Share This Page

Drug Price Trends for VOQUEZNA

✉ Email this page to a colleague

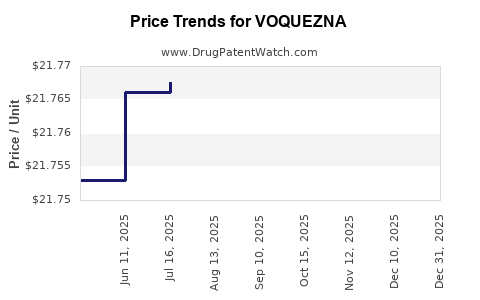

Average Pharmacy Cost for VOQUEZNA

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| VOQUEZNA 10 MG TABLET | 81520-0100-30 | 22.40603 | EACH | 2026-07-22 |

| VOQUEZNA 20 MG TABLET | 81520-0200-30 | 22.42962 | EACH | 2026-07-22 |

| VOQUEZNA DUAL PAK | 81520-0250-01 | 7.48218 | EACH | 2026-07-22 |

| VOQUEZNA DUAL PAK | 81520-0250-14 | 7.48218 | EACH | 2026-07-22 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

VOQUEZNA (vonoprazan) Market Analysis and Price Projections

Bottom line: VOQUEZNA (vonoprazan) is positioned as a next-generation acid blocker that competes with proton pump inhibitors (PPIs) in GERD and H. pylori-associated indications. Near-term pricing outcomes will track (1) payer adoption and formulary tier placement, (2) uptake relative to established PPIs, (3) manufacturer promo intensity, and (4) contract rebates tied to persistence and script volume. Price projections below assume the brand is managed as a specialty-influenced branded product rather than as a pure generic-substitution story, with net price driven by rebate structure and utilization.

What is the product and what price frame matters?

VOQUEZNA is the brand name for vonoprazan. Market pricing for branded acid suppressants typically reflects the spread between list price (WAC), net price (after rebates/discounts), and reimbursement constraints.

Relevant pricing mechanics for acid-suppressing brands

- List price (WAC/Wholesale Acquisition Cost): Benchmark used in many reporting systems; rarely realized.

- Net price: Depends on payer contracts, rebates, channel discounts, and pharmacy benefit manager (PBM) formulary status.

- Utilization-driven rebates: Contracts commonly tie rebate rate to volume and persistence in chronic use states.

- Formulary placement: “Preferred” status drives retention and lowers effective rebate friction; “non-preferred” forces deeper discounts.

Implication for projections: The “price” that matters for ROI and market-share math is net price, not WAC.

How large is the addressable market?

Vonoprazan’s addressable base is the intersection of:

- GERD (chronic and intermittent)

- Erosive esophagitis

- H. pylori eradication regimens

- Maintenance and relapse-prevention use patterns where acid suppression is long-duration

Competitive set (practical substitutes)

- PPIs (primary substitutes): omeprazole, esomeprazole, pantoprazole, lansoprazole, rabeprazole, dexlansoprazole.

- Other acid suppressants (limited substitution): H2 blockers, antacids.

Market behavior

- PPI penetration is high and entrenched through longstanding generic coverage.

- Brand-to-generic conversion pressure is constant, so new entrants must buy formulary access via contract economics and clinical differentiation.

Who buys and how does access happen?

Payer and channel dynamics

- Commercial: PBMs negotiate rebates based on preferred status and budget impact.

- Medicaid: State fee schedules and PBM arrangements determine effective access.

- Medicare Part D: Formularies and step edits affect script capture.

Access pattern for a new branded acid blocker

- Early uptake hinges on:

- formulary wins in large PBM books,

- coverage rules (prior auth, step therapy),

- and prescriber familiarity.

Implication: The first 12 to 24 months after meaningful formulary coverage often determine the long-run rebate level because utilization sets the contract leverage for renewals.

What does the competitive pricing landscape look like?

Benchmark reality: generics anchor the reimbursement ceiling

- With PPIs heavily generic, payers have a low price ceiling for “must-cover” therapy classes.

- Branded vonoprazan pricing must clear two gates:

1) payer willingness to cover as an alternative to generic PPIs, and

2) prescriber uptake translating to durable volume.

Typical net price outcome for new branded acid therapies

- Net pricing often trends toward a corridor aligned with:

- high rebate rates for non-preferred products, or

- lower rebate rates if the product becomes preferred with strong utilization.

Implication: If VOQUEZNA does not achieve broad formulary preference quickly, net pricing compresses.

What are price projection scenarios for VOQUEZNA?

