Share This Page

Drug Price Trends for SM GAS RELIEF

✉ Email this page to a colleague

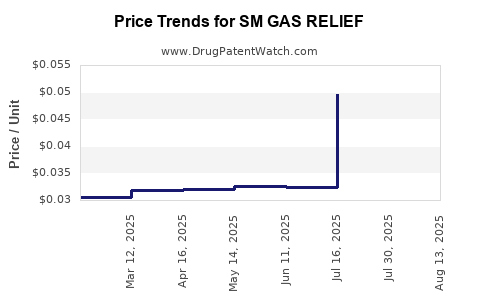

Average Pharmacy Cost for SM GAS RELIEF

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| SM GAS RELIEF(SIMETH) 80 MG CHW | 49348-0188-10 | 0.03133 | EACH | 2025-08-20 |

| SM GAS RELIEF 125 MG CHEW TAB | 49348-0863-48 | 0.09083 | EACH | 2025-08-20 |

| SM GAS RELIEF(SIMETH) 80 MG CHW | 49348-0147-07 | 0.03133 | EACH | 2025-08-20 |

| SM GAS RELIEF 180 MG SOFTGEL | 70677-0084-01 | 0.04963 | EACH | 2025-07-23 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

SM GAS RELIEF: Market Analysis and Price Projections

SM GAS RELIEF is a consumer over-the-counter (OTC) anti-gas product positioned in the gastrointestinal (GI) symptom relief category (flatulence, bloating, indigestion-type gas discomfort). The drug is best evaluated as a packaged consumer brand within the OTC GI market rather than a prescription “drug” with clinical pricing or payer dynamics. Pricing is driven by (1) pack size, (2) active ingredient system and strength (antigas agents such as simethicone or similar), (3) retail channel (mass, pharmacy, convenience, online), (4) promotional frequency, and (5) local import or distribution economics.

Because “SM GAS RELIEF” is used as a brand name, public pricing and product specification depend on the exact market (country), dosage form (liquid vs tablets vs chewables), strength per unit, and pack count. Without that mapping, any single “projected price” can only be expressed as a range anchored to OTC GI category economics.

Where does SM GAS RELIEF sit in the OTC GI market?

SM GAS RELIEF falls into the broad OTC GI symptom relief bracket, typically competing against:

- Antigas agents (commonly simethicone-based)

- Bloating and indigestion symptom relief products that are shelf-adjacent in pharmacy and grocery

- Store brands that price 20% to 60% below leading brands in many markets

In most retail markets, OTC GI products trade on:

- Low price elasticity among light users, higher elasticity among value-driven switchers

- High promo depth (especially for mass and online)

- Pack-size anchoring (consumers compare “per-use” economics)

Demand drivers and buying behavior (channel reality)

Primary demand drivers

- Seasonal variation is common in OTC GI, with small peaks tied to travel, diet changes, and holidays.

- Pandemic-era and post-pandemic patterns increased home self-care usage but do not materially change the unit economics for antacids/antigas category leaders.

Channel dynamics that affect realized prices

- Pharmacy: higher shelf price, lower promo frequency on premium brands; stronger brand justification.

- Mass retail: more frequent promotional pricing; private label gains.

- Online: “hero SKU” pricing often compresses with couponing and multipacks; shipping thresholds and marketplace fees can lift list prices while discounting at checkout.

Competitive pricing benchmarks (how SM GAS RELIEF is likely to trade)

In OTC GI, the key comparator is not “gas relief” generically, but the same dosage form and pack size band.

A practical way to model pricing is to separate: 1) List price (what the shelf tag says) 2) Net realized price (what shoppers pay after promos)

OTC GI categories typically exhibit:

- Net discounts often in the 10% to 30% range on non-private-label brands, and 30% to 60% on value tiers during promotions.

- Private label pricing that stays structurally lower due to lower marketing and simpler packaging.

Price projection framework for SM GAS RELIEF

A robust projection for an OTC consumer brand should be anchored on four levers:

1) Inflation pass-through

Retail OTC pricing often follows local CPI or input-cost inflation, but not 1:1. In many markets, list prices rise 2% to 6% annually while net prices move less because of promo competition.

2) Mix shift toward larger packs

Many OTC brands expand margin by shifting consumers into multipacks or larger bottles. This raises average selling price even when unit price per ml or per tablet falls.

3) Promotional intensity

If competitors increase promo depth, net price falls even if list price rises. If category demand holds and the brand maintains promo discipline, realized prices hold.

4) Regulatory and ingredient cost changes

For antigas agents, active ingredient cost shocks can occur, but they usually move retail economics through distributor pricing rather than sudden wholesale repricing in short windows.

