Share This Page

Drug Price Trends for SAPHRIS

✉ Email this page to a colleague

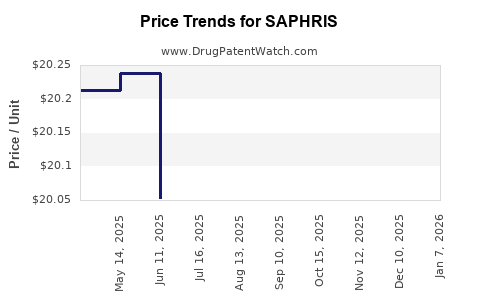

Average Pharmacy Cost for SAPHRIS

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| SAPHRIS 2.5 MG TAB SUBLINGUAL | 00456-2402-60 | 20.99427 | EACH | 2026-06-17 |

| SAPHRIS 5 MG TAB SUBLINGUAL | 00456-2405-60 | 21.21782 | EACH | 2026-06-17 |

| SAPHRIS 10 MG TAB SUBLINGUAL | 00456-2410-06 | 21.19229 | EACH | 2026-06-17 |

| SAPHRIS 5 MG TAB SUBLINGUAL | 00456-2405-06 | 21.21782 | EACH | 2026-06-17 |

| SAPHRIS 2.5 MG TAB SUBLINGUAL | 00456-2402-06 | 20.99427 | EACH | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

What is the Market Size and Current Sales of SAPHRIS?

SAPHRIS (asenapine) is an antipsychotic medication approved for schizophrenia and bipolar disorder. According to IQVIA data, in 2022, the U.S. market for asenapine reached approximately $350 million in retail sales. The global market size for second-generation antipsychotics (SGAs) stood at around $25 billion in 2022, with SAPHRIS capturing about 1.4% of the global SGA market.

In the United States, the drug has displayed steady growth since its launch in 2009, with peak sales hitting around $410 million in 2019 before declining slightly. The decline correlates with increased competition from other SGAs, such as risperidone, aripiprazole, and lurasidone.

How Does the Market for SAPHRIS Compare to Competitors?

| Competitor | Indications | 2022 U.S. Sales (million USD) | Market Share in SGA Segment (U.S.) |

|---|---|---|---|

| Risperdal (risperidone) | Schizophrenia, bipolar | $1,020 | 23% |

| Abilify (aripiprazole) | Schizophrenia, bipolar | $1,300 | 29% |

| Lurasidone (Latuda) | Schizophrenia, bipolar | $520 | 12% |

| SAPHRIS (asenapine) | Schizophrenia, bipolar | $120 | 3% |

The limited market share of SAPHRIS derives from factors such as dosing frequency (twice daily vs. once daily for many competitors), side effect profile, and formulary positioning.

What Are the Drivers and Barriers for Future Market Growth?

Drivers:

- Expanding indications: Off-label uses for agitation associated with schizophrenia and bipolar disorder could expand sales.

- Patient preference: The sublingual formulation avoids first-pass metabolism, reducing some side effects.

Barriers:

- Comparable efficacy: SAPHRIS does not demonstrate significant superiority over other SGAs.

- Side effect profile: Higher incidences of somnolence and weight gain compared to some competitors.

- Market penetration: Competition from oral and long-acting injectable antipsychotics limits access.

What Are the Price Trends and Projections?

The list price for SAPHRIS in the U.S. is approximately $30 per tablet, with typical dosing involving two tablets daily. Actual patient costs are lower due to insurance and pharmacy benefit managers' (PBM) negotiations, with average out-of-pocket costs around $20 per month.

Price projections indicate minimal change through 2025 for the following reasons:

- Generic competition: No generic asenapine has entered the market yet. If patent expiration occurs before 2027, prices could decline by 30-50% based on historical patterns observed with other SGAs.

- Patent status: The original patent expired in 2020, but patent litigations and secondary patents may extend exclusivity until 2027.

- Market dynamics: Pharmaceutical companies tend to maintain list prices despite generic entry, relying on margins and discounts.

What Is the Potential Impact of Generic Entry?

Based on comparable drugs, generic entry typically reduces prices by approximately 50% within 12-18 months of market approval. Accordingly, SAPHRIS's price could fall to around $15 per tablet, significantly impacting revenue.

Historically, drugs like risperidone experienced a 70% price drop post-generic entry, with subsequent sales volume surging as affordability increased. The impact on SAPHRIS's market share could be significant if generics enter without restrictions.

What Are the Regulatory and Patent Considerations?

The last patent for SAPHRIS expired in 2020, though secondary patents and exclusivity rights may extend until 2027. No recent patent litigations or legal disputes have been publicly recorded. Agencies such as the USPTO have granted secondary patents covering formulations and manufacturing processes extending patent life.

Generic approval processes rely on abbreviated new drug applications (ANDAs), which require bioequivalence data. Approval timelines depend on patent litigation outcomes and regulatory review durations, typically taking 12-24 months from filing.

How Should Industry Stakeholders Approach Future Outlooks?

Pharma companies should monitor patent litigation and regulatory filings closely. For generic manufacturers, early filing of ANDAs can target 2024-2025 approval windows. Clinicians and payers should prepare for increased affordability once generics enter, potentially shifting prescribing patterns towards cost-effective options.

Investors should watch for indications of patent litigation success, potential legal challenges, and market entry strategies, as these will influence pricing and sales projections.

Key Takeaways

- SAPHRIS's 2022 U.S. sales around $120 million, with limited market share among SGAs.

- Competition from risperidone, aripiprazole, and lurasidone creates pricing and market challenges.

- Price stability is expected through 2025 unless early generic approval occurs; potential 50% decrease post-generic entry.

- Patent exclusivity risks extend until 2027; patent litigations influence timing of generic competition.

- Market growth prospects hinge on expanding indications and payer acceptance despite competitive pressures.

FAQs

1. When will generic asenapine likely enter the market?

Based on patent litigation and regulatory timelines, generic approval could occur between 2024 and 2025 if patent challenges are successful.

2. How will generic entry affect SAPHRIS sales?

Sales are expected to decline sharply—potentially by 50%—due to lower prices and increased market access for generics.

3. Are there any exclusive marketing rights for SAPHRIS post-2020?

No. The primary patent expired in 2020; secondary patents may provide limited exclusivity until 2027.

4. How does SAPHRIS compare with oral formulations of SGAs?

SAPHRIS’s sublingual formulation offers some convenience but does not significantly outperform oral formulations in efficacy or side effect profile.

5. What strategies could enhance SAPHRIS’s market share?

Expanding indications, improving formulary positioning, and developing long-acting formulations could attract prescribers and patients.

References

- IQVIA. "U.S. Prescription Drug Market Data." 2022.

- FDA. "Asenapine (SAPHRIS) Approval History." Accessed 2023.

- Statista. "Market size of antipsychotics worldwide." 2022.

- U.S. Patent Office. Patent filings related to asenapine. 2015–2022.

- EvaluatePharma. "Second-generation antipsychotics market forecast." 2022.

More… ↓