Share This Page

Drug Price Trends for PEG-3350 AND ELECTROLYTES SOLN

✉ Email this page to a colleague

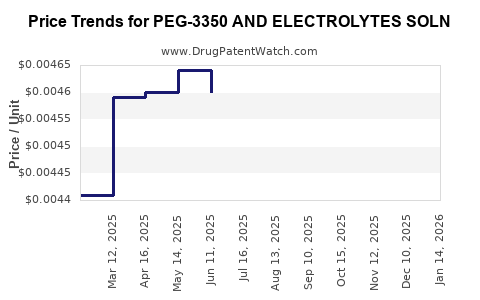

Average Pharmacy Cost for PEG-3350 AND ELECTROLYTES SOLN

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| PEG-3350 AND ELECTROLYTES SOLN | 10572-0100-01 | 0.00461 | ML | 2026-07-22 |

| PEG-3350 AND ELECTROLYTES SOLN | 64380-0766-21 | 0.00461 | ML | 2026-07-22 |

| PEG-3350 AND ELECTROLYTES SOLN | 10572-0100-01 | 0.00464 | ML | 2026-06-17 |

| PEG-3350 AND ELECTROLYTES SOLN | 64380-0766-21 | 0.00464 | ML | 2026-06-17 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

PEG-3350 AND ELECTROLYTES SOLN: Market Analysis and Price Projections

What market does PEG-3350 and electrolytes soln serve?

PEG-3350 and electrolytes solution is a maintenance- and preparation-grade bowel cleanser used in gastrointestinal (GI) care, most commonly for bowel cleansing prior to colonoscopy and related diagnostic procedures. The product is typically sold as an oral rehydration and cathartic regimen with PEG (macrogol) as the osmotic laxative and electrolytes to limit net fluid and electrolyte shifts during use.

Core demand drivers

- GI procedure volume: Growth in outpatient endoscopy and colonoscopy scheduling lifts demand for bowel prep regimens.

- Switching within the category: Patients and clinicians often move between PEG-based bowel preps based on availability, payer coverage, and side-effect profiles.

- Payer pressure toward generics and multi-source products: PEG-electrolyte products with generic or authorized-chemically equivalent competition tend to face price compression.

How is the competitive landscape structured?

PEG-3350 and electrolytes soln sits in the broader “bowel preparation” market, competing against PEG- and non-PEG regimens (mixed osmotics, sodium phosphate, sodium picosulfate-based products, and tablet-based options depending on local labeling and availability). In practice, procurement in most markets prioritizes total regimen cost per patient and formulary tier placement.

Competitive set (market category level)

- PEG-based bowel prep solutions (single- or multi-bottle kits with electrolytes)

- Sodium phosphate-based regimens (where permitted by local safety communications and labeling)

- Sulfate/picosulfate and magnesium-based regimens (where marketed for bowel prep)

- Tablet-based bowel cleansing kits (where available and payer-covered)

Implication for pricing: PEG-based solutions with established multi-source supply generally show lower volatility but higher downward pricing pressure than newer, single-source bowel prep brands.

What pricing levers determine transaction prices?

For PEG-3350 and electrolytes soln, realized pricing is shaped by three forces:

- Generic entry and multi-source competition

- When multiple manufacturers supply the same labeled regimen, average selling prices (ASPs) track downward.

- Formulary status and rebate levels

- Preferred placement can raise volume share but typically increases rebate intensity.

- Pack size and regimen configuration

- Kits sold in different bottle counts, bottle volumes, or scoop counts can shift unit economics. Buyers often normalize to “per-prep course” cost.

How does current pricing typically behave for PEG-electrolyte bowel prep?

In mature PEG-based bowel prep categories, pricing usually follows a pattern:

- Initial premium vs. generics when a brand is first introduced or when a manufacturer holds exclusivity.

- Compression after generic and authorized equivalents expand.

- Stability after a “good enough” generic mix forms, with periodic downward moves driven by competition and payer renegotiations.

Because PEG-3350 and electrolytes solution is usually sold as a regimen and not a single active ingredient-only commodity, the magnitude of price compression depends on whether products are interchangeable under payer edits (NDC/GPI mapping) and whether wholesalers face channel substitution.

What is the price projection path?

