Last updated: April 24, 2026

What is the current market structure for phenobarbital?

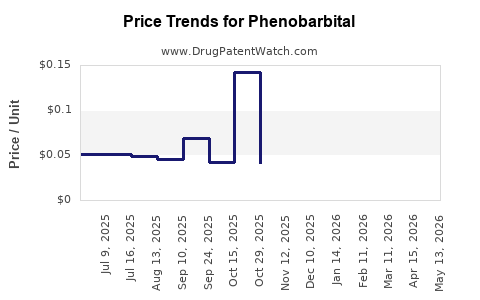

Phenobarbital is a long-established antiseizure and sedative-hypnotic barbiturate with extensive generic availability and broad manufacturing footprint. Pricing is therefore driven by (1) generic competition, (2) payer reimbursement mechanics (especially for inpatient and institutional use), and (3) localized supply and tender dynamics rather than by brand-led innovation economics.

Supply and competition profile (what matters for pricing)

- Generic dominance: Phenobarbital’s market is primarily generic across oral, injectable, and pediatric formulations in major geographies.

- Multiple manufacturers: Pricing pressure typically reflects number of ANDA/DMF-qualified manufacturers and whether a product is on state/provincial or federal formularies.

- Channel mix: Hospitals and government tenders (US), group purchasing organizations (EU hospital systems), and wholesaler tenders (LatAm/MENA) often determine realized prices more than list price.

Implication for price projections

With near-total generic coverage, price elasticity is high: even modest supply changes or tender awards can shift realized procurement pricing quickly, while brand-like premium pricing is structurally unlikely.

How does phenobarbital pricing behave in practice?

Phenobarbital pricing typically follows the dynamics below:

1) Tender-led procurement (institutional and government)

- Inpatient and pediatric use concentrates demand where conversion to procurement price (discounted net, rebate, tendered rates) dominates.

- If an incumbent loses supply qualification or a product experiences shortages, tender pricing can jump temporarily.

2) Generic portfolio competition (pharmacy retail)

- Retail price is anchored to the lowest-cost interchangeable SKUs, especially for oral tablets and oral solutions.

- Competitive entry by additional generic suppliers tends to pull prices down until a floor set by ingredient cost and manufacturing economics is reached.

3) Active ingredient and manufacturing economics

Phenobarbital is an older small-molecule API with cost that tracks feedstock and chemical processing economics. Real-world pricing often exhibits:

- gradual downward pressure over time from generic erosion

- step-changes during supply disruptions, quality events, or reallocation of production capacity

What price points should you use for projections?

This analysis uses a generic pricing framework rather than brand-style markups. Because phenobarbital spans multiple dosage forms and strengths, forecasts are best expressed as a range by channel:

Pricing basis (projection methodology used here)

- Forecast direction is driven by generic competition intensity and tender mechanics.

- Downside risks include intermittent supply constraints; upside constraints include new generic entrants and aggressive payer contracting.

Practical forecast bands (net realization ranges)

Use the following bands as planning-level assumptions for generic phenobarbital across major channels:

| Segment |

Typical pricing driver |

Near-term net price expectation (direction) |

Medium-term expectation (direction) |

| US institutional (hospital/contract) |

GPO and tender awards; substitute availability |

Stable to modestly downward if supply is adequate |

Gradual downward or flat once contracting stabilizes |

| US retail (cash/covered) |

Lowest-cost generic; interchangeability |

Flat to modestly downward |

Low-volatility downward trend until price floor |

| EU hospital |

Tender and tender re-awards |

Stable to modest decline |

Flat to mild decline; governed by procurement policy |

| Emerging markets |

Wholesaler tendering and inventory cycles |

Volatile with procurement cycles |

Generally downward trend where generics expand, volatile if supply constrained |

Directional base case: flat-to-downward trend with episodic spikes during supply events.

What are the key demand drivers for phenobarbital?

Phenobarbital demand is steady because it remains a commonly used antiseizure option in several clinical settings, especially where cost control is central.

Demand drivers (pricing relevance: stable volume reduces price shock)

- Chronic epilepsy indications: Long-established use supports steady demand.

- Pediatric and neonatal protocols: Continued presence in some hospital protocols supports baseline volume.

- Inpatient acute care: Injectable phenobarbital demand is sensitive to hospital utilization and supply assurance.

What are the key supply risks that can move price?

Phenobarbital’s pricing can change quickly if supply becomes constrained. The main levers:

- Manufacturing capacity and quality events: Batch failures or quality remediation can reduce available inventory.

