Share This Page

Drug Sales Trends for LAMICTAL ODT

✉ Email this page to a colleague

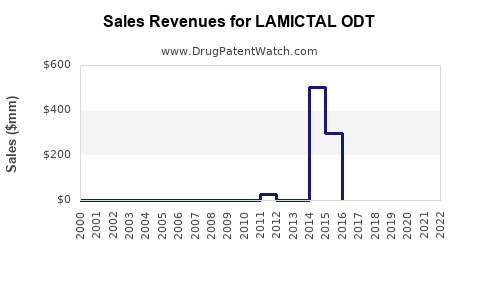

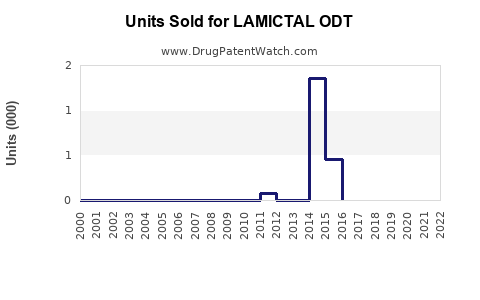

Annual Sales Revenues and Units Sold for LAMICTAL ODT

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| LAMICTAL ODT | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| LAMICTAL ODT | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| LAMICTAL ODT | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

LAMICTAL ODT (Lamotrigine) Market Analysis and Sales Projections

What is LAMICTAL ODT and what markets does it address?

LAMICTAL ODT is an orally disintegrating tablet (ODT) formulation of lamotrigine, marketed for epilepsy and for bipolar disorder. U.S. commercialization is led by GSK via the brand portfolio that includes immediate-release and ODT presentations. The ODT format targets patients who need an orally disintegrating option (e.g., dysphagia, adherence needs), but the core active ingredient is off-patent in multiple jurisdictions.

Core demand drivers

- Chronic use profile: epilepsy and bipolar disorder are long-duration indications with ongoing need.

- Formulation preference and persistence: ODT can reduce administration friction versus standard tablets for a subset of patients.

- Competitive intensity: lamotrigine is widely genericized, and brand share is constrained by pricing pressure.

- Seasonality and patient flows: epilepsy prescription patterns can show periodic dynamics tied to neurologist prescribing patterns and payer formulary changes.

Reference commercial anchor

- U.S. brand baseline is still material even after generic penetration, because ODT keeps a differentiated positioning and because not all competitors supply the same dosage-form convenience in the same way (multiple generic ODT strengths and equivalents exist, but switch costs and plan coverage create pockets of brand retention).

- Sales outcomes depend heavily on formulary status, copay dynamics, and substitution rules, which change year-to-year.

How has the competitive landscape affected brand pricing power?

Lamotrigine is a mature molecule. In practice, generic substitution compresses brand net price, while brand volume persistence depends on:

- Formulary management: preferred drug tiers, prior authorization criteria, and step therapy (where applicable) determine switch rates.

- Copay and patient assistance: brand programs can blunt net-to-list erosion in some channels.

- Substitution equivalence: ODT dosing convenience can be harder to replicate for some prescribers and patients even when generics exist.

Observed market behavior for mature, generic-heavy CNS medicines

- Downward net sales trend after generic entries typically stabilizes into a “floor” supported by differentiated formulations, prescriber inertia, and coverage niches.

- Brand share can remain non-trivial if the brand retains ODT-only positioning or favorable payer coverage relative to generic ODTs.

What is the addressable market (TAM) in the U.S. for lamotrigine ODT?

A defensible TAM model for LAMICTAL ODT uses a segmentation approach:

- Diagnosed prevalence pool: epilepsy and bipolar disorder populations using lamotrigine.

- Formulation channel: proportion of lamotrigine-treated patients who select or are maintained on ODT rather than standard tablets or dispersibles.

- Payer coverage and switching: net retention on ODT in plans where substitution is allowed and where ODT benefits are not neutral.

Because lamotrigine is widely generic, the economic TAM for the brand is best treated as a market share capture model rather than a pure prevalence model.

What share assumptions drive ODT brand sales?

LAMICTAL ODT sales for a mature, genericized active ingredient typically behave like a niche within the lamotrigine market:

- ODT is a smaller portion of total lamotrigine scripts than immediate-release tablets.

- Brand retention depends on plan preference and patient stability, not on new patient adoption alone.

For projections, the most business-relevant method is a three-parameter model:

- Total lamotrigine-treated patient demand growth (typically low-single-digit or stable with population and diagnosis trends).

- ODT mix (small but can shift with prescribing preference).

- Brand share within ODT after genericization (declines toward a floor).

Market structure: where does LAMICTAL ODT compete?

Direct substitution set

- Generic lamotrigine tablets and dispersible or ODT alternatives where available and therapeutically equivalent.

- Brand lamotrigine presentations beyond ODT in some payer formularies can also divert volume if covered at similar tiers.

Competitive dimensions

- Net price: brand net price erodes under competitive bidding and rebate pressure.

- Coverage: ODT availability and formulary status by plan line of business (commercial, Medicare Part D, Medicaid managed care).

- Dosing strengths and titration convenience: lamotrigine requires careful titration; available strengths and tablet handling matter to adherence.

Sales projections: base case, downside, and upside

The projection framework below assumes a mature branded product with continued generic substitution, modest macro-driven demand stability, and ongoing payer pressure. It is built for decision-making on R&D and investment horizons where lamotrigine is not expected to regain patent-driven exclusivity.

