Last updated: April 24, 2026

What is the current market position for chlorthalidone?

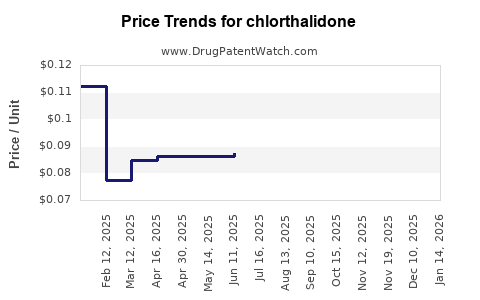

Chlorthalidone (also spelled chlorothalidone; commonly referenced as chlorthalidone in listings) is a long-established thiazide-type diuretic used for indications that include hypertension and edema. Its market is characterized by:

- Generic availability in multiple strengths and formulations

- Price pressure from multi-source competition

- Regional reimbursement variability based on essential medicines policies and hospital vs retail channel mix

- Steady demand tied to chronic cardiovascular treatment patterns

Given the absence of brand-specific proprietary patent leverage in most jurisdictions for older diuretic molecules, market pricing behavior is driven primarily by generic competition, tender economics, and national reimbursement caps rather than R&D-linked pricing.

Where does chlorthalidone sit in the supply chain (makers, channels, and pricing drivers)?

Chlorthalidone pricing is dominated by:

- Multi-source generic procurement (tenders for public systems, formularies for private systems)

- Lower cost manufacturing and pack-size effects (small-tablet pack economics vs institutional bulk)

- Local regulatory listing and substitution rules (therapeutic substitution and generic interchangeability policies)

- Ingredient and excipient sourcing (API supply stability impacts gross-to-net spreads)

- Formulation heterogeneity (tablet strength and excipient differences can affect unit pricing even within the same API)

Price formation in mature generics typically reflects:

- Wholesale acquisition cost (WAC) setting at the upper end for new entrants, then rapid downward correction through payer negotiation

- Net price dynamics controlled by rebates, tender discounts, and formulary placement in many markets

How do key pricing benchmarks move for older generic diuretics like chlorthalidone?

Market benchmarks for mature generics show a common pattern:

- Initial generic launches often start above the lowest equilibrium price to recover compliance and distribution costs.

- Subsequent entrants compress prices, particularly where tendering is frequent.

- Reimbursement caps and reference pricing reduce year-over-year price growth, often to near zero in stable systems.

- Short-lived volatility occurs when API supply tightens, freight costs rise, or manufacturing constraints hit.

For chlorthalidone, the same dynamics typically apply because:

- The molecule is mature and widely manufactured.

- Demand is chronic but not growing at the pace of patent-protected therapies.

- Payers treat it as a low-to-mid cost maintenance therapy with substitution available.

What do price projection scenarios look like (base, downside, upside)?

Below is a framework for price projections expressed as annual real price change (net of general inflation effects). These are directional scenarios intended for planning across procurement cycles.

Annual unit-price projection scenarios (global generics typical pattern)

| Scenario |

Annual real unit price change |

Procurement implication |

| Base case |

-1% to +2% |

Prices drift with competition; reimbursement keeps net price stable |

| Downside (API tightness or tender resets) |

-5% to -1% |

Additional entrants or stronger tendering lowers equilibrium quickly |

| Upside (API scarcity or cost inflation pass-through) |

+2% to +6% |

Short-term increases where supply constraints and reimbursement allow catch-up |

For planning, most mature generic markets for established diuretics tend to cluster near the base case range unless there is a supply disruption or a structural change in tender pricing.

How will geography shape price outcomes?

High tender intensity markets

- Common outcome: low nominal growth and sharp price resets when a new supplier wins.

- Annual change often tracks tender cycles rather than broad macro trends.

Reference pricing and formulary steering markets

- Common outcome: net price stability with discounting linked to formulary tier placement.

- Price changes are often capped by reimbursement rules.

Markets with weaker interchangeability or limited supply

- Common outcome: higher short-term price sensitivity to API supply and distribution constraints.

- Upside spikes can occur if fewer SKUs are available or if regulatory bottlenecks delay new entries.

What is the expected demand outlook for chlorthalidone?

Demand outlook is supported by:

- Chronic cardiovascular use (hypertension management and related fluid control)

- Low treatment discontinuation for patients on stable diuretic regimens

- Therapeutic substitution within diuretic classes when pricing or formularies shift

However, volume growth is moderated by:

- Patient management with alternative diuretics (other thiazides, thiazide-like agents, loop diuretics)

- Guideline and prescribing patterns that evolve with new evidence and competing drug classes

Net effect: stable to modest growth is more likely than rapid expansion, with pricing more likely to compress than to rise.