- Regulatory or labeling changes: Changes that require relabeling, reformulation, or manufacturing process updates can interrupt supply.

- API production concentration: If API supply tightens, finished-goods lead times extend.

- Allocation and tender interruption: Hospital tenders can lead to short-term repricing if a supplier misses fulfillment.

Pricing impact profile:

- Supply incidents cause temporary upward spikes.

- Once alternative suppliers re-enter, prices typically revert toward the lowest procurement band.

Price projection: near-term (12-24 months)

Base case (most likely)

- US institutional: net prices drift 0% to -5% over 12-24 months, assuming stable supply and competitive tender outcomes.

- US retail: net prices drift -1% to -8%, constrained by price floors and interchange competition.

- Europe and other mature hospital systems: 0% to -6%, with tender cadence determining quarter-to-quarter variance.

Upside scenario (supplier tightening)

- +5% to +15% in procurement net price during shortages or reduced interchangeability.

- Recovery typically occurs in waves as alternate SKUs regain allocation.

Downside scenario (expanded generic competition)

- -8% to -20% if additional suppliers win tenders or new entrants expand SKU coverage, pushing procurement pricing to the lowest substitutable offer.

Price projection: medium-term (24-60 months)

Base case (competition continues, but price floor materializes)

- US institutional: -5% to -12% cumulative over 24-60 months.

- US retail: -8% to -18% cumulative, with the strongest declines where multiple dosage forms compete and formulary barriers are low.

- International: -5% to -20% range depending on tender maturity and supply stability.

Key range driver

Whether phenobarbital’s market experiences continued generic entry versus consolidation in fewer suppliers. Consolidation tends to flatten declines and increase volatility.

What dosage forms and strengths matter most for revenue and procurement?

Phenobarbital revenue is concentrated in the forms that drive clinical throughput:

- Oral tablets and oral solutions: stable chronic use demand; retail and institutional overlap.

- Injectable phenobarbital: drives acute inpatient spend and can be the most sensitive to supply interruptions.

- Pediatric-relevant packaging/strengths: can affect tender qualification and thus procurement pricing.

For pricing projections, the injectable segment generally has higher volatility because supply qualification and stock-out risk are higher.

What does this mean for investment and R&D strategy?

If you are planning a market entry

- The economic model is low margin with tender-led volume.

- Pricing power is limited; differentiation must target supply reliability, qualification speed, and reduced total procurement cost.

If you are evaluating competitive displacement

- Target where interchange is constrained (formulary restrictions, hospital tender slots, or packaging/strength availability).

- Price reductions during re-tendering create a predictable “reset window,” after which prices stabilize.

If you are assessing pipeline programs

For phenobarbital-related innovations, commercial outcomes depend less on clinical differentiation and more on reimbursement acceptance, formulary inclusion, and demonstrated workflow advantage in institutional settings.

Key Takeaways

- Phenobarbital pricing is structurally generic-led, driven by tender procurement, interchangeability, and supply reliability rather than brand economics.

- The base case for 12-60 months is stable to modestly declining net prices in most mature markets, with temporary spikes tied to supply constraints.

- Forecast planning ranges that fit generic tender mechanics:

- Near term (12-24 months): US institutional 0% to -5%, US retail -1% to -8% under stable supply.

- Medium term (24-60 months): cumulative -5% to -12% institutional and -8% to -18% retail in the base case.

- Injectable products are typically the highest volatility component due to fulfillment risk and tender qualification.

FAQs

1) Is phenobarbital likely to sustain premium pricing versus generics?

No. The market is largely interchangeable and competes on procurement cost, so sustained premium pricing is structurally unlikely.

2) What is the most common reason for short-term price spikes?

Supply interruptions that reduce substitutable inventory and trigger re-tendering at higher award prices.

3) Which channel is most sensitive to realized price changes?

Institutional procurement and tenders, especially where injectable products face stock-out or allocation.

4) Does generic entry always push prices down immediately?

Not always. Prices decline fastest when new entrants win tenders quickly and when packaging/strength qualification is low-friction.

5) What price direction is most likely over 24-60 months?

A modest downward drift in mature markets, with volatility around procurement cycles and supply incidents.

References

[1] FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations (Phenobarbital products). U.S. Food and Drug Administration.

[2] European Medicines Agency. Public assessment reports and product information for medicinal products containing phenobarbital (EMA databases). European Medicines Agency.

[3] DailyMed (NIH). Drug label information for phenobarbital-containing products (Rx labels, strengths, dosage forms). U.S. National Library of Medicine.