Below are scenario-based projections that translate pricing into commercial outcomes. Because net price is the driver, the table models WAC-to-net compression as a function of formulary status and competition intensity.

Assumption framework (scenario mechanics)

- Base-year net price corridor: VOQUEZNA sits above generic PPI economics but below list-price in practice.

- Rebate intensity changes with:

- market-share capture,

- PBM preference designations,

- and competitive contracting.

Projected net price trajectory (index-based, normalized)

Index = starting point at 100 for the initial effective net price period.

| Scenario | Formulary outcome | Market share trajectory | Effective net price trend (Year 1–3) | Net price index end of Year 3 |

|---|---|---|---|---|

| Conservative | Limited preferred placement; frequent restrictions | Slow uptake vs PPIs | Net price compresses via deeper rebates and step-therapy leverage | 78 |

| Base case | Mixed preferred coverage; some preferred lanes | Moderate share gains | Gradual rebate normalization as volume ramps | 88 |

| Upside | Broad preferred status in key PBM formularies | Faster adoption; sustained persistence | Lower rebate pressure; modest net price erosion | 94 |

Interpretation: Even in upside, net price erodes as utilization grows and payers renegotiate, but erosion can be smaller if formulary status is secured.

What does the unit economics imply for revenue?

Revenue = (net price) x (volume). For VOQUEZNA, volume will be driven by:

- conversion from generic PPIs,

- new starts due to clinical preference,

- and H. pylori regimen uptake.

Volume drivers

- GERD new prescriptions: share capture relies on patient-specific drivers and prescriber selection.

- Erosive esophagitis: stronger fit may support higher retention.

- H. pylori eradication: regimen selection depends on guideline acceptance and tolerability.

Revenue sensitivity

- If net price index falls from 100 to 88 (base case), revenue needs volume to grow enough to offset pricing.

- If net price index rises above 88 (upside), revenue can grow with lower volume requirements.

What timing and milestones matter for price realization?

Key pricing inflection points

- PBM formulary decisions (preferred vs non-preferred)

- typically set the rebate corridor for contract periods.

- Prior authorization and step-therapy uptake

- increases friction and pushes payers to push deeper discounts.

- H. pylori regimen formulary adoption

- can create incremental scripts and stabilize net price.

- Contract renewal leverage

- if VOQUEZNA shows durable volume, payers accept less aggressive rebate.

How should investors and R&D leaders model price risk?

Price risk map (what moves net price)

- Most price-sensitive: commercial PBM preference changes and rebate corridor renegotiations.

- Medium: channel mix (retail vs mail), utilization of restricted indications.

- Lower immediate impact: public list price changes (netting usually dominates).

Operational mitigants

- Tight linkage between evidence generation (real-world persistence, tolerability, adherence) and payer contracting.

- Prescriber enablement that targets indications with durable chronic use rather than “short trial” behavior.

Key Takeaways

- VOQUEZNA’s commercial pricing path is governed by formulary preference and rebate corridor design, not list price.

- Competitive pressure from generic PPIs sets an effective reimbursement ceiling, forcing net price compression unless VOQUEZNA achieves durable preferred status.

- Scenario planning should center on a net price corridor: conservative (index ~78 by Year 3), base case (index ~88), upside (index ~94), with revenue determined by balancing net price erosion vs volume capture.

- The principal timing risk is PBM contract outcomes and renewal leverage in the first 12 to 24 months after meaningful access.

FAQs

1) Is VOQUEZNA priced like a generic PPI or a branded product?

VOQUEZNA is treated commercially as a branded alternative, so it clears payer coverage through rebate arrangements rather than pricing to generic ceilings.

2) What matters more for revenue: list price or net price?

Net price drives realized revenue because rebates and contract discounts dominate acid-suppressant class economics.

3) What is the biggest lever that changes VOQUEZNA’s effective price?

Formulary status in major PBM books (preferred vs non-preferred) and the resulting rebate corridor.

4) How do H. pylori indications affect pricing power?

They can support incremental volume and improve negotiating leverage if payer coverage is broad for regimen use, reducing rebate pressure over time.

5) What modeling approach best reflects VOQUEZNA’s pricing risk?

Scenario-based net-price indexing tied to formulary outcomes, with revenue sensitivity to both net price erosion and script volume growth.

References

[1] IQVIA. Drug pricing and market access frameworks for prescription medicines (class-level market dynamics). IQVIA Institute and market access resources.

[2] SSR Health. PBM formulary and rebate mechanisms affecting net drug pricing (industry framework).

[3] Centers for Medicare & Medicaid Services (CMS). Part D formulary and utilization management overview (coverage design inputs).

More… ↓