Share This Page

Drug Price Trends for SUNOSI

✉ Email this page to a colleague

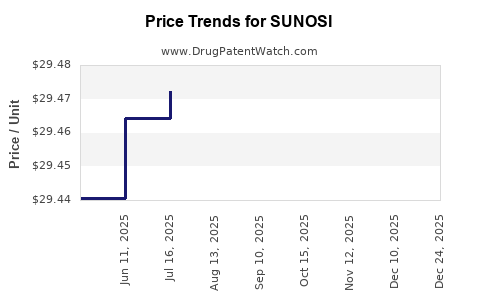

Average Pharmacy Cost for SUNOSI

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| SUNOSI 150 MG TABLET | 81968-0351-01 | 31.33321 | EACH | 2026-06-17 |

| SUNOSI 75 MG TABLET | 81968-0350-01 | 31.33299 | EACH | 2026-06-17 |

| SUNOSI 75 MG TABLET | 81968-0350-01 | 31.23983 | EACH | 2026-05-20 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for SUNOSI

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| SUNOSI 150MG TAB | Axsome Therapeutics, Inc. | 81968-0351-01 | 30 | 561.82 | 18.72733 | EACH | 2024-01-01 - 2028-02-14 | FSS |

| SUNOSI 75MG TAB | Axsome Therapeutics, Inc. | 68727-0350-01 | 30 | 468.18 | 15.60600 | EACH | 2023-02-15 - 2028-02-14 | FSS |

| SUNOSI 150MG TAB | Axsome Therapeutics, Inc. | 68727-0351-01 | 30 | 467.58 | 15.58600 | EACH | 2023-02-15 - 2028-02-14 | FSS |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

SUNOSI Market Analysis and Price Projections

SUNOSI (solriamfetol) is a wakefulness-promoting agent approved for the treatment of excessive daytime sleepiness (EDS) in adult patients with narcolepsy and adult patients with obstructive sleep apnea (OSA). Its market trajectory is influenced by its efficacy, safety profile, pricing strategy, and competitive landscape.

What is the Current Market Size and Growth Trajectory for SUNOSI?

SUNOSI's market penetration is directly tied to the prevalence of narcolepsy and OSA, two conditions characterized by EDS. The global narcolepsy market was valued at approximately $3.5 billion in 2022 and is projected to reach $5.9 billion by 2030, growing at a compound annual growth rate (CAGR) of 6.8% [1]. The OSA market is significantly larger, with an estimated global market size of $10.5 billion in 2022, projected to reach $18.2 billion by 2030, at a CAGR of 7.2% [2].

SUNOSI's specific market share within these segments is still developing. Its approval in 2019 and subsequent market launch positioned it as a novel therapeutic option. Post-launch sales figures provide a clearer indication of its current market impact:

- 2021 Revenue: $95.7 million [3]

- 2022 Revenue: $156.3 million [4]

- First Nine Months of 2023 Revenue: $143.6 million [5]

These figures demonstrate a consistent upward trend in revenue, indicating increasing adoption and market acceptance. The growth is driven by physician familiarity, patient access, and the unmet need for effective EDS treatments.

What are the Key Drivers of SUNOSI's Market Growth?

Several factors are propelling SUNOSI's market expansion:

- Addressing Unmet Needs: Both narcolepsy and OSA are chronic conditions with significant impacts on quality of life. Traditional treatments often have limitations, including side effects or incomplete efficacy. SUNOSI offers a distinct mechanism of action (dopamine and norepinephrine reuptake inhibition) that provides an alternative for patients who do not respond optimally to existing therapies.

- Broad Label Indications: Approval for both narcolepsy and OSA broadens its addressable patient population, increasing its market potential. This dual indication allows for wider physician prescribing and patient uptake.

- Favorable Clinical Data: Clinical trials demonstrated SUNOSI's efficacy in improving wakefulness in patients with EDS associated with both conditions. This robust data supports physician confidence in prescribing the drug. For instance, in the narcolepsy trials, SUNOSI demonstrated significant improvements in the Maintenance of Wakefulness Test (MWT) scores compared to placebo [6].

- Commercialization Strategy: The pharmaceutical company responsible for SUNOSI's commercialization employs targeted marketing and educational initiatives to raise awareness among healthcare providers and patients. This includes engagement with sleep specialists, neurologists, and primary care physicians who manage patients with sleep disorders.

