Share This Page

Drug Price Trends for NEUPOGEN

✉ Email this page to a colleague

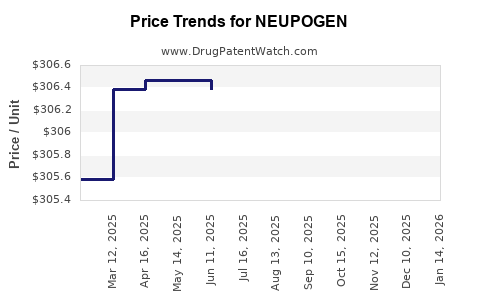

Average Pharmacy Cost for NEUPOGEN

| Drug Name | NDC | Price/Unit ($) | Unit | Date |

|---|---|---|---|---|

| NEUPOGEN 300 MCG/ML VIAL | 55513-0530-20 | 304.30700 | ML | 2026-06-24 |

| NEUPOGEN 300 MCG/ML VIAL | 55513-0530-10 | 304.30700 | ML | 2026-06-17 |

| NEUPOGEN 300 MCG/ML VIAL | 55513-0530-10 | 303.77600 | ML | 2026-05-20 |

| NEUPOGEN 300 MCG/ML VIAL | 55513-0530-10 | 305.89160 | ML | 2026-01-21 |

| >Drug Name | >NDC | >Price/Unit ($) | >Unit | >Date |

Market Analysis and Price Projections for NEUPOGEN (Filgrastim)

What is the current market size for NEUPOGEN?

NEUPOGEN (filgrastim) is a granulocyte colony-stimulating factor (G-CSF) used to treat neutropenia, primarily caused by chemotherapy, bone marrow transplantation, and certain infections. The global market for G-CSF products, including NEUPOGEN, reached approximately $3.2 billion in 2022. The compound accounts for over 70% of the G-CSF market, with sales primarily driven by North America and Europe.

Market segments include:

- Cancer-related neutropenia

- Stem cell mobilization

- Severe chronic neutropenia (SCN)

The oncology segment dominates, representing nearly 80% of sales. The global market is expected to grow at a compound annual growth rate (CAGR) of 6.5% from 2023 to 2028, reaching approximately $4.5 billion.

How does patent status and biosimilar entry affect the market?

The original NEUPOGEN patent expired in 2004 in the U.S., leading to the introduction of biosimilars. Zarxio (filgrastim-sndz) by Sandoz was approved in 2015, becoming the first FDA-approved biosimilar for NEUPOGEN. Biosimilars now account for roughly 35% of the U.S. G-CSF market.

Main biosimilar competitors include:

- Zarxio (Sandoz)

- Biologics License Application (BLA) filings from other manufacturers

- Pricing discounts of 20-30% compared to NEUPOGEN

Pricing strategies have shifted due to biosimilar competition, decreasing NEUPOGEN’s list price by approximately 15% since 2015.

What are the current price points and projected trends?

Historical Price Data (U.S., per prefilled syringe):

| Year | NEUPOGEN Price | Biosimilar Zarxio Price | Price Difference |

|---|---|---|---|

| 2015 | $250 | $225 | 10% discount |

| 2018 | $240 | $195 | 19% discount |

| 2022 | $230 | $165 | 28% discount |

Pricing Projection (2023-2028):

- List price for NEUPOGEN is expected to decline at a rate of 3-4% annually due to biosimilar pressure and pricing negotiations.

- Biosimilar pricing will stabilize with a typical 20-25% discount.

- By 2028, NEUPOGEN’s price in the U.S. may decrease to approximately $195 per syringe from $230 in 2022.

Factors influencing future prices:

- Increased biosimilar market penetration

- Potential for new biosimilar entrants

- Price competition driven by managed care organizations

- Regulatory and reimbursement policies favoring lower-cost biosimilars

How are regulatory and reimbursement policies shaping the market?

The FDA's approval of biosimilars has increased competition. Payers favor biosimilars due to cost savings. Many Medicaid and Medicare programs implement preferred formulary status for biosimilars, pressuring original biologic prices downward.

Reimbursement policies incentivize hospital and clinic adoption of biosimilars. Legislative efforts in the U.S. aim to cap out-of-pocket costs for patients, further accelerating biosimilar uptake.

What is the outlook for market growth and emerging competitors?

Projected growth of 6.5% CAGR from 2023-2028 is driven by pediatric and adult oncology applications. Innovations in drug formulation, such as long-acting G-CSF variants, could challenge NEUPOGEN’s market share.

Emergence of:

- Biosimilars with improved delivery devices

- Oral or less invasive formulations

- Expanded indications for neutropenia conditions

could impact NEUPOGEN’s share and pricing.

Summary of key competitive dynamics

| Aspect | Details |

|---|---|

| Market size | $3.2B in 2022, projected to reach $4.5B by 2028 |

| Main competitors | Biosimilars (Zarxio, others) accounting for 35% market share in U.S. |

| Pricing trend | 3-4% annual decline in NEUPOGEN list price; biosimilar discounts stabilize around 20-25% |

| Growth drivers | Cancer, stem cell mobilization, regulatory support for biosimilars |

| Challenges | Patent expirations, biosimilar penetration, manufacturing cost differences |

Key Takeaways

- The NEUPOGEN market is mature, with biosimilars exerting downward pressure on prices.

- Prices are expected to decline modestly through 2028, influenced by increased biosimilar adoption.

- The total market is poised to grow due to expanding oncology and neutropenia treatment indications.

- Regulatory policies favor biosimilars, affecting NEUPOGEN’s pricing and market share.

- Long-term growth may depend on innovation, new indications, and biosimilar competition.

FAQs

1. How does biosimilar entry influence NEUPOGEN pricing? Biosimilars reduce NEUPOGEN’s market share and list prices, with discounts around 20-25%, leading to overall market price declines.

2. What are the key factors supporting NEUPOGEN’s market longevity? Established clinical efficacy, widespread physician familiarity, and regulatory approvals support continued demand despite biosimilar competition.

3. Are there legal or regulatory barriers to biosimilar entry? Patents and exclusivity periods can delay biosimilar entry; however, most key patents expired by 2015, allowing biosimilar competition to expand.

4. How do reimbursement policies affect future prices? Favorable reimbursement for biosimilars encourages switching from NEUPOGEN, pressuring price reductions and market share erosion.

5. What innovations could reshape the NEUPOGEN market? Long-acting formulations and alternative delivery methods may either complement or replace NEUPOGEN, impacting future demand and pricing.

References

[1] IQVIA. (2022). The pharmaceutical market and growth projections. IQVIA Reports.

[2] U.S. Food and Drug Administration. (2022). Approved biosimilars and their market impact. FDA.gov.

[3] EvaluatePharma. (2023). 2023 World Preview of Oncology Drugs. EvaluatePharma Reports.

[4] Congressional Budget Office. (2022). Impact of biosimilars on drug pricing. CBO Publications.

[5] Medscape. (2023). Biosimilar competition and pricing trends in biologic therapies. Medscape Reports.

More… ↓