Share This Page

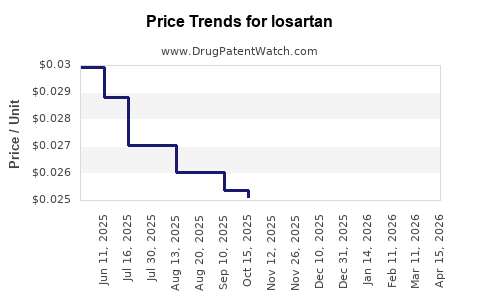

Drug Price Trends for losartan

✉ Email this page to a colleague

Average Pharmacy Cost for losartan

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| LOSARTAN POTASSIUM 100 MG TAB | 11788-0102-30 | 0.04353 | EACH | 2026-06-24 |

| LOSARTAN POTASSIUM 50 MG TAB | 11788-0101-30 | 0.03367 | EACH | 2026-06-24 |

| LOSARTAN POTASSIUM 100 MG TAB | 82009-0044-10 | 0.04353 | EACH | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for losartan

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| COZAAR 50MG TAB | Organon LLC | 78206-0122-02 | 90 | 254.89 | 2.83211 | EACH | 2024-01-06 - 2027-01-14 | Big4 |

| COZAAR 100MG TAB | Organon LLC | 78206-0123-02 | 90 | 526.21 | 5.84678 | EACH | 2024-01-06 - 2027-01-14 | FSS |

| COZAAR 25MG TAB | Organon LLC | 78206-0121-01 | 90 | 186.61 | 2.07344 | EACH | 2022-01-15 - 2027-01-14 | Big4 |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

Losartan market analysis and price projections: demand drivers, generic pricing outlook, and U.S. exclusivity/expiration map

Losartan is a mature, high-volume angiotensin II receptor blocker (ARB) with U.S. availability dominated by generics and limited brand exposure. Price is structurally pressured by wholesale generic competition, multi-source sourcing, and payer-driven rebates. Near-term U.S. price movements are likely to be modest in magnitude and concentrated in select dose strengths and tablet vs. combination SKUs, while volume growth is driven by guideline adherence, formulary coverage, and switching within ARBs rather than brand-to-generic conversion.

Bottom line: Expect flat-to-down average net price over the next 12 to 36 months for most losartan-only tablets, with localized increases possible for constrained strengths or specific combination products, and continued share shifting toward lowest-cost multisource SKUs.

What is the losartan market size, sales mix, and revenue exposure by geography and payer?

Featured snippet:

- Losartan is largely generic in the U.S., so revenue is split across multiple manufacturers with limited brand-like pricing power.

- Growth is primarily substitution-driven (other ARBs to losartan or among generics) and dosing regimen expansion rather than premium pricing.

U.S. demand profile and payer mix

Losartan’s core market is hypertension, with add-on use in selected populations (including proteinuric CKD and other guideline-supported indications). In practice, payer formularies treat losartan as a preferred ARB “cost anchor” when contracts favor specific NDCs. As a result:

- Share is sensitive to state Medicaid preferred drug lists and Medicare Part D formulary tiering.

- Net pricing is dominated by rebate mechanics and contracted distributor pricing rather than list price.

International exposure

Internationally, ARB penetration varies by payer structure, patent transition timing, and local generic competition intensity. Countries with later generic liberalization or stronger local manufacturing protections tend to show higher baseline pricing persistence, but the overall downtrend follows global genericization patterns.

How is losartan priced in the U.S. versus key international markets, and what drives net price?

Featured snippet:

- Net price in the U.S. for generic losartan is driven by AMP dynamics, contract pricing, and NDC-level competition more than by wholesale list price.

Key pricing mechanics

- Generic competition by strength and manufacturer

Losartan tablets have many therapeutically substitutable generics, which creates rapid erosion in negotiated price as more suppliers enter. - Payer contracting and PBM rebates

Even with generics, PBMs and integrated payers negotiate rebates or fees tied to formulary inclusion and preferred placement. - NDC concentration and supply constraints

Temporary disruptions, plant outages, or regulatory issues can lift specific NDC pricing, but these effects are usually short-lived unless sustained.

Price level vs. price trend

- List prices can remain stable due to standard WAC-to-NADAC/AMP behavior, but average realized net prices trend downward as competitive pressure intensifies.

- Where losartan is substituted for other ARBs, the market can show volume resilience even as pricing declines.

What is the historical and current losartan price trend (generic tablet and combination products)?

Featured snippet:

- Losartan’s generic erosion pattern typically shows steep declines post-entry, then flattening as the market saturates.