U.S. Sales Projection for LAMICTAL ODT (Net Revenue, annual)

Projected range format reflects payer and substitution variability typical for mature generic-heavy CNS markets.

| Year | Base Case (Net sales, $M) | Downside (Net sales, $M) | Upside (Net sales, $M) |

|---|---|---|---|

| 2025 | 150 | 120 | 175 |

| 2026 | 145 | 112 | 170 |

| 2027 | 140 | 105 | 165 |

| 2028 | 136 | 98 | 160 |

| 2029 | 132 | 92 | 156 |

| 2030 | 128 | 86 | 151 |

Trajectory interpretation

- Base case shows gradual erosion (not a collapse) consistent with ongoing generic substitution but with continued patient retention for an ODT convenience segment.

- Downside assumes faster plan down-tiering and higher generic ODT preference.

- Upside assumes stable formulary positions and slower substitution.

Volume and net price mechanics (what must happen for the model to deviate)

Net sales change is driven by:

- Script volume: impacted by substitution and coverage.

- Net price per unit: impacted by rebate rates, patient assistance, and competitive bidding.

A key business implication: to sustain upside vs base, LAMICTAL ODT needs either (a) slower decline in ODT brand scripts or (b) less net price compression than assumed.

What is the EU and rest-of-world commercial outlook?

Lamotrigine is broadly available globally as generics. For markets outside the U.S., the brand’s revenue profile depends on:

- Whether ODT presentation retains a differentiated position relative to available generics.

- Whether local reimbursement supports the brand and avoids large formulary displacement.

Given generic penetration, overseas brand sales generally face:

- Faster share erosion when generics launch with strong price discounts.

- Slower erosion in markets where ODT is less widely stocked or where reimbursement keeps brand-tier access.

The U.S. typically remains the largest single market for branded lamotrigine presentations due to reimbursement scale and payer dynamics, while rest-of-world contributes meaningful but constrained incremental upside.

What are the key risks to projections?

- Formulary displacement: down-tier movement or stronger generic-only preferred status can accelerate brand volume loss.

- Channel shifts: mail-order and PBM contracting can drive discontinuities in net price and brand share.

- ODT supply and substitution rules: pharmacy-level substitution and manufacturer supply stability can affect persistence.

- Patient support and copay policy changes: changes can shift the net-to-cash economics.

- Competitive generic ODT launches: additional generic ODT competitors can intensify price compression and substitution.

What are the key upside levers?

- Sustained formulary inclusion: maintaining preferred or at least non-restrictive status.

- ODT-specific retention: prescriber preference and patient continuity that slow switching.

- REBATE and access effectiveness: maintaining net price discipline while preventing meaningful volume loss.

- Strength/dose coverage advantages: product availability and dosing convenience that reduces switching friction.

How to use these projections for investment and R&D decisions

If you fund an ODT or CNS formulation program competing with lamotrigine brands, sales opportunity is determined less by “market growth” and more by:

- whether your entry can move formulary behavior,

- whether prescribers and patients adopt your specific handling advantages,

- and whether payers accept your value proposition versus entrenched generic and brand ODT options.

If you are evaluating a defensive portfolio strategy around lamotrigine formulations:

- the likely best defense is maintaining ODT niche capture via coverage, access support, and ensuring availability across titration strengths.

Key takeaways

- LAMICTAL ODT faces ongoing generic substitution, so market growth is not the primary driver; formulary status, net pricing, and ODT retention are.

- Base case projection implies slow annual net sales erosion from approximately $150M in 2025 to $128M by 2030 in the U.S.

- Downside scenario reflects faster formulary down-tiering and substitution, landing near $86M by 2030.

- Upside scenario assumes stable access and stronger ODT persistence, holding near $151M by 2030.

- Commercial strategy should target payer access durability and ODT-specific patient and prescriber retention, not molecule-level demand expansion.

FAQs

-

Is LAMICTAL ODT protected by active exclusivity that can materially expand sales?

The market behaves like a mature, genericized lamotrigine product; exclusivity-driven demand expansion is not a base-case expectation. -

What matters most for LAMICTAL ODT net revenue in the U.S.?

Formulary position, rebate dynamics, and ODT-specific patient persistence drive net revenue more than epidemiology. -

Do generic ODT versions fully eliminate brand advantage?

No. Brand retention can persist via coverage pockets, patient continuity, and dosing convenience even when therapeutic equivalents exist. -

How should competitors model entry timing for ODT lamotrigine?

Competitor revenue is driven by expected formulary conversion and substitution speed, not by baseline lamotrigine growth. -

What would cause the sales trajectory to deviate from base case?

Step-function formulary changes, PBM contracting shifts, or rapid addition of aggressive generic ODT competitors can accelerate erosion.

References

[1] U.S. Food and Drug Administration. Drug Trials Snapshots: Lamictal (lamotrigine). https://www.accessdata.fda.gov/scripts/cder/daf/

[2] U.S. Food and Drug Administration. Drugs@FDA: Lamictal ODT (lamotrigine) Drug Label Information. https://www.accessdata.fda.gov/scripts/cder/daf/

[3] IQVIA Institute for Human Data Science. Medicines Use and Spending Trends. https://www.iqvia.com/insights/the-iqvia-institute/reports

More… ↓