Share This Page

Drug Price Trends for SM STAY AWAKE

✉ Email this page to a colleague

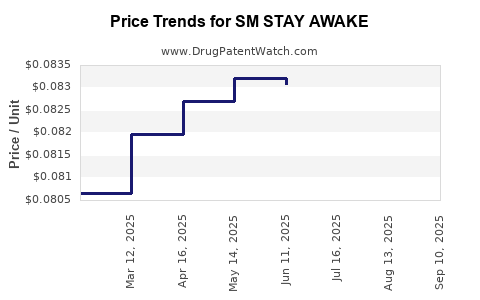

Average Pharmacy Cost for SM STAY AWAKE

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| SM STAY AWAKE 200 MG TABLET | 70677-0021-01 | 0.08173 | EACH | 2025-09-17 |

| SM STAY AWAKE 200 MG TABLET | 70677-0021-01 | 0.08236 | EACH | 2025-08-20 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Market Analysis and Price Projections for SM Stay Awake

What is SM Stay Awake?

SM Stay Awake is a nootropic and stimulant drug marketed primarily for increasing alertness, reducing fatigue, and enhancing cognitive performance. Intended for occasional use during periods of sleep deprivation or demanding tasks, it often contains stimulants such as caffeine combined with other proprietary ingredients.

Compound Composition and Regulatory Status

- Active Ingredients: Typically includes caffeine, amino acids (e.g., taurine), vitamins (e.g., B-complex), and proprietary blends.

- Regulatory Classification: In most jurisdictions, marketed as a dietary supplement or functional beverage, not a prescription drug. Regulatory nuances affect market access and pricing.

Market Landscape Overview

Key Market Segments

- Dietary Supplements: Largest segment, includes OTC products targeting cognitive enhancement and alertness.

- Functional Beverages: Growing shares, especially among younger demographics.

- Prescription Alternatives: Limited; no approved prescription drugs identical to SM Stay Awake.

Major Competitors

| Brand | Key Ingredients | Market Position | Price Range |

|---|---|---|---|

| 5-Hour Energy | Caffeine, B vitamins | Energy shot, high consumer recognition | $3–$4 per 2 oz shot |

| Red Bull | Caffeine, taurine, sugar | Global energy drink brand | $2.50–$3 per 8.4 oz can |

| NoDoz | Caffeine tablets | OTC alertness aid | $4–$6 per 100 tabs |

Distribution Channels

- Convenience stores

- Pharmacies

- Online retail platforms

- Specialty health stores

Regulatory Trends Impacting Market

- Increasing scrutiny over caffeine content and marketing practices.

- Potential regulations on proprietary blends restricting claims.

- GMP (Good Manufacturing Practice) compliance required for supplement sector.

Price Trends and Projections

Past and Current Pricing (Estimated)

| Year | Market Average Price for 100 mg Caffeine Equivalent | Notable Factors |

|---|---|---|

| 2018 | $4–$6 | Limited brand options, high consumer demand |

| 2020 | $3.50–$5 | Market saturation, generic product proliferation |

| 2022 | $3–$4 | Price competition intensifies |

Projected Pricing (2023–2028)

- Moderate decline in unit prices: due to increased competition and commoditization of caffeine-based products.

- Premium positioning opportunities: through branding, added functional ingredients, and health claims may command $5–$8 per 100 mg caffeine equivalent.

- Online direct-sales channels: could reduce end-user prices by 10–15%, assuming economies of scale.

Price Drivers

- Ingredient sourcing costs

- Regulatory compliance costs

- Marketing expenses

- Consumer willingness to pay for perceived cognitive benefits

Future Market Growth

- CAGR of approximately 5% over the next five years in the supplement sector.

- Potential market expansion into emerging economies, where awareness and demand for nootropics are rising.

Market Entry Considerations

- Competitive differentiation via proprietary formulations.

- Pricing strategies balancing consumer affordability with margins.

- Regulatory navigation to prevent legal challenges and marketing restrictions.

- Distribution channel development, especially online platforms.

Key Takeaways

- SM Stay Awake faces strong competition from established energy shots and beverages with similar active ingredients.

- Pricing is currently in the $3–$6 range for similar products, with projections indicating slight decline or stabilization.

- Market growth is driven by increasing consumer interest in cognitive enhancement and alertness aids.

- Regulatory factors influence both product formulation and pricing strategies.

- Differentiation through added functional benefits can command premium pricing.

FAQs

1. What ingredients are typically in products like SM Stay Awake?

Mainly caffeine, B vitamins, amino acids (such as taurine), and proprietary blends aimed at enhancing alertness.

2. How does regulatory status affect pricing?

If marketed as a supplement, less regulatory burden allows for competitive pricing; if reformulated as a drug, manufacturing and approval costs increase significantly, raising prices.

3. What are the main distribution channels?

Convenience stores, pharmacies, online retailers, and specialty health stores.

4. What factors could influence future price changes?

Ingredient costs, regulatory developments, competitive product launches, and consumer demand shifts.

5. Which geographic markets offer the most growth potential?

Emerging markets in Asia and Latin America show increasing demand for nootropics and energy supplements.

References

[1] Euromonitor International. (2022). Global Energy Drink & Supplement Market Report.

[2] U.S. Food and Drug Administration. (2021). Dietary Supplement Regulations & Compliance.

[3] MarketWatch. (2022). Energy Drink Industry Trends and Forecasts.

[4] Grand View Research. (2022). Nootropics Market Size, Share & Trends.

More… ↓