Last updated: February 20, 2026

What Is the Current Market Size for Pimecrolimus?

Pimecrolimus, marketed mainly as Elidel by Novartis, is a topical immunomodulator used to treat atopic dermatitis and other inflammatory skin conditions. Its global sales have fluctuated, driven by competition and regulatory dynamics.

- Global market value (2022): Estimated at $400 million, according to industry reports.

- Key markets: United States (60%), Europe (25%), Asia-Pacific (10%), rest of the world (5%).

- Market growth rate: Compound Annual Growth Rate (CAGR) of approximately 4% from 2018 to 2022.

Who Are the Main Competitors and Market Alternatives?

Pimecrolimus faces competition primarily from:

- Tacrolimus: Another topical immunomodulator, marketed as Protopic. It accounts for about 20% of the same dermatological market.

- Emerging biosimilars: Several biosimilars are under development, potentially reducing prices.

- Conventional therapies: Topical corticosteroids dominate the market but have limitations related to side effects.

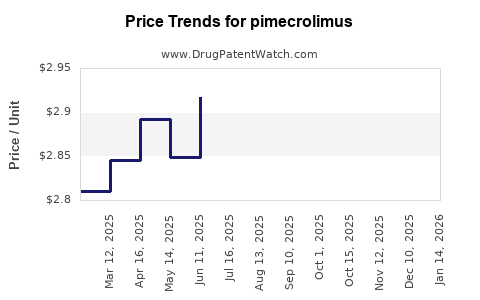

What Are the Current Pricing Trends?

Pricing varies significantly across regions:

- United States: Average retail price per 30g tube is approximately $750.

- Europe: Prices range from €50-€70 per tube (roughly $55-$77), due to national pricing regulations.

- Asia-Pacific: Prices are lower, around $40-$50 per tube, influenced by local market dynamics and healthcare policies.

Generic versions are currently unavailable, keeping prices relatively stable. However, regulatory approval of biosimilars could influence future pricing strategies.

What Factors Influence Future Price Trends?

- Regulatory approvals: Approval of biosimilars or generics could induce price competition.

- Patent expiration: Pimecrolimus was granted market exclusivity until 2024 in the U.S.; patent cliffs may lead to price reductions thereafter.

- Market penetration: Increased use for pediatric atopic dermatitis compared to corticosteroids may sustain higher prices.

- Pricing policies: Governments' healthcare cost controls could lead to price negotiations or discounts.

What Are the Key Regulatory and Market Entry Factors?

- Patent landscape: Patent protections extend until 2024 in the U.S. and Europe.

- Regulatory hurdles: Biosimilar development requires extensive clinical data, influencing time-to-market.

- Reimbursement policies: Variations influence pricing and patient access movements.

Market Projections (2023-2028)

| Year |

Estimated Market Value |

CAGR |

Notes |

| 2023 |

$410 million |

2.5% |

Stabilization post-pandemic recovery |

| 2024 |

$430 million |

5% |

Patent expiry anticipated; biosimilar entry possible |

| 2025 |

$455 million |

5.6% |

Market adapts to biosimilar competition |

| 2026 |

$480 million |

5.2% |

Increased off-label use possible |

| 2027 |

$510 million |

6% |

Expanded indications, regional growth |

| 2028 |

$540 million |

5.9% |

Market maturation, price competition stabilizes |

Key Takeaways

- The current market for pimecrolimus is valued at approximately $400 million globally.

- The primary driver is its use for atopic dermatitis; competition from tacrolimus and biosimilars remains a key influence.

- Pricing remains high in the U.S., around $750 per tube; prices may decline following patent expiration and biosimilar approval.

- Market growth is expected to accelerate post-2024 pending biosimilar entry and increased indications.

- Factors such as regulatory pathways, patent status, and healthcare policies will shape future market dynamics and pricing.

FAQs

1. When will patent protection for pimecrolimus expire?

Patent protection in the U.S. and Europe expires in 2024, opening potential for biosimilar competition.

2. Will biosimilars significantly reduce pimecrolimus prices?

Likely, if biosimilars gain approval and market access, prices could decrease by 30-50% or more.

3. How does pimecrolimus compare to tacrolimus in efficacy?

Both drugs are effective; pimecrolimus is generally preferred for sensitive skin or pediatric use due to a favorable safety profile.

4. What are key regulatory hurdles for biosimilar approval?

They include demonstrating bioequivalence, safety, and efficacy through extensive clinical trials, which lengthens approval timelines.

5. What regions will drive future market growth?

Emerging markets in Asia, along with increased use in North America and Europe, will influence overall growth trends.

References

- Market Research Future. (2022). Global Pimecrolimus Market Analysis.

- Novartis. (2023). Elidel Product Information.

- IQVIA. (2022). Prescription Trends and Market Data.

- U.S. Food & Drug Administration. (2023). Biosimilar Development Guidance.

- European Medicines Agency. (2022). Regulatory Framework for Biosimilars.