Historical pattern typical of mature generics

- Early generics: larger step-downs after initial entry.

- Later multi-source stage: slower decline and more stable net price.

- Concentration episodes: brief volatility when supply tightens for specific strengths.

Combination product impact

Losartan’s price behavior can differ for fixed-dose combinations (for example, losartan combined with hydrochlorothiazide). Combination SKUs can maintain comparatively higher net prices because:

- fewer immediate competitors at the exact dosage combinations, and

- substitution dynamics depend on matching tablet strength and dosing equivalence.

When does losartan lose exclusivity, and what does that mean for pricing in 2026–2029?

Featured snippet:

- Losartan is long past U.S. primary brand exclusivity for the active ingredient; pricing is governed by generic competition rather than exclusivity timing.

Exclusivity and patent reality for a mature ARB

Losartan’s U.S. pricing outlook is driven by:

- multi-source generic entry,

- any remaining formulation/process protection (where still enforceable), and

- FDA approvals for ANDAs with Paragraph IV challenges on relevant patents (if any active, case-specific).

Because the market is already genericized, “loss of exclusivity” typically does not create a new, discrete price crash. Instead, new entry and label expansions cause incremental downward pressure.

What patents protect losartan in the U.S., and how strong is the remaining patent estate?

Featured snippet:

- For losartan as an active ingredient, the meaningful enforcement risk is now centered on formulation/process or specific combination indications/dose forms, not first-wave composition-of-matter.

Patent estate relevance to price

Even if remaining patents exist for certain specific claims (for example, formulation variants or manufacturing methods), the practical effect on market price usually depends on:

- whether the claims cover broadly substitutable products, and

- whether there are enforceable barriers preventing generic entry for key strengths/dosage forms.

For pricing projections, the critical question is not “how many patents exist,” but whether they constrain supply at enough NDCs to affect total market competition.

How likely are further generic or authorized generic launches for losartan, and what price declines would follow?

Featured snippet:

- Additional generic launches at already saturated NDCs typically lead to marginal price erosion rather than structural reset, unless supply gaps or enforceable barriers break.

Market entry mechanics

New entrants can occur via:

- ANDA approvals for existing strengths,

- 505(b)(2) label changes (less common for a fully generic molecule),

- combination expansions, or

- authorized generic agreements (rare for fully saturated products but possible for specific label niches).

Price impact by entry type

- More competitors for the same strength: lowers competitive negotiated price and shifts share to lowest-cost NDCs.

- Entry for previously constrained strengths: produces temporary price normalization downward.

- Authorized generic entry: can compress prices quickly if it changes payer preferred-NDC landscape.

How does losartan compare with other ARBs on pricing, volume stability, and competitive risk?

Featured snippet:

- Losartan typically prices below many newer ARBs and is treated as a low-cost ARB class option in formularies.

Competitive positioning

Compared with ARBs such as valsartan, irbesartan, olmesartan, and telmisartan, losartan’s market behavior is shaped by:

- payer tendency to prefer lower acquisition cost,

- generic breadth (many equivalent suppliers), and

- substitution from competing ARBs based on contract pricing.

Implications for pricing projections

- If payer budgets tighten, losartan gains share as “cost anchor,” stabilizing volume but not price.

- If shortages hit certain ARBs more severely than losartan, losartan can see short-term demand spikes, temporarily supporting price.

What FDA regulatory status affects losartan supply and price (ANDAs, shortages, labeling, and recalls)?

Featured snippet:

- FDA-driven product availability events (shortages, recalls, manufacturing holds) can create short-term price spikes for specific NDCs, even in a generic market.

ANDA supply and labeling

- Each ANDA approval supports at least one NDC strength. More NDCs increase competition and reduce price stability risk.

- Label changes or manufacturing changes can alter which NDCs are preferred, affecting net price.

Shortage dynamics

Shortages are typically episodic. The price effect is:

- strongest for constrained strengths,

- weaker for widely stocked NDCs,

- short duration unless supply failures persist.

What generic entry risks exist for losartan from Paragraph IV challenges and biosimilar-style dynamics?

Featured snippet:

- Biosimilar frameworks do not apply to losartan; Paragraph IV and ANDA litigation is the relevant risk type, but for losartan pricing the market is already generic.

Paragraph IV litigation relevance

If any active Paragraph IV cases remain for specific patents or product formats, they can affect:

- timing of new generics,

- authorized generic sequencing,

- settlement-driven entry dates.

For pricing projections in a mature market, litigation primarily matters when it delays supply for key NDCs, creating temporary higher net prices.

