Share This Page

Drug Sales Trends for DULOXETINE

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for DULOXETINE (2022)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

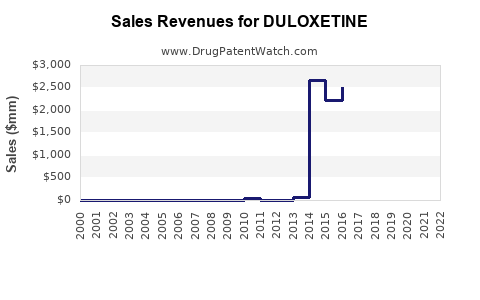

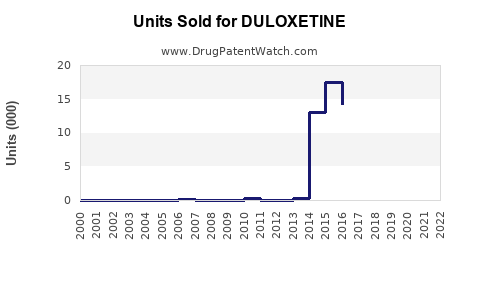

Annual Sales Revenues and Units Sold for DULOXETINE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| DULOXETINE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| DULOXETINE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| DULOXETINE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| DULOXETINE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| DULOXETINE | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| DULOXETINE | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

DULOXETINE MARKET ANALYSIS AND SALES PROJECTIONS

Duloxetine, a serotonin-norepinephrine reuptake inhibitor (SNRI), is approved for the treatment of major depressive disorder (MDD), generalized anxiety disorder (GAD), diabetic peripheral neuropathic pain (DPNP), fibromyalgia, and chronic musculoskeletal pain. The market for duloxetine is mature, with significant generic competition following patent expirations. Future growth is projected to be modest, driven by continued adoption in established indications and potential new uses.

MARKET LANDSCAPE AND KEY DRIVERS

WHAT IS THE CURRENT MARKET SIZE AND SEGMENTATION FOR DULOXETINE?

The global market for duloxetine was valued at approximately \$4.5 billion in 2022. This market is primarily segmented by indication and by region.

- By Indication:

- Major Depressive Disorder (MDD): The largest segment, accounting for an estimated 40% of the market.

- Generalized Anxiety Disorder (GAD): The second-largest segment, representing approximately 25%.

- Diabetic Peripheral Neuropathic Pain (DPNP): Approximately 15%.

- Fibromyalgia: Approximately 10%.

- Chronic Musculoskeletal Pain: Approximately 10%.

- By Region:

- North America: Dominant market, with an estimated 55% share, driven by high prevalence of target conditions and established healthcare infrastructure.

- Europe: Accounts for approximately 25% of the market.

- Asia-Pacific: Growing market, representing approximately 15%, with increasing access to healthcare and awareness of mental health conditions.

- Rest of the World (RoW): Approximately 5%.

WHAT ARE THE PRIMARY FACTORS DRIVING DULOXETINE MARKET GROWTH?

Key drivers for duloxetine market growth include:

- Rising Prevalence of Mental Health Disorders: Increasing global incidence of depression and anxiety disorders fuels demand for effective pharmacological treatments. The World Health Organization (WHO) estimates that depression affects over 280 million people worldwide. [1]

- Increasing Diagnosis and Treatment of Neuropathic Pain: Greater awareness and improved diagnostic capabilities for conditions like DPNP contribute to the use of duloxetine for pain management.

- Off-Label Prescribing and New Indications: While primarily approved for specific conditions, ongoing research and clinician experience may lead to expanded off-label use or investigation into new therapeutic areas, potentially broadening the market.

- Generic Availability and Affordability: The widespread availability of generic duloxetine has made the treatment more accessible and affordable, increasing prescription volumes, particularly in price-sensitive markets.

WHAT ARE THE MAJOR CHALLENGES FACING THE DULOXETINE MARKET?