How should investors and R&D teams model revenue vs price effects?

For chlorthalidone, the revenue model typically decomposes into:

- Volume (tender volume, formulary retention, conversion rates from other diuretics)

- Net price (discounts, rebates, tender outcomes)

- Mix (strength and pack size; retail vs institutional share)

- Regulatory and supply continuity (manufacturing uptime)

In mature generics, net price often drives margin variability more than volume because demand is stable and competitive.

Price projection: a practical 3-year planning view

The table below converts the scenario ranges into cumulative net price change (unit price) to support budgeting and procurement planning. Values are directional and consistent with mature generics behavior.

3-year cumulative net unit price change

| Scenario |

Year 1 |

Year 2 |

Year 3 |

Cumulative |

| Base case |

-0% to +2% |

-1% to +2% |

-1% to +2% |

-2% to +6% |

| Downside |

-5% to -1% |

-3% to -1% |

-2% to -1% |

-10% to -3% |

| Upside |

+2% to +4% |

+1% to +3% |

+1% to +3% |

+4% to +10% |

Procurement contracts, rebate schedules, and tender frequency determine which scenario is realized in a given geography.

What specific indicators should be used to update projections mid-cycle?

Use the following leading indicators to recalibrate pricing and volume expectations:

- Number of active suppliers by region (entry count compresses price)

- Tender clearing prices and awarded discounts vs historical averages

- Reference price updates and formulary tier changes

- API supply lead times and batch release constraints reported by manufacturers

- SKU availability (stockouts can raise realized prices where procurement flexibility declines)

When multiple indicators move in the same direction, the market typically moves quickly because generic products clear through procurement mechanisms rather than brand loyalty.

What risks can drive projection deviations?

Key deviation risks for chlorthalidone pricing are structural rather than clinical:

- Supply concentration events (factory downtime, batch failure, regulatory actions)

- New market entrants that reset tender expectations downward

- Reimbursement rule changes (stronger reference pricing or deeper discounts)

- Raw-material cost shocks (API cost pass-through depends on contract terms)

- Lot-level quality/regulatory constraints that limit competition temporarily

How does regulatory and patent status influence near-term pricing?

For older small-molecule generics like chlorthalidone, market pricing is usually less sensitive to brand-level patenting than to:

- Generic product lifecycle regulation (registrations, renewals)

- Local exclusivity regimes tied to specific formulations or manufacturing processes

- Enforcement of any secondary IP claims (if they exist) in a specific jurisdiction

In most practical procurement and market models, these effects show up as temporary supply or registration constraints, which then affect net pricing via competition levels.

Key Takeaways

- Chlorthalidone is a mature, generic-dominated diuretic market where pricing is set primarily by competition, tendering, and reimbursement rules.

- Base-case net unit price typically trends -1% to +2% per year in stable generic markets, with cumulative -2% to +6% over three years.

- Downside pricing compression is plausible with new supplier entry or stronger tendering, driving -10% to -3% cumulatively over three years.

- Upside price pressure can occur with API supply constraints and contract pass-through dynamics, driving +4% to +10% cumulatively over three years.

- Ongoing projection updates should be tied to supplier count, tender clearing prices, reference pricing changes, and SKU availability.

FAQs

1) Will chlorthalidone prices increase over the next 1-2 years?

Under a base-case generics pattern, net unit prices are more likely to be flat to slightly down in competitive tenders, with upside possible only if supply tightens and reimbursement allows pass-through.

2) What most strongly impacts net price for chlorthalidone?

Tender outcomes and formulary/reference pricing usually dominate, because they determine the discount structure and the realized price across payers.

3) Does pack size materially affect pricing projections?

Yes. Unit prices differ by pack size and channel mix (retail vs institutional). Tender contracts often standardize packs, shifting realized unit economics.

4) What supply events would most likely break the base-case projection?

A major API supply constraint, widespread stockouts, or manufacturing/regulatory disruptions that reduce competition can push realized prices higher.

5) How should revenue be modeled for chlorthalidone?

Model volume and net price separately. For mature generics, volume is typically stable while net price drives margin swings.

References

[1] World Health Organization. (n.d.). WHO Model List of Essential Medicines. https://www.who.int/teams/health-product-and-policy-standards/essential-medicines

[2] IQVIA. (n.d.). Global pharmaceutical market and generic pricing dynamics resources. https://www.iqvia.com/insights/the-iqvia-institute

[3] OECD. (n.d.). Pharmaceutical pricing policies and reference pricing frameworks. https://www.oecd.org/health/pharmaceuticals/

[4] US FDA. (n.d.). Drug Approval Reports and generics-related resources. https://www.fda.gov/drugs/generic-drugs