What settlement agreements or authorized licensing deals affect losartan market entry and pricing?

Featured snippet:

- Settlement terms can delay or accelerate entry, but in a mature generic category the net effect is usually confined to specific strengths or formulations.

Where settlement impacts pricing

- Delayed generic entry for a small subset of NDCs can temporarily maintain higher contracted pricing.

- Accelerated entry can compress net price quickly once payers update formularies or preferred-NDC status.

Losartan price projections: base-case, upside, and downside scenarios for 12–36 months

Featured snippet:

- Base case: flat-to-down average net price with modest volatility; demand stable.

- Upside case: localized increases from supply constraints and contract readjustments.

- Downside case: new NDC entries and intensified competitive contracting drive further erosion.

Scenario assumptions (U.S. generic market)

- Continued multi-source competition and PBM contracting.

- No broad, category-wide supply failure.

- Any litigation impacts are NDC-specific and time-bounded.

Projection ranges (average net price, generic losartan tablets)

- Base case (12–36 months): -0% to -5% average net price drift, with most decline occurring in the early part of the horizon and flattening later.

- Upside case: +0% to +3% in periods of constrained supply for particular strengths or manufacturing outages.

- Downside case: -5% to -12% if multiple additional suppliers enter preferred NDCs or if PBMs re-optimize contracting toward the lowest-cost sources.

Combination products (losartan + HCTZ and other fixed-dose variants)

- Base case: -0% to -4% average net price drift, generally less steep than mono-therapy if fewer exact-combination competitors exist.

- Downside case: -4% to -10% if competitive penetration increases for key combinations.

- Upside case: +0% to +3% with similar shortage dynamics but less uniform across NDCs.

What volume drivers could change losartan revenue even if price declines?

Featured snippet:

- Volume is more sensitive to payer preference and switching than to pricing alone.

Key volume drivers:

- Guideline adherence: stable hypertension management demand.

- Class switching: from other ARBs based on formulary and contracting.

- Adherence and persistence: once patients stabilize, ARB persistence can be strong.

- Institutional formularies: dialysis/CKD populations can drive ARB usage patterns.

Revenue can hold up even as price declines if share shifts to cheaper ARBs and volume grows through broader payer coverage.

How do manufacturing and IP/IP barriers affect supply availability and price?

Featured snippet:

- In generic losartan, manufacturing capacity and regulatory status are primary determinants of short-term price volatility.

Manufacturing/IP barriers that matter operationally

- Bulk API supply continuity and DMF status stability

- Solid oral dosage (tablet) manufacturing consistency

- Compliance actions that remove NDCs from the market temporarily

- Capacity bottlenecks during peak demand or during competitive reallocation

Even without active patent barriers, operational constraints can move short-term pricing.

Key Takeaways

- Losartan is a mature generic-heavy ARB market where net pricing is dominated by multi-source competition and payer contracting.

- Over 12–36 months, expect flat-to-down net price for losartan tablets, with small localized volatility tied to NDC-specific supply constraints.

- Combination products (notably losartan fixed-dose combinations) can show less steep price erosion than mono-therapy, but remain contract-driven.

- Exclusivity and patent events are unlikely to create category-wide pricing discontinuities; the practical impact is NDC-specific and tied to entry timing, litigation, and supply disruptions.

FAQs

1) Will losartan prices fall further as more ANDAs are approved?

Most likely: any additional ANDA approvals in an already saturated market typically drive incremental net price erosion for affected strengths, not a structural break across all dosages.

2) What NDCs are most sensitive to losartan price spikes?

Strengths with fewer currently active suppliers, recent manufacturing issues, or tighter distributor inventory are most likely to show short-term net price increases.

3) How does losartan compare economically with ACE inhibitors like lisinopril?

ACE inhibitors are also generic and cost-competitive; payer preference often determines relative share, while losartan’s pricing typically follows its ARB-contract position rather than ACE cost.

4) Does Paragraph IV litigation materially affect losartan pricing today?

Only if it delays generic supply for key NDCs. In a broadly generic market, litigation effects are usually localized and time-bound.

5) Could drug shortages increase losartan revenue?

Yes, but primarily through temporary price uplift for constrained NDCs and share movement during shortage windows.

References

- FDA. “Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations.” U.S. Food and Drug Administration. (Accessed 2026).

- FDA. “Drugs@FDA.” U.S. Food and Drug Administration. (Accessed 2026).

- FDA. “Drug Shortages.” U.S. Food and Drug Administration. (Accessed 2026).

More… ↓