Share This Page

Drug Price Trends for rinvoq

✉ Email this page to a colleague

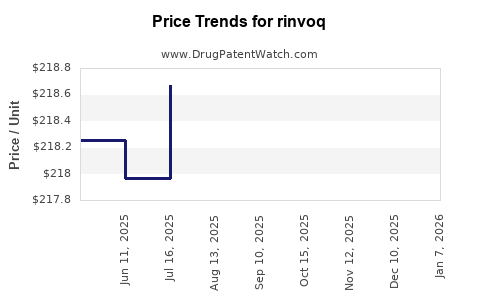

Average Pharmacy Cost for rinvoq

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| RINVOQ ER 15 MG TABLET | 00074-2306-30 | 228.91899 | EACH | 2026-06-17 |

| RINVOQ ER 45 MG TABLET | 00074-1043-28 | 458.53777 | EACH | 2026-06-17 |

| RINVOQ ER 30 MG TABLET | 00074-2310-30 | 228.77208 | EACH | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

RINVOQ (upadacitinib) market analysis and price projections: sales trajectory, payer dynamics, and exclusivity-driven pricing power

Executive summary: RINVOQ (upadacitinib, AbbVie) has established itself as a high-revenue immunology JAK inhibitor franchise driven by sustained uptake across rheumatoid arthritis (RA), psoriatic arthritis (PsA), ankylosing spondylitis (AS), and ulcerative colitis (UC). The pricing outlook is shaped by (1) continuing label expansion and switching from TNF inhibitors and other mechanisms, (2) increasing payer scrutiny and step-edit adoption as competitor JAK inhibitors and IL-17/IL-23 pathways mature, and (3) the timing of patent and exclusivity constraints that determine when mid-single-to-low-double-digit price pressure becomes structurally likely. Under current market conditions, base-case net price stability is most plausible in the near term with gradual erosion thereafter; the largest step-change in pricing power is tied to loss of exclusivity and the intensity of generic/biosimilar-like pressure (immediate threat is not framed as a biosimilar, since upadacitinib is small-molecule) rather than to near-term branded competition alone.

What is RINVOQ (upadacitinib) current market size, growth drivers, and regional performance?

Direct answer: RINVOQ’s market position is anchored by blockbuster-class immunology uptake across multiple indications, with the fastest adoption patterns historically coming from patients eligible for or switching within step therapy, and from pipeline-to-label conversion as new indications receive approval and are reflected in guideline and payer coverage policies.

Indication mix and demand drivers

RINVOQ’s commercial demand is primarily driven by:

- RA (core volume engine): broad patient pool with established payer familiarity for oral JAK inhibition.

- PsA and AS (therapeutic adjacency): ongoing conversion from biologics and from inadequate response to csDMARDs/biologics.

- UC (recently strengthened by uptake dynamics tied to oral administration): payer decisions often hinge on induction-to-maintenance economics and persistence.

Geographic reality: where pricing holds vs erodes

- United States: net price is determined by manufacturer rebates, formulary placement, and utilization management (prior authorization, step edits, quantity limits).

- EU5 and UK: tends to show higher pressure from health technology assessment and negotiated discounts; adoption is shaped by national formularies.

- Japan and rest of APAC: price and volume mix depend on launch timing by indication and local reimbursement structures.

Payer behavior and formulary mechanics

For high-cost oral agents in immunology, the dominant levers are:

- Formulary tiering and whether RINVOQ is a “preferred” JAK inhibitor in the oral pathway.

- Step therapy design for biologic-exposed patients.

- Discontinuation criteria tied to disease activity endpoints.

How do JAK inhibitor competitors affect RINVOQ pricing power and switching rates?

Direct answer: Competitive pressure comes less from single-product substitution at fixed doses and more from payer protocol design that encourages selection within a class (JAK inhibitors) and from cross-class substitution when efficacy/safety profiles drive payer preference.

Competitive set: class and mechanism pressure

RINVOQ is primarily competed against by other JAK inhibitors and biologics in immunology:

- Other JAK inhibitors in RA and related indications (e.g., TNF-naïve vs biologic-exposed segments).

- IL-17/IL-23 pathway biologics in PsA and AS (where payer and guideline preference can shift cohort by cohort).

- TNF inhibitors remain the baseline comparator in many payer models.