The duloxetine market faces several significant challenges:

- Intense Generic Competition: The expiration of key patents has led to a highly competitive generic market. This has resulted in significant price erosion and reduced profit margins for original manufacturers and branded generic products.

- Therapeutic Advancements and Pipeline Competition: Development of novel antidepressants and pain management therapies with potentially improved efficacy, safety profiles, or different mechanisms of action could displace duloxetine in certain patient populations.

- Side Effect Profile and Patient Compliance: Duloxetine can cause side effects such as nausea, dry mouth, and fatigue, which can impact patient adherence to treatment.

- Regulatory Scrutiny and Post-Marketing Surveillance: Like all pharmaceuticals, duloxetine is subject to ongoing regulatory review and post-marketing surveillance, which can lead to label changes or restrictions.

PATENT LANDSCAPE AND COMPETITIVE INTELLIGENCE

WHAT IS THE PATENT STATUS OF DULOXETINE?

The primary patents for duloxetine hydrochloride (marketed originally as Cymbalta by Eli Lilly and Company) expired in the United States in December 2013 and in Europe shortly thereafter. [2] This opened the market to generic manufacturers.

- Key Patents:

- US Patent 4,956,388 (Method of treating depression and anxiety): Expired December 2013.

- US Patent 5,023,269 (Compositions containing duloxetine): Expired June 2007.

- Additional formulation and method-of-use patents also expired, further facilitating generic entry.

WHO ARE THE MAJOR GENERIC MANUFACTURERS OF DULOXETINE?

Following patent expiries, numerous pharmaceutical companies have entered the duloxetine market with generic formulations. Major players include:

- Teva Pharmaceutical Industries Ltd.

- Mylan N.V. (now part of Viatris)

- Sun Pharmaceutical Industries Ltd.

- Aurobindo Pharma Ltd.

- Lupin Ltd.

- Dr. Reddy's Laboratories Ltd.

- Endo International plc

WHAT IS THE COMPETITIVE POSITION OF DULOXETINE COMPARED TO OTHER SNRIs AND ANTIDEPRESSANTS?

Duloxetine competes with other SNRIs and different classes of antidepressants.

- Other SNRIs:

- Venlafaxine (Effexor XR): Similar efficacy profile to duloxetine but can have a more pronounced effect on blood pressure. Generic availability is high.

- Desvenlafaxine (Pristiq): Active metabolite of venlafaxine, offering a potentially simpler dosing regimen and fewer CYP2D6 interactions. Patent protection for the original product has largely expired, leading to generic competition.

- Selective Serotonin Reuptake Inhibitors (SSRIs):

- Fluoxetine (Prozac): One of the most prescribed antidepressants, known for its long half-life and activating effects. Highly genericized.

- Sertraline (Zoloft): Widely prescribed for depression, anxiety, and PTSD. Highly genericized.

- Escitalopram (Lexapro): Generally well-tolerated, often preferred for its milder side effect profile. Highly genericized.

- Other Antidepressant Classes:

- Tricyclic Antidepressants (TCAs): Older class, generally reserved for treatment-resistant depression due to a higher risk of side effects and overdose toxicity.

- Atypical Antidepressants: Agents like bupropion (Wellbutrin) and mirtazapine (Remeron) offer different mechanisms and side effect profiles, providing alternatives for patients who do not respond to or tolerate SSRIs/SNRIs.

Duloxetine's advantage lies in its dual mechanism (serotonin and norepinephrine reuptake inhibition), which is particularly beneficial for comorbid conditions like depression with pain symptoms. However, the extensive generic competition limits significant pricing power.

SALES PROJECTIONS AND MARKET FORECAST

WHAT ARE THE PROJECTED SALES FOR DULOXETINE GLOBALLY OVER THE NEXT FIVE YEARS?

The global duloxetine market is expected to experience a Compound Annual Growth Rate (CAGR) of approximately 2% from 2023 to 2028.

- 2023 Estimated Revenue: \$4.6 billion

- 2028 Projected Revenue: Approximately \$5.1 billion

This modest growth is primarily attributed to the ongoing generic market dynamics, which keep prices low despite increasing prescription volumes. Regional growth will vary, with the Asia-Pacific region showing a higher percentage growth rate due to increasing market penetration.

