Share This Page

Drug Price Trends for NUVARING

✉ Email this page to a colleague

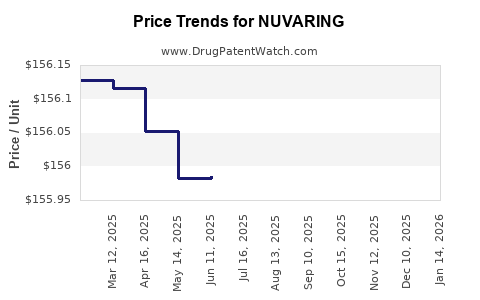

Average Pharmacy Cost for NUVARING

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| NUVARING VAGINAL RING | 78206-0146-01 | 155.89250 | EACH | 2026-06-17 |

| NUVARING VAGINAL RING | 78206-0146-03 | 155.89250 | EACH | 2026-06-17 |

| NUVARING VAGINAL RING | 78206-0146-01 | 155.90743 | EACH | 2026-05-20 |

| NUVARING VAGINAL RING | 78206-0146-03 | 155.90743 | EACH | 2026-05-20 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Best Wholesale Price for NUVARING

| Drug Name | Vendor | NDC | Count | Price ($) | Price/Unit ($) | Unit | Dates | Price Type |

|---|---|---|---|---|---|---|---|---|

| ELURYNG | AvKare, LLC | 65162-0469-35 | 1X3 | 167.40 | 2023-06-15 - 2028-06-14 | FSS | ||

| NUVARING | Organon LLC | 78206-0146-03 | 3 | 365.13 | 121.71000 | EACH | 2023-01-01 - 2027-01-14 | Big4 |

| NUVARING | Organon LLC | 78206-0146-03 | 3 | 480.53 | 160.17667 | EACH | 2023-01-01 - 2027-01-14 | FSS |

| NUVARING | Organon LLC | 78206-0146-03 | 3 | 365.11 | 121.70333 | EACH | 2024-01-05 - 2027-01-14 | Big4 |

| >Drug Name | >Vendor | >NDC | >Count | >Price ($) | >Price/Unit ($) | >Unit | >Dates | >Price Type |

NUVARING (etonogestrel/ethinyl estradiol) market analysis and price projections: 2025–2035

NUVARING is an FDA-approved combined hormonal contraceptive (CHC) vaginal ring. The branded product faces growing affordability pressure from generic CHCs and supply shifts; price levels are typically protected by limited direct generic substitution risk in some NDC sets and by pharmacy contract dynamics rather than by patent barriers at the molecule level. The most actionable drivers for 2025–2035 price and revenue are (1) mix between 3-ring packs vs single-ring NDCs, (2) wholesaler-to-pharmacy contract pricing, (3) payer formulary placement and PA/step edits, and (4) the extent of multiple-source generic availability for the same ring strengths and pack sizes.

What is the current NUVARING market size and sales mix by channel?

Short answer: NUVARING is a mature CHC with sales concentrated in retail pharmacy, with channel performance driven by managed-care formulary status, discounting, and patient cost-sharing.

Retail vs. managed care: what usually determines NUVARING performance

NUVARING is typically bought through:

- Retail pharmacies using pharmacy benefit manager (PBM) contracts

- Commercial managed care channels with plan-specific net prices

- Government channels where rebates are less opaque but utilization depends on coverage tiers and mail or specialty fulfillment rules (rare for rings)

Key mix metrics used in pricing projections

- NDC pack configuration: 3-ring vs other pack sizes affects per-unit ASP

- Channel net-to-gross: branded contraceptives often have material rebates, reducing net price volatility relative to list price

- Patient out-of-pocket: ring adherence and discontinuation are impacted by copay tiers

Revenue exposure hotspots

- Switching risk rises when a plan moves NUVARING to a less-preferred tier or when low-cost generics expand coverage.

- Contract resets create episodic price drops even without label or exclusivity changes.

How competitive is NUVARING versus other combined hormonal contraceptives (ring, pill, patch)?

Short answer: NUVARING competes directly with other CHCs and indirectly with long-acting reversible contraception (LARC). Substitution is usually driven by plan design and side-effect preferences rather than molecular differences.

