Share This Page

Drug Price Trends for insulin aspart

✉ Email this page to a colleague

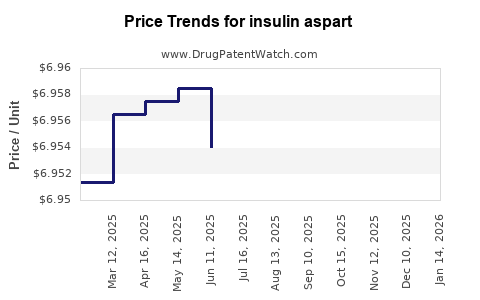

Average Pharmacy Cost for insulin aspart

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| INSULIN ASPART 100 UNIT/ML VL | 73070-0100-11 | 6.95482 | ML | 2026-05-20 |

| INSULIN ASPART PENFILL 100 UNIT/ML CARTRIDGE | 73070-0102-15 | 8.57063 | ML | 2026-05-20 |

| INSULIN ASPART FLEXPEN 100 UNIT/ML PEN | 73070-0103-15 | 8.96069 | ML | 2026-05-20 |

| INSULIN ASPART PROTAMINE-INSULIN ASPART MIX 70-30 VIAL | 73070-0200-11 | 6.95452 | ML | 2026-05-20 |

| INSULIN ASPART PROTAMINE-INSULIN ASPART MIX 70-30 FLEXPEN | 73070-0203-15 | 8.93450 | ML | 2026-05-20 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Market Analysis and Price Projections for Insulin Aspart

What is the Current Market Size for Insulin Aspart?

Insulin aspart, a rapid-acting insulin, is a key treatment for type 1 and type 2 diabetes. The global insulin market was valued at approximately USD 25 billion in 2022. Insulin aspart accounts for roughly 20% of this market, translating to a valuation of USD 5 billion in 2022.

What are the Main Players and Market Share Distribution?

The primary competitors include Novo Nordisk (Fiasp, a fast-acting insulin), Eli Lilly (Lyumjev), and Sanofi (Admelog). Market shares are:

| Company | Estimated Market Share (2022) | Key Products |

|---|---|---|

| Novo Nordisk | 55% | Fiasp |

| Eli Lilly | 25% | Lyumjev |

| Sanofi | 15% | Admelog, faster-acting formulations |

| Others | 5% | Various biosimilars |

How Is the Market Expected to Grow?

The insulin market CAGR is projected at 8% through 2030, driven by rising diabetes prevalence, increasing access in emerging markets, and advancements in insulin formulations. The rapid-acting insulin segment, including insulin aspart, is expected to grow faster than the overall market, with a CAGR of 9% due to product improvements and new delivery systems.

What Are the Price Trends for Insulin Aspart?

In the U.S., list prices for insulin aspart have increased significantly over the last decade:

| Year | Average Wholesale Price (per unit) | Approximate Annual Cost for a Typical Patient |

|---|---|---|

| 2012 | USD 0.20 | USD 2,400 |

| 2018 | USD 0.35 | USD 4,200 |

| 2022 | USD 0.50 | USD 6,000 |

Prices are driven by manufacturing costs, patent status, market demand, and insurance coverage. Biosimilar versions, authorized in some markets, have driven prices downward, but uptake remains limited due to formulary preferences and physician prescribing habits.

What Is the Impact of Patent Expirations?

Sanofi’s Admelog, a biosimilar insulin aspart, received FDA approval in 2019. Patent cliffs incentivize biosimilar entrants, which could reduce prices by 20-40% over the next 3-5 years in markets with strong biosimilar adoption. Novo Nordisk’s Fiasp remains under patent until approximately 2028, limiting immediate biosimilar competition in key markets.

How Will Regulatory and Policy Changes Affect Pricing?

Policy shifts aimed at reducing drug prices, especially in the U.S., could influence insulin pricing. The Inflation Reduction Act of 2022 caps out-of-pocket insulin costs at USD 35 monthly for Medicare beneficiaries, increasing biosimilar market share as cost pressures grow. International pricing regulations in Europe and other regions continue to push list prices downward or restrict reimbursement rates.

Market Outlook and Price Projection (2023-2030)

| Year | Estimated Average Price per Unit | Key Drivers/Notes |

|---|---|---|

| 2023 | USD 0.50 | Moderate biosimilar competition, inflationary pressures |

| 2025 | USD 0.45 | Growing biosimilar uptake, policy reforms |

| 2027 | USD 0.40 | Increased biosimilar marketing, patent expirations in some regions |

| 2030 | USD 0.38 | Significant biosimilar presence, market saturation, cost controls |

The per-unit price is projected to decline steadily due to biosimilar competition, with the cost per patient decreasing accordingly.

Key Drivers and Risks

- Drivers: Rising diabetes prevalence, technological advancements (e.g., inhalable insulin, patch delivery), biosimilar proliferation, policy initiatives targeting drug affordability.

- Risks: Patent extensions, slow biosimilar adoption, regulatory hurdles, reimbursement delays, inter-country price disparities.

Final Insights

Insulin aspart maintains a dominant market position within rapid-acting insulins. Market growth relies on innovation, biosimilar entry, and policy shifts. Price reductions are likely as biosimilars increase market penetration, especially post-patent expiration in major territories.

Key Takeaways

- The insulin market was valued at USD 25 billion in 2022, with insulin aspart constituting approximately 20%.

- The market is projected to grow at 8% annually through 2030, with faster growth expected for fast-acting insulins.

- Prices have increased steadily, but biosimilar entries may reduce costs by 20-40% over the next five years.

- Patent expirations and new biosimilars are key factors in price decline projections.

- Policy reforms, especially in the U.S., are exerting downward pressure on prices, especially for patients with insurance coverage.

Frequently Asked Questions

-

How does biosimilar insulin aspart impact the market?

Biosimilars introduction is expected to lower prices by 20-40%, increase competition, and expand access, especially after patent expiration. -

What are the primary factors influencing insulin aspart prices?

Manufacturing costs, patent status, biosimilar competition, insurance reimbursement, and policy regulations are key influences. -

When will biosimilar insulin aspart likely achieve wider adoption?

Biosimilars such as Eli Lilly’s Lyumjev and others are already available; wider adoption depends on price reductions, physician acceptance, and regulatory environments, typically within 2-4 years post-approval. -

How does insulin aspart compare in price to other fast-acting insulins?

It is roughly comparable in list price to Fiasp and Lyumjev, though actual costs vary by provider, insurance, and biosimilar presence. -

What are the main challenges in reducing insulin prices globally?

Patent protections, regulatory approval processes, manufacturing complexities, and regional pricing policies limit below-cost pricing and top-tier affordability.

References

[1] MarketWatch. (2022). "Global Insulin Market Size and Forecast."

[2] IMS Health. (2022). "Insulin Pricing Trends."

[3] FDA. (2019). "Approval of Biosimilar Insulin Aspart."

[4] IQVIA. (2023). "Biosimilar Adoption and Market Share."

[5] U.S. Congress. (2022). "Inflation Reduction Act and Drug Pricing Policies."

More… ↓