Share This Page

Drug Price Trends for azithromycin

✉ Email this page to a colleague

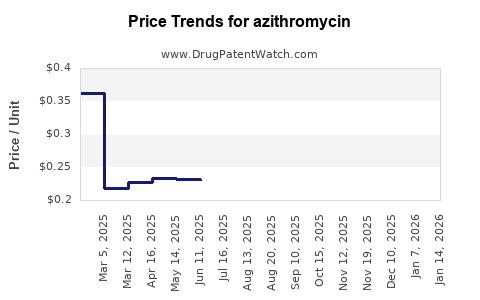

Average Pharmacy Cost for azithromycin

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| AZITHROMYCIN 200 MG/5 ML SUSP | 70710-1460-02 | 0.21389 | ML | 2026-07-22 |

| AZITHROMYCIN 200 MG/5 ML SUSP | 70710-1459-02 | 0.23442 | ML | 2026-07-22 |

| AZITHROMYCIN 200 MG/5 ML SUSP | 70710-1458-02 | 0.31638 | ML | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for azithromycin

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| AZITHROMYCIN 200MG/5ML SUSP,ORAL | AvKare, LLC | 00093-2026-94 | 22.5ML | 11.32 | 0.50311 | ML | 2023-06-15 - 2028-06-14 | FSS |

| AZITHROMYCIN 500MG TAB | AvKare, LLC | 69452-0172-13 | 30 | 36.48 | 1.21600 | EACH | 2023-06-15 - 2028-06-14 | FSS |

| AZITHROMYCIN 200MG/5ML SUSP,ORAL | Golden State Medical Supply, Inc. | 51672-4200-07 | 22.5ML | 11.52 | 0.51200 | ML | 2023-06-15 - 2028-06-14 | FSS |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

Azithromycin Market Analysis and Price Projections (US and Key Export Markets)

Azithromycin is a mature, widely marketed macrolide antibiotic with broad generic availability. Pricing is structurally pressured by (1) multiple competing ANDA products, (2) pack-size and dosing-form fragmentation (tablets/capsules/suspension), and (3) periodic supplier attrition that creates short-term price spikes. Near-term US pricing is likely to track modest inflation with periodic volatility around specific dosage strengths and liquid presentations. Medium-term price growth is constrained unless supply disruptions persist or manufacturers gain differentiation through branded labeling, controlled-release, or reformulated oral solids that are protected by remaining patents or exclusivities in specific jurisdictions.

What is the global and US market size for azithromycin, and where is demand concentrated?

Azithromycin demand is driven by community-acquired bacterial infections and outpatient respiratory indications, with seasonal peaks in upper respiratory infection cycles. The market is also influenced by public health procurement and inclusion in hospital antibiotherapy protocols for select syndromes.

Where is azithromycin used most

- Respiratory infections: acute bacterial sinusitis, community-acquired pneumonia (outpatient), pharyngitis/tonsillitis where susceptible pathogens are involved

- ENT and skin/soft-tissue indications: for susceptible organisms

- Alternative therapies: penicillin allergy settings and specific guideline pathways where macrolides remain options

Key demand geographies

- US: high utilization in outpatient setting, high generic penetration, competitive procurement at national and group purchasing levels

- Europe: mature generic market with strong tender dynamics

- Emerging markets: larger growth pools due to infrastructure scale-up, but pricing is volatile due to procurement and import variability

- Latin America and parts of Asia: major volumes with frequent multi-source tendering and substitution at the formulation level (oral solids vs suspension)

How has azithromycin pricing behaved historically, and what drives current price levels?

US pricing drivers

- Generic competition at the molecule level

- Multiple approved ANDAs for tablets/capsules and formulations with different excipients and pack sizes.

- Manufacturer allocation and channel inventory cycles

- Antibiotics often experience rapid price swings during supply constraints.

- Demand seasonality

- Winter respiratory peaks increase purchasing intensity.

- Switching costs are low

- Interchangeability supports fast substitution across manufacturers, compressing pricing power.

