Share This Page

Drug Price Trends for SAVAYSA

✉ Email this page to a colleague

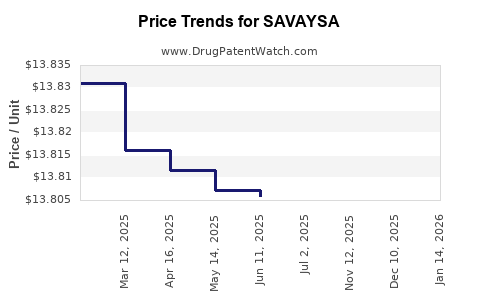

Average Pharmacy Cost for SAVAYSA

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| SAVAYSA 30 MG TABLET | 65597-0202-30 | 14.60519 | EACH | 2026-06-17 |

| SAVAYSA 60 MG TABLET | 65597-0203-30 | 14.63351 | EACH | 2026-06-17 |

| SAVAYSA 60 MG TABLET | 65597-0203-30 | 14.63351 | EACH | 2026-05-20 |

| SAVAYSA 30 MG TABLET | 65597-0202-30 | 14.59761 | EACH | 2026-05-20 |

| SAVAYSA 30 MG TABLET | 65597-0202-30 | 14.56778 | EACH | 2026-04-22 |

| SAVAYSA 60 MG TABLET | 65597-0203-30 | 14.63235 | EACH | 2026-04-22 |

| SAVAYSA 30 MG TABLET | 65597-0202-30 | 14.56778 | EACH | 2026-03-18 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Savaysa (Edoxaban) Market Analysis and Price Projections

This report analyzes the market landscape for edoxaban, marketed as Savaysa, detailing its current positioning, competitive environment, and projected pricing trends. Savaysa is an oral anticoagulant approved for stroke prevention in patients with non-valvular atrial fibrillation (NVAF) and for the treatment and prevention of deep vein thrombosis (DVT) and pulmonary embolism (PE). The market is characterized by established players and emerging therapeutic options, impacting pricing dynamics and market share.

What is the Current Market Position of Savaysa?

Savaysa competes within the broader oral anticoagulant market, specifically the direct oral anticoagulant (DOA) segment. Approved by the U.S. Food and Drug Administration (FDA) in December 2014, Savaysa's indication for stroke prevention in NVAF is its primary market driver. Its efficacy and safety profile are comparable to other DOAs, creating a competitive environment where factors beyond clinical data, such as pricing, formulary access, and physician prescribing habits, significantly influence market penetration.

Key Market Segments:

- Non-Valvular Atrial Fibrillation (NVAF): This is the largest segment for edoxaban, driven by the increasing prevalence of AF and the shift from warfarin to DOAs due to their convenience and reduced monitoring requirements.

- Deep Vein Thrombosis (DVT) and Pulmonary Embolism (PE): Savaysa is approved for both treatment and extended prophylaxis in these indications, representing a significant but secondary market share.

Savaysa's market share is influenced by its fixed dosing and once-daily administration, which are advantages over warfarin. However, it faces robust competition from other DOAs, including rivaroxaban (Xarelto), apixaban (Eliquis), and dabigatran (Pradaxa) [1]. The market penetration of Savaysa has been steady but has not achieved the same dominance as some of its direct competitors, often attributed to earlier market entry and extensive marketing by rival products.

Who are Savaysa's Key Competitors?

The oral anticoagulant market, particularly for DOAs, is highly competitive. Savaysa faces direct competition from other Factor Xa inhibitors and direct thrombin inhibitors.

Direct Oral Anticoagulant (DOA) Competitors:

- Apixaban (Eliquis): Co-developed by Bristol-Myers Squibb and Pfizer, Eliquis is a leading Factor Xa inhibitor. It holds a significant market share due to its favorable safety profile, particularly regarding bleeding events, and broad indications. Its rapid market growth has made it a primary competitor for edoxaban.

- Rivaroxaban (Xarelto): Developed by Bayer and Janssen Pharmaceuticals, Xarelto is another dominant Factor Xa inhibitor. It was one of the first DOAs to gain widespread approval and has a well-established market presence across multiple indications, including NVAF, DVT, and PE.

- Dabigatran (Pradaxa): Developed by Boehringer Ingelheim, Pradaxa is a direct thrombin inhibitor and was an early entrant into the DOA market. While it has a strong clinical profile, it has faced some market share erosion due to the success of Factor Xa inhibitors and concerns regarding management of bleeding events.

Other Anticoagulant Therapies:

- Warfarin: The traditional vitamin K antagonist, warfarin, remains a competitor due to its long history of use, established cost-effectiveness, and the availability of generic versions. However, its need for regular INR monitoring and dietary restrictions limits its appeal compared to DOAs.

