a highly successful drug, reaching peak global sales of $12.9 billion in 2008.

- Patent expiration in 2011 (U.S.) and 2012 (Europe) led to rapid market erosion, with sales falling to $6.2 billion by 2012.

- Branded Lipitor now holds a minimal market share, with generic atorvastatin accounting for over 95% of prescriptions in developed markets.

- The generic atorvastatin market is driven by price competitiveness, regulatory approval, and favorable healthcare payer policies.

- The global atorvastatin market is projected to stabilize between $4 billion and $6 billion annually, with continued dominance by generic versions.

- The competitive landscape is characterized by numerous generic manufacturers vying for market share through efficiency and pricing.

Frequently Asked Questions

-

When did Lipitor's primary patents expire in key markets? Lipitor's primary patents expired in the United States in November 2011 and in major European markets in 2012.

-

What is the typical price difference between branded Lipitor and generic atorvastatin? Generic atorvastatin is typically priced at 70-90% less than branded Lipitor was at its peak, with ongoing price reductions due to intense generic competition.

-

Are there any remaining patent protections for Lipitor? While primary composition of matter and use patents have expired, secondary patents related to specific formulations or manufacturing processes might exist, but they have not effectively prevented widespread generic entry.

-

What is the global market size for all statin drugs currently? The global statin market, encompassing all statin drugs (including atorvastatin, simvastatin, rosuvastatin, etc.), is estimated to be valued at approximately $25 billion to $30 billion annually.

-

Which regions have the highest prescription rates for generic atorvastatin? Developed markets such as the United States, Canada, Western Europe, and Australia exhibit the highest prescription rates for generic atorvastatin due to established generic substitution practices and healthcare policies.

Citations

[1] Pfizer Inc. (2007). Pfizer Inc. 2006 Annual Report. [2] Pfizer Inc. (2008). Pfizer Inc. 2007 Annual Report. [3] Pfizer Inc. (2009). Pfizer Inc. 2008 Annual Report. [4] Pfizer Inc. (2010). Pfizer Inc. 2009 Annual Report. [5] Pfizer Inc. (2011). Pfizer Inc. 2010 Annual Report. [6] Pfizer Inc. (2012). Pfizer Inc. 2011 Annual Report. [7] Pfizer Inc. (2013). Pfizer Inc. 2012 Annual Report. [8] Pfizer Inc. (2014). Pfizer Inc. 2013 Annual Report. [9] Pfizer Inc. (2015). Pfizer Inc. 2014 Annual Report. [10] Pfizer Inc. (2016). Pfizer Inc. 2015 Annual Report.

More… ↓