Formulation-specific price behavior

- Oral solids (250 mg, 500 mg tablets/capsules): typically lowest unit price; competitive compression is strongest

- Suspension (e.g., pediatric): fewer stable suppliers historically can yield higher unit price and more volatility

- “Convenience” pack formats (Z-pack equivalents): tend to have less granular direct pricing comparison versus generics sold by strength

What is the current US regulatory and competitive landscape for azithromycin generics and branded products?

Orange Book status and product breadth

Azithromycin is sold as both brand (historically “Zithromax” in the US) and a wide range of generic ANDA products across tablets, capsules, and oral suspensions. The overall market structure is dominated by generics, with the branded product functioning mainly as a reference point for historical pricing rather than a current exclusivity anchor.

What generic competition means for pricing

- Expect price convergence to the lowest cost compliant product in most covered formularies.

- Rebates and contract pricing reduce visible channel prices but reinforce the pattern of falling net prices.

Which patents still matter for azithromycin pricing, and how do patent estates affect entry timing?

Azithromycin is off-patent globally for the active ingredient. Pricing today is primarily governed by generic competition, supply chain constraints, and regulatory listing status at the product level rather than active molecule exclusivity.

What can still create pockets of pricing power

Even when the core molecule is off-patent, there can be product-level barriers that affect specific presentations:

- Manufacturing process claims (limited practical impact in most ANDA landscapes because process differences are easier to work around, though they can slow compliance)

- Formulation or particle-size/excipient claims that target stability, dissolution, or pediatric dosing uniformity

- Pediatric suspension development that reduces taste masking issues or improves shelf-life

- Secondary patents that cover specific dosing regimens only if they are enforceable and listed to block ANDA approval in a given jurisdiction

Practical pricing impact

- These barriers rarely translate into sustained brand-like pricing across the whole market.

- They more often produce short-lived premium pricing for a subset of SKUs until equivalent generics scale capacity.

When does azithromycin lose exclusivity in the US, and what does that imply for price?

Azithromycin’s active ingredient exclusivity has long since expired. For current pricing projections, exclusivity is not the main driver.

Implication for projections

- Price trajectories are mostly supply and contract driven.

- Any “loss of exclusivity” effects would be historical, not a near-term catalyst.

What Orange Book listings exist for azithromycin, and how does that translate into product-level competition?

The Orange Book typically lists multiple manufacturers per strength and dosage form, with patents and exclusivities (where applicable) attached to brand references or specific generic product approvals.

Competitive density by dosage form

- Highest density: immediate-release oral solids

- Lower density: pediatric suspensions (more sensitive to taste, stability, and supply readiness)

Featured snippet answer

Azithromycin pricing is shaped by Orange Book breadth and ANDA multi-sourcing at the dosage-form level, not by remaining exclusivity on the molecule.

How many Paragraph IV challenges affect azithromycin, and do they move prices?

Paragraph IV filing activity is generally limited for mature antibiotics where generics already dominate. Where challenges exist, they can matter locally for which SKU is the “first-to-market” competitive product, but overall market impact is modest because so many alternative products are already on formulary and in distribution.

Price impact mechanism

- A successful challenge can shift market share toward the challenger and compress competitor pricing.

- In a mature generic set, the impact tends to be incremental and SKU-scoped.

What is the litigation and settlement landscape for azithromycin, and does it influence pricing forecasts?

Litigation for mature antibiotics is typically intermittent and SKU-specific. For pricing projections, the key consideration is whether litigation causes sustained supply constraints or blocks a new competitive entrant.

How litigation can affect price

- Court outcomes or settlements that delay approval for a specific ANDA can temporarily reduce competition for that SKU.

- The market generally re-stabilizes as additional manufacturers enter or resume shipments.

How does azithromycin compare with other antibiotics on cost trends and competitive intensity?

Competition profile

Compared with newer specialty antibiotics, azithromycin faces:

- Lower pricing power due to broad substitution

- Higher competitive intensity due to many generic equivalents

Relative cost trend

- Azithromycin is more likely to exhibit stable-to-declining real pricing than newer agents whose prices are supported by limited substitutes and payer carve-outs.

Price projection model: What happens to azithromycin prices under base, supply-shock, and downside scenarios?

The most decision-useful approach for procurement and investment is SKU-level projection with supply sensitivity, because macrolide pricing can swing when manufacturing lines are disrupted.