WHAT ARE THE GROWTH PROSPECTS FOR DULOXETINE IN SPECIFIC GEOGRAPHIC REGIONS?

- North America: Expected to maintain its market leadership but with slower growth (CAGR ~1.5%). Increased patient volumes will be offset by continued price pressure from generic competition.

- Europe: Moderate growth projected (CAGR ~2%). Increased adoption in Eastern European markets will contribute to overall regional expansion.

- Asia-Pacific: Forecasted to be the fastest-growing region (CAGR ~4-5%). Factors include expanding healthcare access, rising disposable incomes, increased awareness of mental health, and a growing prevalence of diabetes leading to DPNP.

- Rest of the World (RoW): Growth is expected to be driven by developing economies (CAGR ~3%), contingent on improved healthcare infrastructure and affordability.

WHAT ARE THE POTENTIAL NEW INDICATIONS OR THERAPEUTIC USES THAT COULD IMPACT DULOXETINE'S MARKET POSITION?

While duloxetine has established indications, research continues into its potential efficacy in other areas.

- Stress Urinary Incontinence (SUI): Duloxetine is approved in some regions for SUI. Continued evidence supporting its efficacy and safety in this indication could lead to increased utilization.

- Hot Flashes Associated with Menopause: Studies have explored duloxetine's role in managing vasomotor symptoms of menopause, although it is not a primary indication.

- Other Chronic Pain Syndromes: Ongoing research into neuropathic and non-neuropathic chronic pain conditions may reveal further therapeutic opportunities.

However, the development of new indications faces significant hurdles, including the cost of clinical trials and the challenge of differentiating from existing generic options in a price-sensitive market. The primary growth will continue to stem from its established therapeutic areas.

KEY TAKEAWAYS

The global duloxetine market is characterized by robust generic competition following the expiration of key patents. Market size is substantial, driven by demand for MDD, GAD, and neuropathic pain treatments. Future growth is projected to be modest, with slight increases in revenue driven by higher prescription volumes and expansion in emerging markets, particularly in the Asia-Pacific region. Significant price erosion due to generic availability remains a primary market dynamic.

FREQUENTLY ASKED QUESTIONS

-

What is the primary mechanism of action for duloxetine? Duloxetine is a serotonin-norepinephrine reuptake inhibitor (SNRI). It works by increasing the levels of serotonin and norepinephrine in the brain, neurotransmitters that play a role in mood and pain perception.

-

Are there any significant safety concerns associated with duloxetine use? Common side effects include nausea, dry mouth, constipation, insomnia, and dizziness. More serious risks include suicidal thoughts, liver damage, and potential for serotonin syndrome. Patients should be closely monitored by healthcare professionals.

-

How does duloxetine's efficacy compare to SSRIs for depression? Duloxetine has demonstrated comparable efficacy to SSRIs in treating major depressive disorder. Its dual mechanism may offer an advantage in patients with comorbid pain symptoms, as norepinephrine also plays a role in pain modulation.

-

What is the typical dosage range for duloxetine? Dosages vary based on the indication. For MDD and GAD, the typical starting dose is 60 mg once daily, with potential increases up to 120 mg per day. For DPNP and fibromyalgia, the recommended dose is usually 60 mg once daily.

-

Can duloxetine be used to treat chronic pain conditions other than diabetic neuropathy and fibromyalgia? While duloxetine is specifically approved for DPNP and fibromyalgia, healthcare providers may prescribe it off-label for other chronic pain conditions based on clinical judgment and emerging evidence of efficacy.

CITATIONS

[1] World Health Organization. (2021). Depression. https://www.who.int/news-room/fact-sheets/detail/depression

[2] U.S. Food and Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. Retrieved from https://www.fda.gov/drugs/drug-approvals-and-databases/orange-book-approved-drug-products-therapeutic-equivalence-evaluations

More… ↓