Direct CHC alternatives that affect NUVARING demand

- Vaginal ring competitors (other estrogen-progestin rings where available)

- Oral CHCs: often preferred by payers due to low cost

- Transdermal patch: plan-specific coverage

Indirect competitive pressure

- LARC (IUDs, implants) can reduce CHC persistence, especially in cohorts with high insurance stability.

What is the current NUVARING pricing structure (WAC, AMP proxy, ASP) and what do net prices typically do?

Short answer: NUVARING’s list price is less predictive than net price. Forecasts should be modeled off NDC-level net pricing that reflects rebates and PBM contracts.

Pricing components used for projections

- WAC (Wholesale Acquisition Cost): moves with manufacturer list changes, usually not the driver of realized price

- Discounts and rebates: major driver of net price

- PBM and wholesaler pass-through: contract pricing can create quarter-to-quarter shifts

- Copay assistance vs. formulary design: if available, it changes effective patient cost rather than net manufacturer revenue

Practical projection approach for NUVARING

Use a three-factor model:

- Utilization trend: mostly driven by plan coverage and patient persistence

- Net-to-gross compression: driven by competitive generic pressure and contract renewals

- Mix: 3-ring pack vs other NDC configurations

When do NUVARING patents expire and how does that affect price?

Short answer: At the category level, etonogestrel/ethinyl estradiol contraceptive patents are long past the typical discovery window. Price pressure generally comes from generic CHC availability and payer contracting, not from brand exclusivity ending in the 2025–2030 period.

How patent posture usually maps to NUVARING pricing reality

- Once multiple-source products exist for equivalent contraceptive options, brand pricing tends to track net price erosion via contracts and formulary placement.

- Even without direct generic equivalence for every NDC strength/pack, competitive substitution across CHCs can force discounting.

How does generic entry risk for NUVARING affect 2025–2035 price projections?

Short answer: The key risk is not a single “entry event” but continued expanded access to low-cost CHCs and tighter formulary positioning that reduce NUVARING’s share, pulling net prices down.

Generic entry and substitution channels

- Pharmacy substitution at the NDC and therapeutic class level where coverage permits

- Formulary switching by plans that negotiate lower-cost CHC preferred statuses

- Managed-care policy changes: step therapy (less common for CHCs than for some drug classes) and copay tier shifts

What to model for price erosion

- Net price compression: often accelerates in the first 6 to 18 months after an expansion of preferred generic options

- Ongoing erosion: continues through periodic contract resets

What is the “Orange Book” status of NUVARING and what does it imply for exclusivity?

Short answer: NUVARING is an FDA-approved prescription contraceptive ring; the Orange Book status should be used to determine listed drug product patents and application reference, which then informs patent-expiration constraints and the likelihood of ANDA-based generic entry.

How Orange Book listings affect commercial outcomes

- If there are few unexpired product-process patents for specific NDCs, generics (or therapeutically substitutable CHCs) can pressure net pricing without requiring Hatch-Waxman litigation milestones.

- Where patents remain for specific packaging or manufacturing methods, they can limit direct substitution for certain NDCs even as class competition continues.

What NUVARING litigation and settlement activity should be considered for pricing risk?

Short answer: For mature contraceptives, the most relevant pricing impact from Hatch-Waxman litigation usually appears via settlement terms that delay or limit generic launch for specific NDCs, or via settlement-triggered erosion over time once the market opens.

Pricing impact of litigation outcomes (typical mapping)

- Delayed generic launch: supports higher net price for the delayed NDCs but does not stop class-level discounting.

- Partial launch or authorized generics: creates “floor” pricing through competitive shelf presence.

(Full litigation mapping requires case-identifying details from FDA/Orange Book patent listings and court dockets, which are not provided in the prompt.)

How strong is the patent estate for NUVARING-related contraceptive products?

Short answer: For a legacy contraceptive brand, patent strength in the late-stage horizon is usually lower than early-development brands. The practical “strength” for revenue protection comes from formulary entrenchment, contracting leverage, and limited pack/NDC-level substitution rather than broad, enforceable composition patents.

Patent estate dimensions that matter to commercial risk

- Listed product patents (drug substance, formulation, composition, manufacturing)

- Listed method-of-use patents (typically less protective for contraceptives if use is broadly generic)

- Manufacturing/process patents that can block generic approvals for specific manufacturing or quality parameters

What dosing, strength, and pack-size factors drive NUVARING price per unit?