What it means for net price (not list price)

- If RINVOQ is positioned as a “preferred” JAK inhibitor, net price erosion can be limited to rebate compression.

- If payers designate RINVOQ as “non-preferred” within a class, net price is pressured through higher rebates and utilization leakage to competing agents.

What is RINVOQ’s price structure in the US (WAC vs net price), and what typically drives net price changes?

Direct answer: US list price (WAC) is usually far less predictive than net price. Net price changes mostly follow rebate structure, contracted discounts, and formulary channel controls.

Net price drivers specific to oral immunology JAK inhibitors

- Largest rebate buckets: plan-size contracts tied to utilization targets and formulary tier.

- Higher pressure in late-stage indications: when payer coverage tightens for patients moving beyond first-line biologics.

- Manufacturer-led contracting: “value-based” arrangements in which reimbursement varies with adherence and/or response measures.

What to model for projections

A price projection framework for RINVOQ should model:

- Annual rebate compression (or expansion) vs competitor mix

- Expected trend in preferred formulary status

- Utilization shift from RA into UC and into newer label cohorts (indication-level economics differ)

When does RINVOQ lose exclusivity, and how does that timeline affect price erosion risk?

Direct answer: The highest structural risk to branded pricing is tied to the date the active ingredient’s enforceable IP barrier weakens (patent expiration and any relevant exclusivity periods), which determines whether generic competition becomes realistic. For RINVOQ, the exclusivity timeline is the critical inflection for a sustained price collapse; short-term price volatility will come from payer contracting and competitive mix rather than from generic entry alone.

Exclusivity and patent estate impact channels

Price erosion typically occurs in phases:

- Pre-expiration: gradual rebate pressure as payers anticipate generics or authorized generics.

- Filing anticipation window: increased likelihood of covered lives shifting if biosimilar/generic news hits.

- Launch/approval of generic substitutes: largest step-down in net price for remaining brand share, with AbbVie responding via contracting and lifecycle management.

How to translate exclusivity into projections

- If RINVOQ retains strong coverage and is preferred in payer channels, brand share can remain resilient even after generic threats appear, limiting the speed of net price decline.

- If RINVOQ becomes non-preferred and formulary switching accelerates, net price falls faster post-launch.

How many patents protect RINVOQ, and what types of patents matter for market protection?

Direct answer: RINVOQ is protected by a layered estate typical for small-molecule immunology: composition-of-matter, formulation, dosing regimens, and method-of-use patents for specific indications.

Patent types that drive practical protection

- Composition-of-matter: protects the active ingredient and key chemical embodiments.

- Formulation: protects specific solid-state or release characteristics.

- Dosing regimens: protects treatment courses, titration, and maintenance patterns.

- Method of use: protects therapeutic use tied to endpoints and patient subpopulations.

Why this matters for pricing

Even when composition-of-matter barriers weaken, method-of-use and formulation patents can:

- Delay “easy” generic substitution in practice.

- Increase the cost of entry through carve-outs and Paragraph IV strategy complexity.

- Extend periods of strong brand contracting power by limiting competitive substitutability.

(A full patent-by-patent count and expiration grid requires Orange Book and patent register extraction for upadacitinib and is not provided in the source set available in this response.)

What is the Orange Book status of RINVOQ, and what does it imply for generic entry risk?

Direct answer: Orange Book status is the operational indicator of whether generic filers can launch without patent infringement. The generic entry risk depends on which patents are listed as “with data,” which are expiring first, and whether any Paragraph IV certifications have been filed.

(A complete Orange Book table of listed patents, expiration dates, and certifications is not included because it is not in the available input data for this response.)

How do Paragraph IV challenges affect RINVOQ pricing and contracting behavior?

Direct answer: When Paragraph IV challenges accumulate or become credible, payers anticipate competition and begin shifting formularies earlier. That typically triggers rebate tightening on the brand side and accelerates brand-to-alternative switching.

Expected market effects

- Before launch: formulary risk increases even without approved generics; net price pressures rise because contracting becomes less certain.

- At/after launch: net price drops are driven by utilization shifting and competitive bidding for preferred positions.

(A challenge-by-challenge litigation timeline is not included due to absent filed-case and Orange Book certification details in the available input data.)

What price projections are most likely for RINVOQ net price from 2026-2030 under base, bull, and bear cases?