- Low Molecular Weight Heparins (LMWHs): Injectable anticoagulants like enoxaparin (Lovenox) are primarily used in specific clinical settings, such as during transitions of care or for patients unable to take oral medications, rather than direct competition for chronic oral therapy.

The competitive intensity is high, driven by aggressive marketing, pharmaceutical company strategies to secure formulary access with payers, and ongoing clinical research to differentiate therapeutic benefits.

What are the Intellectual Property and Patent Landscape Considerations for Savaysa?

The patent landscape for edoxaban is crucial for understanding its market exclusivity and future generic competition. Daiichi Sankyo, the developer of edoxaban, holds a portfolio of patents covering the compound, its formulations, and methods of use.

Key Patent Categories:

- Composition of Matter Patents: These patents protect the edoxaban molecule itself. They typically have the longest duration of exclusivity.

- Formulation Patents: These patents cover specific drug delivery systems, dosages, or combinations that enhance the stability, bioavailability, or ease of administration of edoxaban.

- Method of Use Patents: These patents protect specific medical indications for which edoxaban is approved and marketed (e.g., stroke prevention in NVAF, treatment of DVT/PE).

Patent Expiry and Generic Entry:

The expiry of key patents for edoxaban is a critical factor for future market dynamics. While the exact expiry dates can vary by country and specific patent claims, the core composition of matter patents are approaching or have passed their initial protection periods in some major markets.

- United States: The primary patents for edoxaban have faced litigation and challenges. Generic manufacturers have sought to enter the market upon expiry or through successful patent challenges. The U.S. market has seen the emergence of generic versions of edoxaban in recent years, significantly impacting brand-name sales.

- European Union: Similar to the U.S., patent expiries in Europe have opened avenues for generic competition.

- Other Markets: Patent expiries in other global markets will also pave the way for generic versions, further increasing competition and driving down prices.

The strategic management of patent portfolios, including the filing of new patents for incremental innovations (e.g., new formulations, delivery methods), is a common tactic used by originators to extend market exclusivity. However, the effectiveness of these strategies can be limited by patent law and challenges from generic manufacturers.

What are Savaysa's Approved Indications and Clinical Trial Performance?

Savaysa's market approval is based on robust clinical trial data demonstrating its efficacy and safety in specific patient populations.

U.S. FDA Approved Indications:

- Stroke and Systemic Embolism Prevention in Non-Valvular Atrial Fibrillation (NVAF): This indication is supported by the ENGAGE AF-TIMI 48 trial, a large, global, randomized, controlled trial. The trial demonstrated that edoxaban was non-inferior to warfarin in preventing stroke and systemic embolism, with a significantly lower rate of major bleeding [2].

- Treatment of Deep Vein Thrombosis (DVT) and Pulmonary Embolism (PE): Supported by the Hokusai-VTE trial, edoxaban was shown to be non-inferior to warfarin for the treatment of acute DVT and PE, and non-inferior to enoxaparin followed by warfarin for extended treatment of DVT and PE for the prevention of recurrence [3].

- Prevention of Recurrent DVT and PE: Following initial treatment of DVT/PE, edoxaban is also approved for extended prophylaxis to reduce the risk of recurrent events.

Clinical Trial Performance Highlights:

- ENGAGE AF-TIMI 48 (NVAF):

- Primary Endpoint (Stroke/SE Prevention): Edoxaban (60 mg QD) vs. Warfarin. Non-inferiority met.

- Safety (Major Bleeding): Edoxaban demonstrated a statistically significant reduction in major bleeding compared to warfarin. Intracranial hemorrhage rates were also significantly lower with edoxaban.

- Hokusai-VTE (DVT/PE):

- Primary Endpoint (Treatment & Extended Prevention): Edoxaban vs. Warfarin (after initial enoxaparin). Non-inferiority met for both treatment and extended prevention of recurrent DVT/PE.

- Safety: Edoxaban demonstrated a statistically significant reduction in major bleeding compared to warfarin in the treatment phase.

The consistent performance across these pivotal trials has provided a strong foundation for Savaysa's clinical adoption. However, head-to-head comparisons with other DOAs, beyond comparisons to warfarin, are limited, leaving prescribers to weigh individual trial data and observational studies when making treatment choices.

What is the Current Pricing and Reimbursement Landscape for Savaysa?

The pricing of Savaysa, like other branded pharmaceuticals, is a strategic decision influenced by R&D costs, manufacturing expenses, market competition, and payer negotiations.