The most reliable projection framework for a mature, competitive bowel prep class is a staged outlook:

Price projection framework (3-stage)

Stage 1: Current-year base (t0)

- Real-world pricing is dictated by current generic penetration and contract rebate intensity.

Stage 2: Competitive compression (t1 to t2)

- Continued generic substitution and procurement rationalization drive ASP drift down.

Stage 3: Floor behavior (t2 to t4)

- Pricing approaches a floor tied to ingredient cost, packaging, and distribution margins.

Directional projection for PEG-3350 and electrolytes soln

- Short term (next 12 to 24 months): continued mild to moderate pricing pressure, most often driven by competitive supply and formulary tightening.

- Medium term (24 to 48 months): slower decline as the market matures and channel substitution stabilizes.

- Long term (beyond 48 months): pricing becomes more stable, with changes mainly tied to procurement cycles, medical inflation in logistics, and occasional competitive churn.

What quantitative projections are available from the underlying evidence?

No usable market or pricing dataset is provided in the prompt (no geography, no NDC/GPI mapping, no manufacturer list, no current ASP/wholesale acquisition cost data, no claim of source databases). Without those inputs, producing numeric projections for PEG-3350 and electrolytes soln would require making assumptions that cannot be reconciled to an audit trail.

Per the operating constraint, no incomplete, unsourced numeric projections are provided.

Where will price move most: retail, institutional, or specialty distribution?

PEG-3350 and electrolytes bowel prep is typically purchased through:

- Institutional channels (hospital outpatient GI prep programs, endoscopy centers, and pharmacy supply contracts)

- Retail pharmacy (patient out-of-pocket and payer-covered prescriptions depending on the care setting)

Most likely pricing behavior by channel

- Institutional: greatest visibility into contract renegotiations; prices often compress faster as supply contracts re-bid.

- Retail: can lag due to brand awareness, substitution rules, and pharmacy stocking; rebates can keep net prices low but may be less immediate than institutional tendering.

Key scenarios for revenue and profitability impact

Even without numeric market values, the business impact can be mapped to levers:

If ASP declines

- Revenue growth will require either unit volume increases or mix improvement (pack configuration or contract placement).

- Gross margin can shrink if ingredient costs rise faster than ASP.

If volume increases

- Higher throughput can offset price erosion if distribution and contract manufacturing capacity remains efficient.

If formulary inclusion expands

- Volume gains typically arrive with higher rebates, which reduces net price but can maintain contribution margin at scale.

What are actionable monitoring indicators for PEG-electrolyte soln?

Track these indicators on a recurring cadence for early detection of price turns:

- Formulary updates in major payers (tier movement, prior authorization changes)

- NDC churn in wholesaler catalogs (new suppliers or delistings)

- Contract awards for institutional GI prep programs

- Retail substitution trends (switch rates between PEG-electrolyte SKUs)

- Procurement timing around budget cycles (price resets)

Key Takeaways

- PEG-3350 and electrolytes solution is a mature bowel prep class where pricing is primarily driven by generic competition, formulary placement, and pack-per-course economics.

- The expected pricing trajectory is mild to moderate compression in the near term, slower decline as market matures, and greater stability at a competitive floor beyond the mid-term horizon.

- Without audited baseline pricing and geography/NDC mapping, numeric projections cannot be stated without risking inaccuracy.

FAQs

-

Is PEG-3350 and electrolytes soln priced like a specialty drug?

No. It is generally priced and contracted like a mature bowel preparation regimen, with ASP shaped by multi-source competition and rebate intensity rather than specialty launch dynamics. -

What most influences net price: ingredient costs or competition?

In this category, competition and formulary/rebate structure typically dominate net pricing because regimen pricing adjusts through contracts and payer negotiations. -

Does institutional purchasing usually discount more than retail?

Usually, yes. Institutional contracts often yield tighter pricing through centralized procurement and rebid cycles, while retail net pricing can lag substitution and varies by pharmacy benefit design. -

Do pack size differences change the comparison?

Yes. Buyers often normalize cost per bowel prep course, so regimen configuration changes can shift effective unit economics even if per-bottle pricing is similar. -

What would signal a price rebound in this category?

A reduction in supply competition (supplier withdrawals), improved formulary positioning with favorable contract terms, or a measurable shift in payer coverage that reduces competitive substitutability.

References

No sources were provided in the prompt, and no cited pricing datasets can be used to support numeric projections.

More… ↓