- Payer Access and Reimbursement: Securing favorable formulary placement and reimbursement from major health insurance providers is critical. As of late 2023, SUNOSI has achieved significant payer coverage, making it more accessible to patients [7].

What is the Competitive Landscape for SUNOSI?

SUNOSI operates in a competitive but expanding market for wakefulness-promoting agents. Key competitors and their comparative positioning include:

- Modafinil/Armodafinil (Provigil/Nuvigil): These are established first-line treatments for EDS in narcolepsy and OSA. They are available generically, offering a significant price advantage. However, SUNOSI offers a different pharmacological profile and may be chosen for patients with insufficient response or tolerability to modafinil/armodafinil.

- Sodium Oxybate (Xyrem/Xywav): Primarily used for cataplexy and EDS in narcolepsy. Xyrem has a well-established efficacy but carries a significant side effect profile and strict prescribing requirements due to its controlled substance status. Xywav, a lower-sodium formulation, offers an alternative with a similar efficacy profile. SUNOSI competes by offering a non-scheduled alternative with a distinct mechanism.

- Pitolisant (Wakix): Approved for EDS in narcolepsy. Pitolisant acts as a histamine H3 receptor inverse agonist/antagonist. It represents a direct competitor within the narcolepsy indication, offering another non-stimulant option.

- Stimulants (e.g., amphetamines, methylphenidate): While not typically first-line for narcolepsy or OSA due to their stimulant properties and potential for abuse, they are sometimes used off-label for EDS, particularly in OSA. SUNOSI provides a non-stimulant, non-scheduled alternative.

SUNOSI's differentiation lies in its non-stimulant and non-scheduled status, its dual indication for narcolepsy and OSA, and its unique dopamine and norepinephrine reuptake inhibition mechanism. This allows it to capture market share from patients seeking alternatives to existing options.

What are the Factors Influencing SUNOSI's Pricing and Future Price Projections?

SUNOSI is a branded pharmaceutical product, and its pricing is determined by several key factors:

- Research and Development (R&D) Costs: The significant investment in drug discovery, clinical trials, and regulatory submissions is a primary driver of drug pricing.

- Therapeutic Value and Efficacy: SUNOSI's ability to demonstrably improve wakefulness and quality of life for patients with debilitating EDS is a major factor in its valuation and pricing.

- Competitive Pricing: The pricing of existing treatments, including branded and generic options, sets a benchmark. SUNOSI is priced competitively within the branded segment for wakefulness-promoting agents.

- Payer Negotiations and Reimbursement Landscape: Agreements with pharmacy benefit managers (PBMs) and insurance companies significantly impact the net price received by the manufacturer and the out-of-pocket costs for patients.

- Patent Exclusivity: SUNOSI benefits from patent protection, which grants market exclusivity and allows for premium pricing. The duration of this exclusivity is a critical determinant of its long-term revenue potential. U.S. patent protection for solriamfetol extends into the 2030s for key patents [8].

- Manufacturing and Distribution Costs: The cost of goods sold, including raw materials, manufacturing processes, and supply chain logistics, contributes to the final price.

- Market Demand and Patient Volume: As market penetration increases and patient demand grows, the manufacturer may adjust pricing strategies.

Current Pricing:

As of late 2023, the average wholesale price (AWP) for SUNOSI is approximately $350 to $400 per day, translating to roughly $10,500 to $12,000 per month [9]. Actual out-of-pocket costs for patients vary widely based on insurance coverage, co-pays, and patient assistance programs.

Future Price Projections:

Given the factors above, SUNOSI's pricing is expected to remain relatively stable in the short to medium term, supported by its patent exclusivity and demonstrated clinical value.

- 2024-2026: Continued price stability is anticipated, with potential for minor increases reflecting inflation and ongoing R&D investments. The average annual price could range from $130,000 to $150,000 per patient per year.

- 2027-2030: As patent cliffs approach for some older competitive drugs and generic versions of SUNOSI remain several years away, prices may see moderate adjustments. The focus will likely remain on demonstrating continued value and securing favorable reimbursement. The annual price is projected to be in the $140,000 to $160,000 range.

- Post-2030: The introduction of generic competition for SUNOSI would lead to a significant price decline, mirroring trends seen with other branded pharmaceuticals. However, the timing of generic entry depends on patent litigation and market dynamics.