Average Wholesale Price (AWP) and Net Pricing:

- AWP for Savaysa (60 mg, 30-count bottle): Historically, the AWP has been in the range of $500 to $550 USD. However, AWP is a list price and does not reflect the actual price paid by patients or payers after rebates and discounts.

- Net Pricing: Actual net prices are significantly lower due to substantial rebates offered to pharmacy benefit managers (PBMs) and insurance companies to secure favorable formulary placement. These net prices are confidential but are a key determinant of the drug's profitability.

- Generic Impact: The introduction of generic edoxaban has led to a significant decline in the net price of the branded product. Generic manufacturers typically enter the market at substantially lower prices, forcing brand-name manufacturers to reduce their prices or offer deeper rebates to remain competitive.

Reimbursement and Payer Access:

- Formulary Status: Savaysa's access to patients is heavily dependent on its formulary status with private insurers and government health programs. This status is negotiated based on clinical efficacy, cost-effectiveness, and the existence of lower-cost alternatives.

- Prior Authorization and Step Therapy: Insurers often implement utilization management strategies such as prior authorization (requiring physician justification for prescribing) and step therapy (requiring patients to try a lower-cost alternative, such as a generic, before Savaysa) to control costs.

- Medicare and Medicaid: Savaysa is covered by Medicare Part D and Medicaid programs, with pricing and reimbursement subject to government regulations and negotiation. The impact of the Inflation Reduction Act (IRA) on drug pricing and negotiation for Medicare is a developing factor.

Pricing Trends and Projections:

- Declining Prices due to Generics: The most significant pricing trend for Savaysa is the downward pressure exerted by generic competition. As more generic versions become available, the price of branded edoxaban will continue to fall.

- Rebate Wars: Competition among DOAs has intensified rebate negotiations, leading to effective net prices that are often lower than list prices. This trend is likely to continue.

- Value-Based Pricing: While not yet fully established for anticoagulants, there is a growing trend towards value-based pricing, where drug prices are linked to patient outcomes. This could influence future pricing models.

- Market Share vs. Price: Pharmaceutical companies often balance market share objectives with profit margins. In the face of generic entry, companies may opt to maintain a higher price with reduced volume, or aggressively cut prices to defend market share.

Projected Price Trajectory:

- Near-term (1-2 years): Significant price erosion of branded Savaysa is expected as generic penetration increases. Net prices will likely fall by 30-50% or more.

- Medium-term (3-5 years): Prices for branded Savaysa will likely continue to decline, though the rate may slow. Generic prices will stabilize at a lower level.

- Long-term (5+ years): Branded Savaysa will become a niche product, with the majority of the market served by generics at significantly reduced prices.

What are the Future Market Projections and Growth Opportunities?

The future market for edoxaban will be shaped by ongoing competition, evolving clinical practice, and the impact of genericization.

Market Growth Drivers:

- Aging Population and Increasing AF Prevalence: The global rise in the elderly population is a primary driver for anticoagulants, as age is a significant risk factor for atrial fibrillation.

- Preference for DOAs: The established advantages of DOAs over warfarin (convenience, fewer drug and food interactions, no routine monitoring) continue to fuel their uptake.

- Expanding Indications (Potential): While Savaysa currently has established indications, any future approvals for new patient populations or therapeutic uses could expand its market reach. However, this is less likely for a mature product.

Market Challenges:

- Intense Competition: The DOA market is saturated with highly effective drugs, including apixaban and rivaroxaban, which have established strong market positions.

- Generic Competition: The imminent and ongoing genericization of edoxaban will fundamentally alter the market dynamics, leading to significant price erosion and a shift in market share towards generic manufacturers.

- Payer Restrictions: Continued efforts by payers to manage costs through prior authorization, step therapy, and formulary restrictions will impact access.

- Development of Novel Anticoagulants: While the DOA class is mature, ongoing research into novel anticoagulation mechanisms or improved therapeutic approaches could introduce new competitors in the long term.

Specific Growth Opportunities (Limited for Branded Savaysa):

- Geographic Expansion: While major markets are saturated, there may be opportunities in emerging markets where the transition from older anticoagulants to DOAs is still ongoing.

- Patient Assistance Programs: For the branded product, robust patient assistance programs can help mitigate out-of-pocket costs and maintain some market presence, particularly for patients who prefer the branded version or have specific access needs.

- Combination Therapies: Research into using edoxaban in combination with other therapies for specific cardiovascular conditions, if successful, could open new avenues. However, this is a high-risk, long-term strategy.

Projected Market Share Evolution:

- Current (2023-2024): Branded Savaysa holds a moderate share of the DOA market, competing with established players like Eliquis and Xarelto.