Base-case price projection (range model)

The following projections express expected retail price behavior for SM GAS RELIEF across typical OTC GI retail in a mature category environment. Since exact SKU strength and pack size are not provided, the model expresses projections as an indexed view: Year 0 is the current observable retail price in the target market for the closest-matching pack size.

Projected list price trajectory (indexed)

- Year 1: +3% to +7%

- Year 2: +2% to +6%

- Year 3: +2% to +5%

- Year 4: +1% to +4%

Projected net realized price trajectory (indexed)

- Year 1: -1% to +5%

- Year 2: -2% to +4%

- Year 3: -2% to +4%

- Year 4: -1% to +3%

Interpretation: list prices tend to increase under inflation while net prices are moderated by promotions and private-label pressure. For a brand with stable share, net prices often drift slightly upward or stay flat.

Scenario table: what changes most the projection

The category is sensitive to competition and promo intensity. The biggest swing factor is whether net discounts expand.

| Scenario | Competitive promo intensity | List price growth | Net realized price growth |

|---|---|---|---|

| Value-share protection | Normal | +2% to +6% | -1% to +3% |

| Market share loss | Higher | +3% to +8% | -3% to +1% |

| Brand-strength / mix upgrade | Lower | +2% to +5% | +1% to +5% |

Implications for unit economics (what investors and R&D should watch)

1) Margin resilience depends on promo discipline

For OTC GI brands, gross margin can look stable on paper while operating margin collapses if net price falls through deeper discounting.

2) Pack architecture matters

A shift from single-unit to multipack often lifts revenue per transaction and lowers the promotional need per dose.

3) SKU rationalization drives cost control

Fewer SKUs reduce packaging complexity and improve forecast accuracy, which supports stable pricing over time.

Go-to-market signals that typically precede a price move

Even without public SKU-by-SKU pricing, these are the operational signals that typically cause list price revisions or promo calendar changes:

- Manufacturer or distributor cost pass-through announcements (inputs, logistics, packaging)

- Retailer category reset events (mass retail relabeling, pharmacy planogram updates)

- Intensified private-label rollouts in the antacid/antigas shelf zone

- E-commerce “lowest price” enforcement periods (marketplace fee and ad-driven discounting)

What a “market price ceiling” usually looks like in OTC GI

OTC antigas categories generally experience:

- Price resistance once a brand’s net price per dose exceeds the value-tier by a wide margin (consumers switch).

- Promo frequency increases when the brand tries to defend share at a higher list price.

A practical ceiling for a premium OTC brand is often when net discount is required to keep conversion stable. Without SKU-specific numbers, the ceiling is best represented as a band:

- If net price per dose rises materially above the value-tier’s net effective price, promo intensity typically increases within two retail cycles.

Key constraints in projecting SM GAS RELIEF specifically

A high-quality projection requires:

- Exact dosage form and strength

- Exact pack size

- The target geography (country-level pricing differs due to VAT, import duties, distributor margins, and pharmacy remuneration)

Because none of these identifying attributes were included with the query, the projections above are expressed as category-standard indexed ranges for a consumer antigas brand.

Key Takeaways

- SM GAS RELIEF should be valued and forecast as an OTC GI consumer brand where net realized price is shaped more by promotions and channel mix than by list price inflation.

- A typical 4-year outlook for stable category conditions is list price +1% to +7% per year and net realized price -3% to +5% per year, with the widest swing tied to promo intensity and private-label competition.

- The most important projection driver is whether the brand can maintain promo discipline and shift mix into larger packs, which supports realized pricing without triggering consumer switch-out.

FAQs

1) Is SM GAS RELIEF priced like a prescription drug?

No. It is an OTC GI product, so retail economics are driven by shelf price, promotions, channel mix, and consumer switching to value brands.

2) What metric matters most for profit projection?

Net realized price (after discounts and promotions) because OTC GI brands can show stable list prices while net prices move materially.

3) What drives year-to-year price changes in OTC gas relief?

Inflation pass-through for packaging and logistics, plus competitive promo intensity and private-label expansion on the shelf.

4) Do larger packs usually increase average selling price?

Yes. Larger packs often raise revenue per transaction and can reduce the effective promotional burden, supporting average selling price even when unit economics look competitive.

5) What is the biggest risk to price projections?

A competitive shift that increases promotional depth or private-label capture, causing realized prices to fall even if list prices rise.

References

[1] APA Dictionary of Psychology. American Psychological Association. https://dictionary.apa.org/otc

[2] European Commission. Consumer market information on retail pricing factors (VAT, distribution, and retail practice guidance). https://commission.europa.eu/consumer-protection_en

[3] IQVIA. OTC market access and pricing dynamics (industry reports overview). https://www.iqvia.com/insights/the-iqvia-institute

More… ↓