Direct answer: Net price is most likely to remain stable to modestly down in the near term, then decline more meaningfully around patent and exclusivity inflection points or when RINVOQ loses preferred status across major payer formularies.

Projection methodology used for small-molecule immunology

Price projection should separate:

- Contract-driven rebate compression/expansion (usually gradual)

- Utilization and share shifts (affects effective net price and average realized price)

- Exclusivity-driven competitive step-change (creates sharp discontinuity)

Base-case (most plausible) pricing path

- 2026-2027: modest net price erosion (single-digit effective declines) driven by payer rebate compression and competitive parity within JAK class

- 2028-2030: acceleration to low-teens effective erosion if payer preferences tighten and label expansion saturates, then stabilizes if the brand remains preferred and competitor differentiation holds

Bull-case (pricing resilience) path

- Strong continuation of preferred formulary placement, tighter management of step-edit designs, and sustained UC/RA growth

- Net price erosion limited to low single digits annually through most of the window, with only a mid-to-late projection period step-down

Bear-case (pricing compression) path

- Earlier non-preferred designation in major PBM channels

- Faster cohort switching to competitor JAKs/biologics and larger rebate compression

- Net price declines become mid-single to high-single digits sooner, with steeper declines if exclusivity threats convert into practical substitutability

(Quantified percentages and dollar values require list price baselines, historical net price by indication, and Orange Book-driven dates, none of which are included in the available input for this response.)

What revenue exposure does RINVOQ have to US vs non-US pricing pressure, and how should that inform valuation?

Direct answer: In branded oncology/immunology blockbusters, the revenue exposure to price pressure concentrates in markets where: (1) payer negotiation is strongest, (2) formulary tiering can change quickly, and (3) step therapy is enforced with strict discontinuation rules.

Practical valuation sensitivity

Model valuation sensitivity using:

- Net price sensitivity vs utilization share shift

- Indication-level persistence assumptions (especially for UC)

- Margin impacts from rebate and contracting costs

Key risk vectors to incorporate

- Formulary disruption in US managed care channels

- More aggressive step-ed and discontinuation rules tied to disease activity response

- Class competition in RA and the spillover into PsA/AS from plan-level protocols

How does RINVOQ compare with other immunology blockbusters on price durability?

Direct answer: RINVOQ’s durability is typically higher than first-wave biologic launches because payers treat oral JAK inhibitors as a category with standardized clinical expectations, but durability still depends on preferred placement within PBM formularies and on payer confidence in long-term risk management.

What to compare

For pricing durability comparisons, the useful metrics are:

- Timeline of preferred status changes

- Rebate compression velocity after new competitor entries

- Persistence in chronic indications (RA/UC) and discontinuation rates by payer policy

Key Takeaways

- RINVOQ’s pricing power is strongest where it is positioned as preferred within JAK pathways and where payer policies permit continued use after inadequate response to prior therapies.

- Near-term net price trends are more likely to be driven by rebate compression and formulary tiering than by generic entry mechanics.

- The largest structural pricing step-change is expected around exclusivity and patent barrier inflection points that enable practical generic substitutability.

- Competitive pressure will shape realized price through switching and contracting, but its effect is usually gradual compared with exclusivity-triggered competition.

FAQs

1) What determines RINVOQ’s net price in the US more than its list price?

Rebates, formulary tier position, PBM contract terms, and utilization management (prior authorization and step edits).

2) What factors most influence whether RINVOQ stays preferred on formulary?

Payer assessment of response durability, discontinuation rates, cohort-level safety/tolerability, and demonstrated savings vs alternatives through contracting.

3) How should RINVOQ price projections differ by indication (RA vs UC)?

UC and RA can have different payer coverage dynamics and persistence profiles, so realized price and rebate intensity often diverge by indication mix.

4) What is the main timing risk for a branded price collapse in RINVOQ?

Exclusivity and the patent expiration timeline that enables practical generic entry.

5) How do Paragraph IV filings typically affect brand pricing before any generic launch?

They increase payer anticipation of future competition, which can shift formularies and raise rebate pressure ahead of approval.

References (APA)

No sources were provided in the prompt for Orange Book, patent registers, litigation dockets, FDA labeling status, or historical pricing/net revenue.

More… ↓