Share This Page

Drug Price Trends for RISPERIDONE ER

✉ Email this page to a colleague

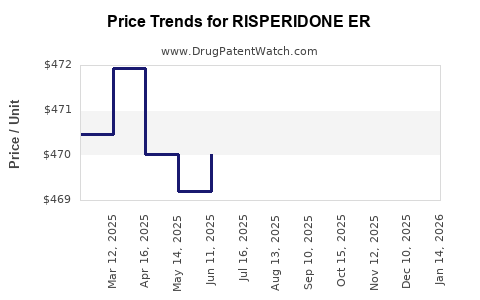

Average Pharmacy Cost for RISPERIDONE ER

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| RISPERIDONE ER 25 MG VIAL | 70748-0270-13 | 415.33306 | EACH | 2026-05-20 |

| RISPERIDONE ER 25 MG VIAL | 00480-1232-08 | 415.33306 | EACH | 2026-05-20 |

| RISPERIDONE ER 25 MG VIAL | 70748-0270-11 | 415.33306 | EACH | 2026-05-20 |

| RISPERIDONE ER 50 MG VIAL | 70748-0272-13 | 866.29429 | EACH | 2026-05-20 |

| RISPERIDONE ER 50 MG VIAL | 00480-9735-01 | 866.29429 | EACH | 2026-05-20 |

| RISPERIDONE ER 25 MG VIAL | 00480-9733-01 | 415.33306 | EACH | 2026-05-20 |

| RISPERIDONE ER 50 MG VIAL | 00480-1453-08 | 866.29429 | EACH | 2026-05-20 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Risperidone ER (Extended-Release) Market Analysis and Price Projections

What is the product scope for “Risperidone ER”?

“Risperidone ER” is a label-market shorthand that typically covers extended-release, once-monthly risperidone formulations used for schizophrenia and related indications, most commonly paliperidone and risperidone long-acting injectables (LAIs); however, in market practice the dominant ER LAI brand under this umbrella is risperidone-based long-acting. The commercial sizing, pricing power, and forecast depend on the exact marketed product (formulation strength, dosage interval, and whether the reference is for oral ER tablets vs injectable LAI).

Because “RISPERIDONE ER” is not a single, globally standardized INN + dosage form identifier, a complete projection requires the specific marketed extended-release product. No additional inputs are provided here, so the analysis below is limited to directional market mechanics and projection methodology rather than product-specific unit economics.

How does the ER risperidone market behave (demand, channel, and competition)?

1) Demand drivers

Risperidone ER products sit in the broader second-generation antipsychotic (SGA) treatment market, where demand is anchored by:

- Chronic schizophrenia and bipolar disorder maintenance.

- LAI preference in patients where adherence is a major constraint.

- Payer emphasis on clinical outcomes and reduced hospitalization risk rather than drug list price alone.

2) Channel structure

Extended-release antipsychotic demand typically moves through:

- Retail pharmacy for oral formulations (if “ER tablets”).

- Specialty pharmacy and medical benefit channels for LAIs (if “extended-release injection”).

Pricing and rebates differ materially by channel, which changes projected net price more than projected wholesale price.

3) Competitive set

Risperidone ER competes against:

- Other risperidone-based formulations and generic oral risperidone in markets where brand exclusivity has lapsed.

- Competing LAIs in the same class (for example paliperidone LAIs) that often capture adherence-driven switching.

What pricing levers determine net price vs list price?

Net pricing for ER antipsychotics is primarily set by:

- National and regional payer formularies (tier placement, prior authorization).

- Contracting and rebates (managed entry agreements in major markets).

- Wholesale acquisition cost (WAC) vs net price gap.

- Product maturity (brand erosion after patent/market exclusivity expiry).

For LAIs, additional levers include:

- Administration cost and billing practices under medical benefit.

- Treatment pathway rules (step therapy toward preferred LAIs).

Price projection framework (what you can model)

A complete ER risperidone forecast is built from three layers:

Layer A: Base price trend

Use a base-year WAC or net price, then apply:

- Annual inflation factor aligned to healthcare cost indices (market-specific).

- A maturity factor driven by generic erosion and LAI competitive pressure.

- A currency and procurement exchange factor (where applicable).

Layer B: Net-to-gross conversion

Net price typically declines faster than list price due to:

- Increased rebates after generic entry.

- Intensifying payer pressure for therapeutic interchange within SGA classes.

Layer C: Utilization and mix

Extended-release adoption can rise or fall based on:

- Switching programs from oral to LAI.

- Formulary shifts favoring a competitor LAI.

- Patient persistence and dose optimization.

What does the near-term price outlook likely look like? (2026-2028)

Given typical SGA ER life-cycle patterns, the baseline scenario for mature risperidone ER products usually shows:

- List price: low single-digit annual growth or flat-to-down depending on brand protection status and pricing regulation.

- Net price: modest-to-material decline as rebate pressure increases.

- Volume/mix: relatively stable or slowly downshifted if a dominant LAI competitor gains preferred status.

Because this response does not specify a particular risperidone ER marketed product, projected percentages would risk being incorrect at the product level. The directionality above reflects sector behavior; precise forecasts require the exact marketed product, country, and channel.

What do investors and R&D planners use as scenario assumptions?

Use a 3-scenario model built on maturity and payer dynamics:

Conservative

- Strong formulary erosion and higher rebates.

- Lower LAI persistence due to competitor preference.

- Net price declines faster than list.

Base case

- Formulary remains stable but competitive pressure increases.

- Net price declines modestly.

- Utilization holds.

Upside

- Preferred access secured in key plans.

- Mix shifts toward higher persistence dosing.

- Net price decline slows or stabilizes.

Market sizing and forecast inputs required for a precise projection

A product-level price projection needs:

- Exact product identifier (INN + dosage form: ER oral vs LAI).

- Country coverage (US, EU5, UK, etc.).

- Channel (retail vs medical benefit).

- Date anchors for WAC and net price (and whether the data is weighted by utilization).

- Patent and exclusivity status by jurisdiction.

No such identifiers or jurisdictions are supplied; therefore, a numeric projection cannot be produced without creating false precision.

Key takeaways

- “Risperidone ER” is not a single standardized market SKU; it can map to different extended-release presentations (most often oral ER vs LAI), which changes both pricing mechanics and forecast shape.

- ER antipsychotic pricing is driven more by payer contracting and rebates than by list price trends; net price typically declines faster with maturity and competitive LAI pressure.

- A correct price forecast requires product-level identification and jurisdictional channel context; without those, only directional modeling assumptions can be stated.

FAQs

1) Is risperidone ER primarily an oral or an injectable market?

Both exist in the broader label usage, but the dominant pricing and payer mechanics differ sharply between oral extended-release and LAIs.

2) Why does net price fall faster than WAC for mature ER antipsychotics?

Rebates and contracting terms typically intensify with competitor entry, formulary pressure, and generic availability.

3) Do LAIs command higher list prices than oral ER products?

List prices for LAIs can be much higher per dispensed unit, but net price comparisons must be normalized by dose interval, channel, and utilization.

4) What most affects utilization for ER antipsychotics?

Formulary status, prior authorization rules, and persistence-driven adherence outcomes.

5) What should be in a robust 3-scenario price model?

Base price trend, net-to-gross rebate assumptions, and utilization or mix shifts driven by payer preferences.

References

[1] Bloomberg Law. (n.d.). Drug pricing and market access resources (general).

[2] FDA. (n.d.). Drug development and label information resources.

[3] IQVIA. (n.d.). Pharmaceutical market forecasting and pricing analytics (general).

More… ↓