It is important to note that these projections are subject to change based on regulatory policy shifts, new therapeutic developments, and evolving market access strategies.

What are the Regulatory and Policy Implications for SUNOSI's Market Access?

Regulatory approvals and ongoing policy decisions by governmental bodies and payers significantly shape SUNOSI's market access and trajectory.

- FDA Approval and Post-Marketing Surveillance: The U.S. Food and Drug Administration (FDA) approval in March 2019 for narcolepsy and December 2019 for OSA was the foundational step. Continued post-marketing surveillance for safety and efficacy is standard and crucial for maintaining market access.

- European Medicines Agency (EMA) Approval: SUNOSI received EMA approval in Europe in July 2020, broadening its global reach and revenue potential.

- Payer Coverage Policies: Health insurance companies and PBMs make decisions about formulary placement and reimbursement tiers. SUNOSI has been working to secure broad coverage. Factors influencing these decisions include:

- Clinical Utility: Evidence of SUNOSI's superior efficacy or safety compared to alternatives.

- Cost-Effectiveness: Analyses demonstrating that the drug's benefits justify its cost relative to other treatments.

- Prior Authorization and Step Therapy: Payers may implement requirements for prior authorization or mandate that patients try other, often less expensive, treatments first (step therapy) before approving SUNOSI. This can create access barriers.

- Patient Assistance Programs: Manufacturer-sponsored programs aim to reduce out-of-pocket costs for eligible patients, facilitating access and adherence.

- Drug Pricing Reforms and Government Policy: Potential legislative changes concerning drug pricing in the U.S. and other major markets could impact SUNOSI's pricing strategies and profitability. Policies aimed at increasing price transparency or negotiating drug prices could introduce downward pressure.

- Orphan Drug Exclusivity and Patent Law: SUNOSI benefits from patent protection and potentially other market exclusivities, which are critical for recouping R&D costs. Litigation challenging these exclusivities could impact its market lifespan and pricing.

Key Takeaways

SUNOSI is experiencing steady market growth, driven by its approval for narcolepsy and OSA, a differentiated mechanism of action, and favorable clinical data. Its current revenue trajectory indicates increasing adoption. The competitive landscape includes established generics and other branded agents, but SUNOSI's non-stimulant, non-scheduled profile provides a distinct value proposition. Pricing is expected to remain stable in the near to medium term, supported by patent exclusivity, with potential declines anticipated post-patent expiry. Payer coverage and evolving regulatory policies are critical determinants of market access and future revenue.

Frequently Asked Questions

- What is the primary mechanism of action for SUNOSI? SUNOSI is a selective norepinephrine and dopamine reuptake inhibitor.

- Which specific sleep disorders is SUNOSI approved to treat? SUNOSI is approved for excessive daytime sleepiness (EDS) in adult patients with narcolepsy and adult patients with obstructive sleep apnea (OSA).

- How does SUNOSI compare in price to generic wakefulness-promoting agents like modafinil? SUNOSI is a branded product and is priced significantly higher than generic versions of modafinil and armodafinil.

- When is SUNOSI's U.S. patent protection expected to expire? Key patents for solriamfetol are expected to provide market exclusivity into the 2030s.

- What are the most significant barriers to SUNOSI's market penetration? Barriers include payer restrictions such as prior authorization and step therapy requirements, as well as competition from lower-cost generic alternatives and other branded therapies.

Citations

[1] Grand View Research. (2023). Narcolepsy market size, share & trends analysis report. [2] Fortune Business Insights. (2023). Obstructive Sleep Apnea (OSA) Market: Global Size, Share, & Industry Trends. [3] Jazz Pharmaceuticals PLC. (2022). 2021 Annual Report. [4] Jazz Pharmaceuticals PLC. (2023). 2022 Annual Report. [5] Jazz Pharmaceuticals PLC. (2023). Third Quarter 2023 Earnings Release. [6] U.S. Food & Drug Administration. (2019). SUNOSI (solriamfetol) Prescribing Information. [7] Jazz Pharmaceuticals PLC. Investor Relations Communications. (Data on file). [8] United States Patent and Trademark Office. (Patent database search for solriamfetol). [9] Redbook® and First Databank® databases. (Subscription-based pharmaceutical pricing information, accessed November 2023).

More… ↓