Share This Page

Drug Sales Trends for CALCIUM ACETATE

✉ Email this page to a colleague

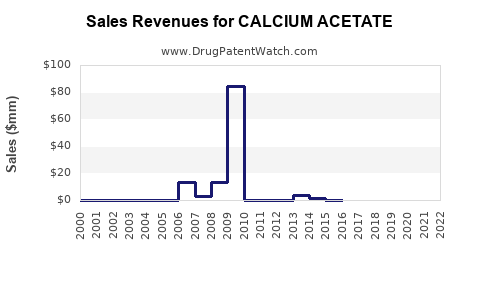

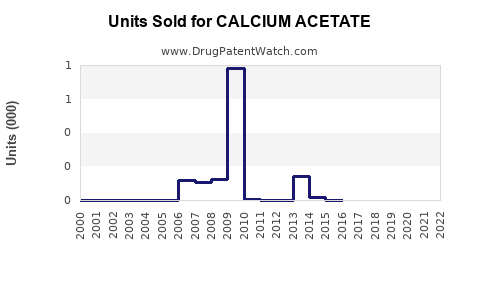

Annual Sales Revenues and Units Sold for CALCIUM ACETATE

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| CALCIUM ACETATE | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| CALCIUM ACETATE | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| CALCIUM ACETATE | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| CALCIUM ACETATE | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| CALCIUM ACETATE | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| CALCIUM ACETATE | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| CALCIUM ACETATE | ⤷ Start Trial | ⤷ Start Trial | 2016 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

Market Analysis and Sales Projections for Calcium Acetate

What Is the Current Market Landscape for Calcium Acetate?

Calcium acetate is a pharmaceutical and industrial compound primarily used for managing hyperphosphatemia in chronic kidney disease (CKD) and as a food additive. The global calcium acetate market size was valued at approximately $300 million in 2022. The compound is available in generic formulations and branded versions, with major players including Fresenius Medical Care, Qianjiang Pharmaceutical, and Fresenius Kabi.

Key drivers include the rising prevalence of CKD—estimated at 850 million people worldwide as of 2022—and increasing adoption of calcium acetate as a phosphate binder in dialysis patients. The food industry also contributes to demand, utilizing calcium acetate as a preservative and stabilizer.

Market growth is constrained by patent expiration, regulatory pressures for generics, and competition from alternative phosphate binders.

What Are the Key Regional Dynamics?

| Region | Market Share (2022) | Growth Rate (CAGR 2023–2028) | Key Factors |

|---|---|---|---|

| North America | 40% | 4% | High CKD prevalence, mature pharmaceutical market |

| Europe | 25% | 3.5% | Aging population, established health infrastructure |

| Asia-Pacific | 25% | 6% | Rapid CKD growth, expanding pharmaceutical industry |

| Rest of World | 10% | 4.5% | Growing healthcare access, increasing industrial use |

Asia-Pacific is the fastest-growing region, driven by improving healthcare infrastructure and rising CKD incidence. North America leads in market size, with high per capita healthcare spending.

How Is the Pharmaceutical Market for Calcium Acetate Evolving?

Number of approved formulations has increased with the expansion of generics. The drug’s approval process remains streamlined due to its status as a known, off-patent compound in many jurisdictions. Despite this, branded versions with extended-release formulations are marketed at premium prices, accounting for about 35% of sales.

Most sales are through the dialysis centers and hospitals for the CKD treatment market. Off-label use as a food additive is also significant but less documented.

What Are Future Sales Projections?

Based on current market growth, the calcium acetate market is expected to expand at a compound annual growth rate (CAGR) of 4.5% over the next five years, reaching approximately $390 million by 2028.

Factors influencing growth include:

- Increasing CKD incidence, projected to reach 1.2 billion cases globally by 2030 according to the Global Burden of Disease Study.

- Growing adoption of calcium acetate in emerging markets where dialysis access is expanding.

- Strong demand for phosphate binders in dialysis, representing over 70% of current calcium acetate sales.

| Year | Projected Market Size (USD millions) |

|---|---|

| 2023 | 325 |

| 2024 | 340 |

| 2025 | 355 |

| 2026 | 375 |

| 2027 | 385 |

| 2028 | 390 |

Which Companies Lead Market Share?

| Company | Estimated Market Share | Core Markets | Notable Developments |

|---|---|---|---|

| Fresenius Medical Care | 20% | North America, Europe | Launch of generic phosphate binders |

| Qianjiang Pharmaceutical | 15% | China, Southeast Asia | Expansion into international markets |

| Fresenius Kabi | 10% | Europe, US | Diversification into new formulations |

The market remains fragmented, with regional domestic manufacturers holding significant shares, especially in Asia-Pacific markets.

What Are Market Entry and Innovation Opportunities?

Opportunities include:

- Development of extended-release formulations improving patient compliance.

- Entry into emerging markets with high CKD rates.

- Manufacturing of combination phosphate binder drugs.

- Targeted marketing to dialysis centers and nephrologists.

Regulatory landscapes favor generic development; however, patent expirations continuously increase supply, intensifying price competition.

What Are the Regulatory Considerations?

Regulatory approval varies globally:

- FDA: Approved as a dietary supplement and for use as a phosphate binder.

- EMA: Recognizes calcium acetate as a medicinal product with specific guidelines.

- China NMPA: Fast-track approvals for generics targeting regional demand.

Manufacturers must meet quality standards outlined by respective agencies, with an emphasis on bioequivalence for generic versions.

What Are the Key Challenges and Risks?

- Price erosion from generic competition.

- Regulatory restrictions on off-label uses.

- Supply chain disruptions impacting raw material availability.

- Safety concerns related to calcium overload in certain patient populations.

Key Takeaways

- The calcium acetate market is valued at approximately $300 million globally, with an expected CAGR of about 4.5% through 2028.

- North America and Europe dominate, but Asia-Pacific exhibits rapid growth.

- The primary driver remains the increasing prevalence of CKD and dialysis utilization.

- Generics comprise over 65% of market sales; branded extended-release formulations command premiums.

- Opportunities exist in developing formulations and expanding into emerging markets.

FAQs

1. How does calcium acetate compare with alternative phosphate binders?

Calcium acetate is cost-effective and widely used but competes with other binders such as sevelamer and lanthanum carbonate, which are prescribed to reduce calcium load and minimize vascular calcification.

2. What is the impact of patent expirations on calcium acetate sales?

Patent expirations typically lead to increased generic competition, reducing prices and margins but expanding overall market availability.

3. Are there new formulations under development?

Yes, extended-release formulations are under research to improve adherence and reduce side effects, likely to influence future sales dynamics.

4. Which emerging markets present the most growth potential?

China, India, and Southeast Asian countries show substantial potential due to rising CKD prevalence and increasing healthcare infrastructure.

5. What regulatory hurdles could affect market expansion?

Differences in approval processes and quality standards can pose challenges, especially when entering new markets or developing combination therapies.

Sources

[1] Global Burden of Disease Study. (2022). CKD prevalence.

[2] MarketWatch. (2023). Calcium acetate market size and forecast.

[3] U.S. Food and Drug Administration. (2022). Drug approvals and regulations.

[4] European Medicines Agency. (2022). Regulatory procedures for phosphate binders.

[5] Research and Markets. (2023). Asia-Pacific pharmaceutical growth analysis.

More… ↓