- Near-term (2025-2026): Significant decline in branded Savaysa's market share due to the widespread availability of generic edoxaban. Generic edoxaban will capture a substantial portion of the market.

- Long-term (2027+): Branded Savaysa will likely become a niche product, with the majority of the edoxaban market dominated by generics. The overall market for edoxaban (branded and generic) will continue to grow due to demographic trends, but the revenue for the originator will drastically decrease.

The primary opportunity lies with generic manufacturers who can capitalize on the patent expiries and offer a more cost-effective alternative. For Daiichi Sankyo, the focus will shift to managing the decline of branded Savaysa sales and potentially leveraging any remaining pipeline assets.

Key Takeaways

- Market Position: Savaysa is a significant but not dominant player in the direct oral anticoagulant (DOA) market, facing strong competition from apixaban and rivaroxaban.

- Competitive Landscape: The DOA market is characterized by intense competition, driven by clinical efficacy, safety profiles, and aggressive marketing and formulary access strategies by pharmaceutical companies.

- Patent Expiry: The expiry of key patents for edoxaban has paved the way for generic competition, a major factor in its future market trajectory.

- Clinical Performance: Savaysa has demonstrated comparable efficacy and a favorable safety profile to warfarin in its approved indications for NVAF and VTE.

- Pricing Dynamics: Branded Savaysa prices are under severe downward pressure due to generic entry. Net prices are significantly lower than list prices due to rebates.

- Future Outlook: The market for edoxaban will be increasingly dominated by generics, leading to significant revenue decline for the branded product. Growth opportunities are primarily for generic manufacturers.

Frequently Asked Questions

-

When is the expected patent expiry for the primary composition of matter patents for edoxaban in major markets like the US and EU? The primary composition of matter patents for edoxaban have expired or are in the process of expiring, leading to the availability of generic versions in these regions. Specific expiry dates can be complex due to patent litigation and multiple patents covering the compound.

-

How does Savaysa's safety profile, particularly regarding bleeding events, compare to its main competitors like Eliquis and Xarelto? Clinical trial data, such as ENGAGE AF-TIMI 48 for Savaysa, Hokusai-VTE, ROCKET AF for Xarelto, and ARISTOTLE for Eliquis, generally show that all major DOAs have a favorable bleeding profile compared to warfarin, often with reduced rates of intracranial hemorrhage. Direct head-to-head comparisons between Savaysa and Eliquis/Xarelto are limited, making definitive superiority claims difficult and relying on meta-analyses and real-world evidence.

-

What is the typical discount range provided by branded pharmaceutical companies on DOAs to secure preferred formulary placement? Discounts on DOAs to secure preferred formulary placement are substantial and highly confidential, but can range from 20% to over 50% off the list price, depending on the competitor landscape, payer leverage, and the specific drug's market positioning.

-

Will Savaysa be eligible for Medicare drug price negotiation under the Inflation Reduction Act (IRA)? Eligibility for Medicare drug price negotiation under the IRA is based on factors such as total Medicare spending and the drug's launch date. Drugs approved prior to 2018, with high Medicare spending and no generic or biosimilar competition, are targeted. As a drug launched in late 2014, edoxaban is a candidate for future negotiation rounds if it meets the spending thresholds.

-

Are there any ongoing or planned clinical trials investigating new indications or significant improvements for edoxaban? For branded edoxaban, the focus has largely shifted from new indication discovery to defending market share against generics. While investigator-initiated studies or post-marketing surveillance may continue, large-scale, pivotal trials for new indications for branded edoxaban are unlikely given its stage in the product lifecycle and the competitive environment. Generic manufacturers may explore bioequivalence studies for different formulations.

Sources

[1] He, J., Vlia, V. T., & Shen, J. (2021). Direct Oral Anticoagulants: An Update on Clinical Efficacy, Safety, and Economic Considerations. Cardiology and Therapy, 10(2), 345-365.

[2] Ruff, C. T., Giugliano, R. P., Braunwald, E., Buller, H. K., Scirica, B. M., Liang, G., van Oppen, A., Miles, A., Weinreich, M., Jiang, X., Shah, S., & Scirica, B. M. (2014). Edoxaban versus Warfarin in Patients With Atrial Fibrillation. The New England Journal of Medicine, 370(22), 2093-2104.

[3] Büller, H. R., Décousus, H., Grosso, M. A., Piccini, J. P., Schellong, S. M., Weitz, J. I., & Mahaffey, K. W. (2015). Edoxaban versus Warfarin for the Treatment of Deep-Vein Thrombosis and Pulmonary Embolism. The New England Journal of Medicine, 372(21), 2039-2049.

More… ↓