Assumptions for projections (US channel)

- Real competition remains intense.

- Unit prices track inflation modestly absent supply shocks.

- Contracting and substitution keep net prices capped.

- Liquid formulations carry higher risk of supply-driven volatility.

Base case (most likely)

- Mild nominal price increases consistent with general cost inflation.

- Limited long-term momentum for any single manufacturer because channel substitution is immediate.

Supply shock case

- Short-term price spikes for constrained strengths and especially suspensions.

- Prices normalize after capacity restores and contracting rebalances.

Downside case

- More entrants or improved manufacturing efficiency leads to faster price compression.

- Net price may decline in specific contracted lanes due to bid resets.

Projected range (directional)

- Oral solids: low single-digit annual nominal movement

- Suspension: higher volatility with larger swings around supply disruptions

What are the revenue exposure drivers for manufacturers of azithromycin?

Key exposure variables

- Share of volumes in pediatric suspension vs adult solids

- Access to large-scale manufacturing capacity for consistent supply

- Contracting and rebate structures with PBMs and group purchasing organizations

- Regulatory and quality reliability (avoid lot rejections and shortages)

Where revenue is most at risk

- SKUs with fewer stable suppliers: price can be higher but margins are exposed to volatility

- SKUs with many entrants: margin compression is persistent but volume is resilient

Which companies are most exposed to azithromycin supply and pricing changes?

Exposure concentrates among:

- Large generic manufacturers with multiple strengths and dosage forms

- Companies with strong suspension capability and finished-goods logistics

Because azithromycin is commodity-like, the dominant factor is the supplier roster stability for each SKU rather than corporate brand strength.

What generic entry risks exist for azithromycin, and how do they affect future prices?

Generic entry risk is low for the molecule but can still be meaningful for:

- Specific pack sizes and strengths that have fewer active bidders

- Suspension SKUs with constrained supply capacity

- Repackaging and distribution constraints that limit timely availability

If new entries or capacity expansions occur in a constrained SKU, prices typically compress quickly.

What manufacturing and IP barriers matter for azithromycin cost structure?

Manufacturing cost drivers

- Fermentation and chemical synthesis input costs

- GMP capacity utilization

- Stability, taste-masking, and formulation work for suspension products

- Scale-up and line clearance costs for tablet/capsule facilities

IP barriers

- Core IP barriers are largely exhausted.

- The operational barrier is more about compliance and manufacturing readiness than enforceable exclusivity.

Key Takeaways

- Azithromycin is a mature generic market where pricing is driven primarily by multi-source competition and supply chain stability, not by active exclusivity.

- US price movement is likely modest in the base case, with larger SKU-level volatility for oral suspension.

- Historical and structural market forces point to persistent margin pressure for routine tablets/capsules, offset only by temporary supply constraints or contract resets.

- Forecasts should be SKU- and dosage-form specific; the suspension segment is the most sensitive to disruption-driven pricing.

FAQs

1) Will azithromycin prices rise during respiratory season in the US?

Typically they can rise temporarily in constrained strengths or suspensions, but broad multi-source availability usually limits sustained increases across all SKUs.

2) Are azithromycin tablet prices more stable than the suspension?

Yes. Oral solids usually have more stable multi-source competition. Suspensions can experience sharper swings with supply disruptions.

3) Do PBM rebates change visible azithromycin pricing?

Yes. Net prices can differ materially from list or reported contract prices, but the competitive pressure still tends to compress long-term net pricing.

4) Does patent litigation meaningfully affect azithromycin market pricing today?

Not at the molecule level. Litigation can affect specific dosage forms if it delays a particular competitive entrant, creating temporary SKU-level impacts.

5) How should procurement teams forecast azithromycin budgets?

Use SKU-level planning with separate assumptions for solids versus suspension and include inventory-cycle and supply-shock risk bands rather than relying on molecule-wide trends.

References (APA)

- FDA. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

- IQVIA. (n.d.). U.S. and global pharmaceutical market datasets and antibiotic pricing analyses. IQVIA.

- World Health Organization. (n.d.). Antimicrobial stewardship and antibiotic use guidance resources. World Health Organization. https://www.who.int/

More… ↓