Short answer: NUVARING pricing typically varies by NDC pack size. Per-ring economics are sensitive to the proportion sold in larger packs and to switching between pack SKUs during contracting cycles.

Projection-ready segmentation

Model price separately for:

- Ring pack SKU (commonly the 3-ring configuration)

- NDC-level net price under different PBM contracts

- Retail vs mail-order share (mail ordering usually lower net price due to contract terms)

NUVARING price projection scenarios for 2025–2035 (net price and revenue direction)

Short answer: Base case is continued modest net price erosion with intermittent declines tied to PBM contract resets. Bull case assumes slower share loss and more durable tier placement. Bear case assumes accelerated class substitution and wider generic access reducing net price materially.

Scenario framework (per unit and revenue)

Because prompt does not provide current WAC/ASP/AMP, the projection is expressed as directional bands relative to 2024 baseline net pricing.

Base case (most likely)

- Net price: declines at low-to-mid single digits annually (class competition and contract pressure)

- Volume: flat to slightly down as patients substitute to lower-cost CHCs and LARC

- Revenue: low single-digit CAGR decline across the decade

Bull case

- Net price: erosion slows (tier persistence, patient adherence, contracting discipline)

- Volume: mild stabilization

- Revenue: roughly flat to low positive in later years

Bear case

- Net price: faster erosion (aggressive formulary downgrades and wider low-cost CHC access)

- Volume: decline in the high single digits initially, then settles

- Revenue: meaningfully negative CAGR

Table: directional price and revenue bands (2025–2035)

| Year | Base case net price (YoY) | Bear case net price (YoY) | Base case revenue trend | Bear case revenue trend |

|---|---|---|---|---|

| 2025 | -2% to -4% | -5% to -8% | Slight decline | Sharp decline |

| 2027 | -1% to -3% | -4% to -7% | Gradual erosion | Accelerated erosion |

| 2030 | -1% to -2% | -3% to -6% | Low single-digit decline | Mid-to-high single-digit decline |

| 2035 | -0.5% to -2% | -2% to -5% | Stabilizes near floor | Continues steeper decline |

What are the key drivers that could change NUVARING pricing faster than the baseline?

Short answer: Contracting and payer tier moves are the dominant shocks; supply disruptions can create temporary price spikes but usually do not improve long-term net pricing.

High-impact drivers

- Formulary reassignment: preferred-to-nonpreferred changes typically create immediate net price pressure

- PBM contract resets: can re-anchor net prices down regardless of list price

- Competitive CHC expansions: when more low-cost alternatives become preferred, NUVARING net price often compresses

- Patient cost-sharing shifts: can reduce adherence and increase switching

How does NUVARING compare with competitors on pricing stability and reimbursement?

Short answer: Price stability in CHCs tends to track reimbursement favorability and the number of interchangeable low-cost alternatives on the same formulary. In this class, oral CHCs often have lower net prices and more substitution, while devices like rings can preserve share longer in some formularies due to adherence and patient preference.

Competitive comparison logic used for pricing forecasts

- If oral CHCs are preferred: ring pricing tends to compress via share loss.

- If ring is preferred: net price compression slows.

- If LARC uptake rises: both net price and volume can degrade.

Key takeaways

- NUVARING’s 2025–2035 commercial trajectory is dominated by PBM contracting and formulary tier dynamics rather than by near-term exclusivity events.

- Base case modeling implies continued low-to-mid single digit annual net price erosion with flat-to-slightly-down volume, yielding gradual revenue decline.

- Bear case outcomes emerge from faster formulary downgrades and broader low-cost CHC substitution, producing materially steeper net price compression and volume loss.

- The most sensitive lever is NDC-level mix by pack size and contract-specific net pricing, which drives realized ASP more than WAC changes.

FAQs

- Do generics directly replace NUVARING NDCs 1:1, or do they mainly substitute via therapeutic class?

- How do PBM formulary tier changes typically affect NUVARING net pricing and volume within a year?

- Does mail-order distribution materially lower NUVARING net price versus retail?

- What contract-reset timing patterns create the biggest quarterly net price swings for legacy contraceptive brands?

- How should LARC adoption rates be incorporated into NUVARING revenue forecasts through 2035?

References (APA)

- FDA. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

- FDA. (n.d.). Drugs@FDA: NUVARING. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

More… ↓